I walked into a crowded charging station, the smell of freshly brewed coffee filling the air, and overheard a heated conversation between two EV owners — Rachel and Mike. They were debating the merits of umbrella policies for their electric cars. Rachel, a proud Tesla Model 3 owner, swore by the added protection, while Mike, who leased a BMW iX, thought it was a waste of money. Sound familiar?

Rachel mentioned that her insurance provider, State Farm, offered a bundled deal that included an umbrella policy for an extra $200 per year. Mike, on the other hand, was paying $150 per month for his lease, and didn't want to add any more expenses. Know what the kicker is? His lease agreement with BMW Financial Services didn't even require him to have an umbrella policy.

That one stung, and I couldn't help but chime in. I asked them if they'd considered the potential risks of not having an umbrella policy. What if they were involved in a serious accident, and their regular insurance didn't cover all the damages? Would they be able to afford the excess costs out of pocket?

They both looked at me, taken aback, and I realized I'd struck a chord. We started discussing the pros and cons of umbrella policies, and how they applied to EV owners. It turns out, there's a lot to consider when deciding whether to opt for extra liability coverage.

What's the Point of an Umbrella Policy for EV Owners?

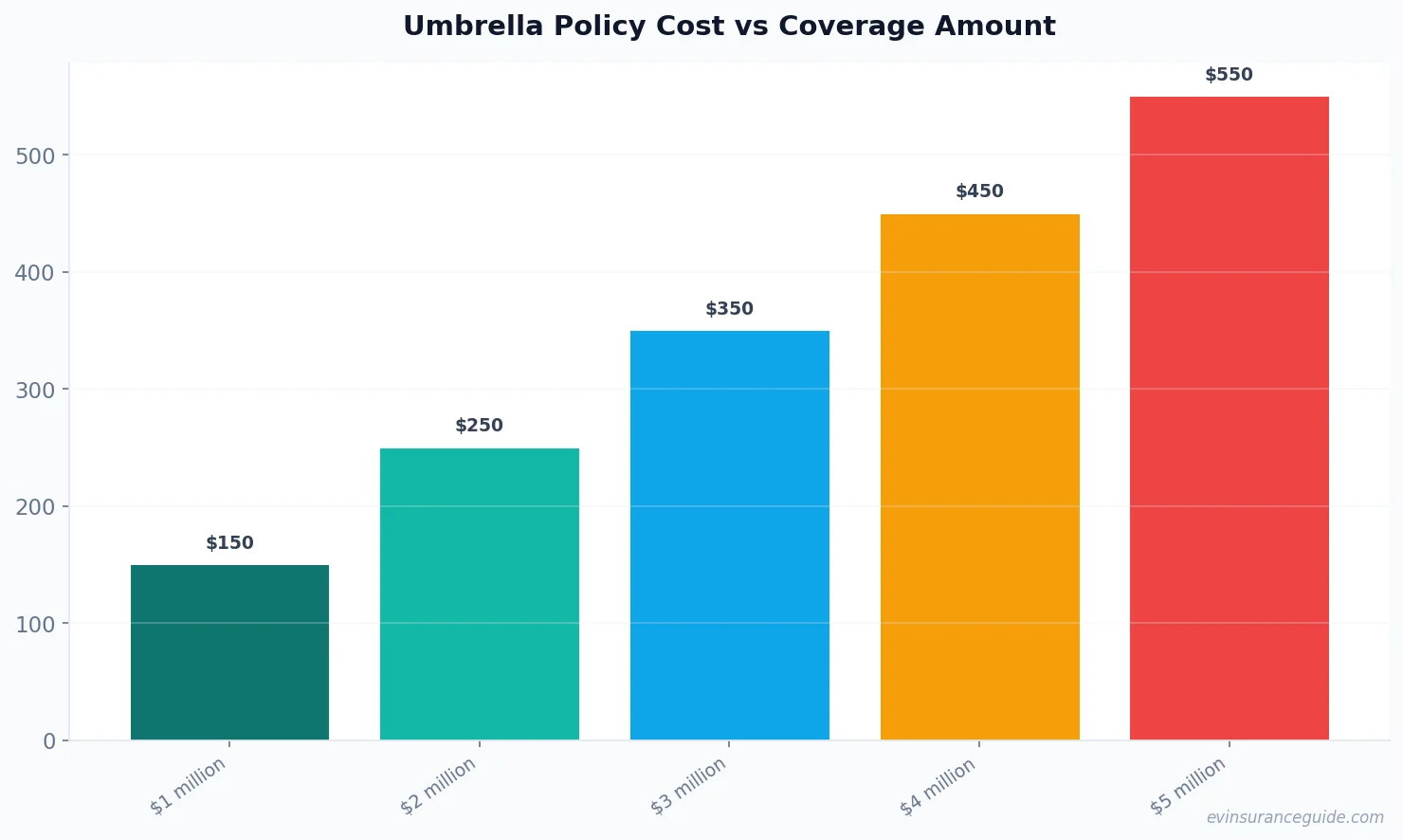

