Last Tuesday, a guy named Marcus emailed me asking why his Ioniq 5 quote jumped 40%. He'd just financed the car and was already facing a higher insurance premium. Sound familiar? I've seen this happen to plenty of EV owners, especially those who don't fully understand how gap insurance works.

A Story of Depreciation and Woe

Marcus had bought his Ioniq 5 for $45,000, but just a year later, the car's value had dropped to $32,000. That's a 29% depreciation hit. Now, if Marcus were to total his car, his insurance would only cover the current market value – leaving him with a $13,000 gap to pay off the loan. Know what the kicker is? This isn't an isolated incident. EVs depreciate faster than their gas-guzzling counterparts, making gap insurance a must-have for many owners.

You see, EVs like the Tesla Model 3 and BMW iX are still relatively new to the market, so their resale values are harder to predict. This unpredictability, combined with the high upfront costs of EVs, creates a perfect storm of depreciation. And let's not forget the Rivian – a $70,000+ vehicle that's prone to even more drastic depreciation due to its premium price point.

Wild, right? The fact that these cars can lose so much value in just a few years is a harsh reality check for many owners. But here's the thing: gap insurance can help mitigate this risk. By covering the difference between the car's actual cash value and the outstanding loan balance, gap insurance gives EV owners a financial safety net.

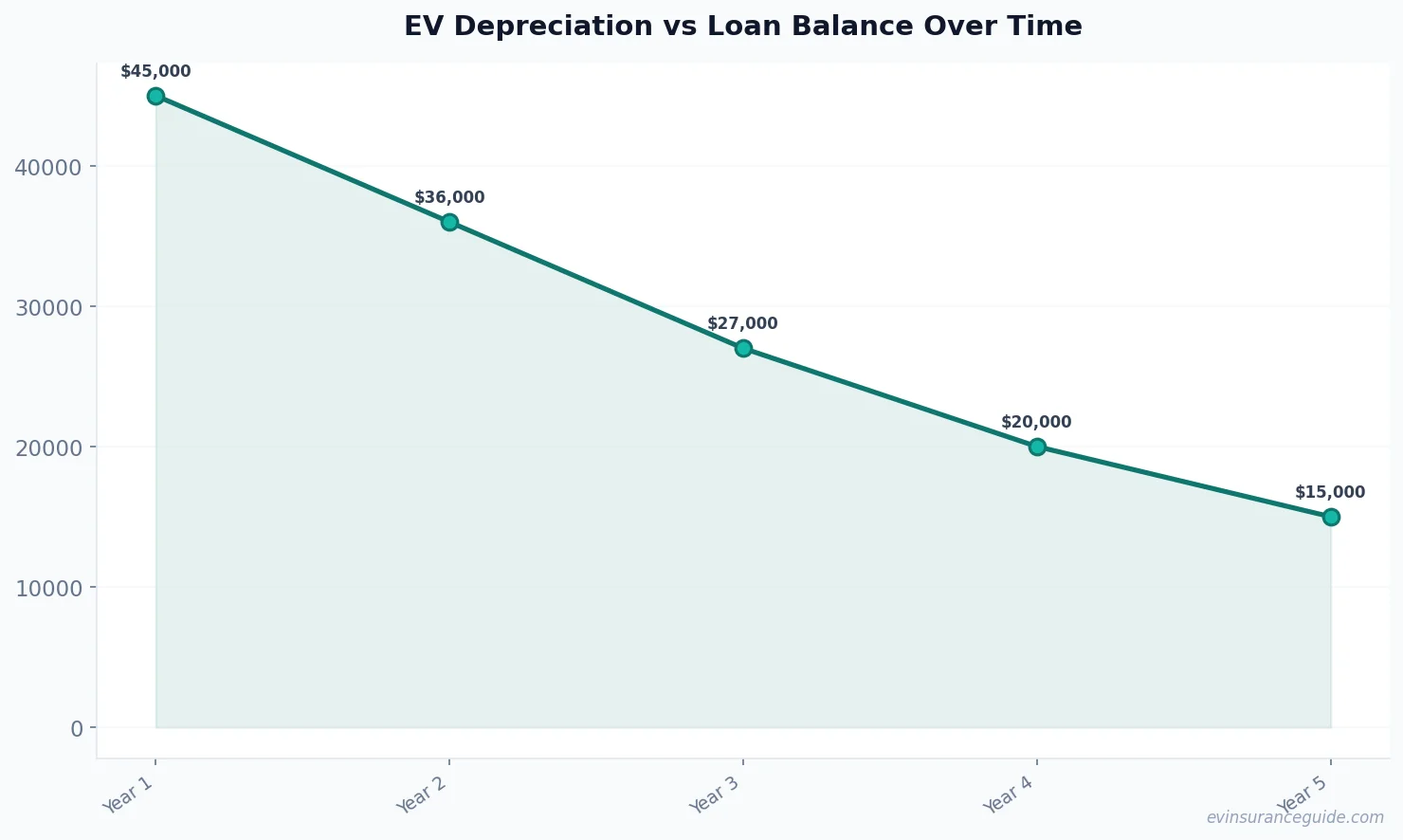

5 Years of EV Depreciation Data