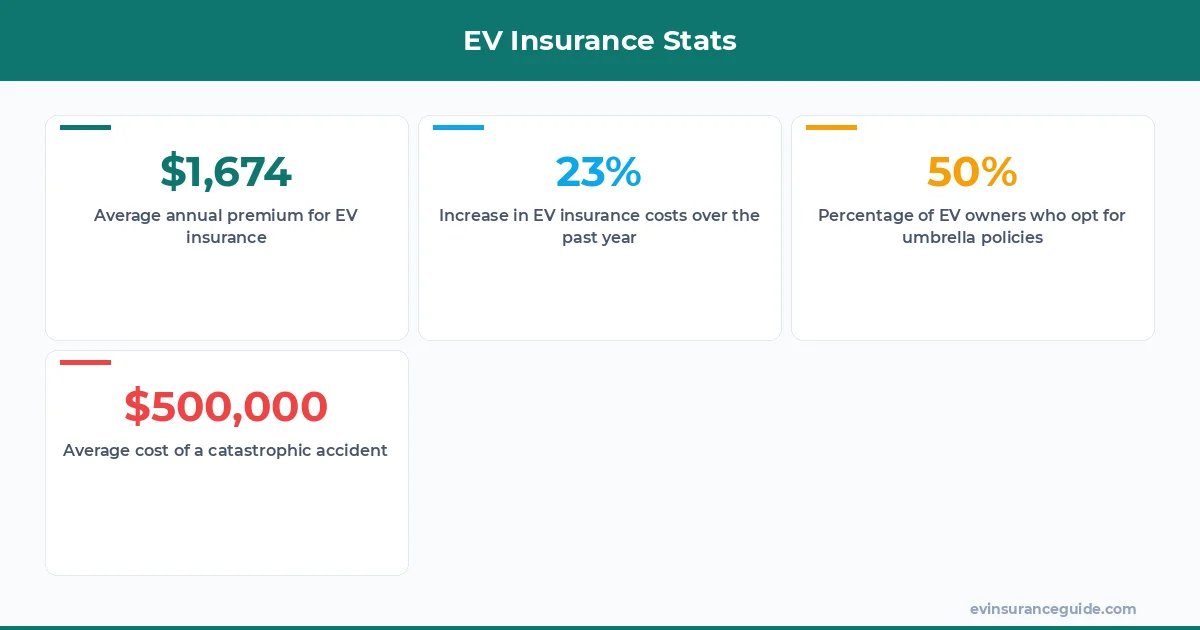

An umbrella policy provides extra liability coverage, usually in the range of $1 million to $5 million, to protect EV owners from financial ruin in case of a catastrophic accident. It's not just for the wealthy; anyone can benefit from the added peace of mind. Consider this: if you're involved in a serious accident, and your regular insurance only covers $300,000 of the damages, you'll be on the hook for the remaining amount. Ouch.

For example, let's say you own a Rivian R1T, and you're involved in an accident that causes $500,000 in damages. Your regular insurance, provided by Geico, only covers $300,000. Without an umbrella policy, you'd be responsible for the remaining $200,000. That's a pretty big hit to take.

But, with an umbrella policy, you'd be covered for the excess amount, up to the policy limits. It's worth noting that umbrella policies often come with a deductible, which can range from $250 to $1,000. So, it's essential to factor that into your decision.

OK So Here's the Deal With EV Lease vs Buy Insurance

When it comes to EV lease vs buy insurance, things get a bit more complicated. If you're leasing an EV, like Mike, you might not need an umbrella policy, since the lease agreement usually includes some level of insurance coverage. However, if you're buying an EV outright, like Rachel, an umbrella policy could be a good idea, especially if you have significant assets to protect.

For instance, if you're leasing a Hyundai Ioniq 5, your lease agreement with Hyundai Motor Finance might include a $300,000 liability coverage limit. In that case, an umbrella policy might not be necessary. But, if you're buying a Tesla Model Y, and you've got a net worth of $500,000, an umbrella policy could provide valuable protection.

Well, actually, it's not that simple. There are many factors to consider, including the type of EV you own, your driving history, and your financial situation. And, let's not forget about the cost. Umbrella policies can range from $150 to $500 per year, depending on the provider and the coverage limits.

Is an Umbrella Policy Like Having a Spare Tire for Your EV?

In a way, yes. An umbrella policy is like having a spare tire for your EV — it's there to protect you in case of an emergency. But, just like a spare tire, it's not something you hope to use every day. It's a precautionary measure, designed to give you peace of mind and protect your assets.

Consider this: according to a study by the National Highway Traffic Safety Administration (NHTSA), the average cost of a car accident is around $136,000. That's a pretty big hit to take, especially if you're not prepared.

But, with an umbrella policy, you can rest easy knowing that you're protected in case of a catastrophic accident. And, it's not just about the financial protection — it's also about the emotional peace of mind.

For example, let's say you're involved in a serious accident, and your umbrella policy covers the excess damages. You'll be able to focus on recovering from the accident, rather than worrying about how you'll pay for the damages.

5 Reasons to Consider an Umbrella Policy for Your EV

If you're still on the fence about whether to get an umbrella policy for your EV, here are five reasons to consider:

- 1. Extra liability coverage: An umbrella policy provides extra liability coverage, usually in the range of $1 million to $5 million, to protect EV owners from financial ruin in case of a catastrophic accident.

- 2. Protection for your assets: If you have significant assets, such as a house or investments, an umbrella policy can help protect them in case of a lawsuit.

- 3. Peace of mind: Knowing that you have an umbrella policy can give you peace of mind, especially if you're driving a high-value EV like a Tesla or a Rivian.

- 4. Flexibility: Umbrella policies can be tailored to fit your specific needs and budget.

- 5. Cost-effective: Umbrella policies can be relatively affordable, with premiums ranging from $150 to $500 per year.

A Story of How an Umbrella Policy Saved the Day

I'd like to share a story about a friend of mine, who we'll call Emily. Emily owns a Tesla Model S, and she's a bit of a reckless driver. One day, she was involved in a serious accident on the highway, and her Tesla was totaled. The other driver was seriously injured, and Emily was found to be at fault.

Luckily, Emily had an umbrella policy, which covered the excess damages and medical expenses. Without it, she would have been on the hook for hundreds of thousands of dollars.

As Emily would say, > Having an umbrella policy is like having a safety net — it's there to catch you when you fall. And, trust me, it's worth every penny.

That's a pretty compelling argument, if you ask me.

FAQs

#### What is an umbrella policy?

An umbrella policy is a type of insurance that provides extra liability coverage, usually in the range of $1 million to $5 million, to protect EV owners from financial ruin in case of a catastrophic accident.

#### How much does an umbrella policy cost?

The cost of an umbrella policy can range from $150 to $500 per year, depending on the provider and the coverage limits.

#### Do I need an umbrella policy if I'm leasing an EV?

It depends on the lease agreement and the level of insurance coverage provided by the lessor. If you're leasing an EV, you might not need an umbrella policy, but it's always a good idea to check your lease agreement and consult with an insurance expert.

#### Can I bundle my umbrella policy with my regular insurance?

Yes, many insurance providers offer bundled deals that include an umbrella policy. It's always a good idea to shop around and compare prices to find the best deal.

#### How do I choose the right umbrella policy for my EV?

To choose the right umbrella policy for your EV, you should consider factors such as the type of EV you own, your driving history, and your financial situation. It's also a good idea to consult with an insurance expert and read reviews from other customers.

#### What is the difference between an umbrella policy and a regular insurance policy?

An umbrella policy provides extra liability coverage, usually in the range of $1 million to $5 million, to protect EV owners from financial ruin in case of a catastrophic accident. A regular insurance policy, on the other hand, provides coverage for damages and injuries up to a certain limit, usually $300,000.

Go get yourself a better quote. You deserve it. — Alex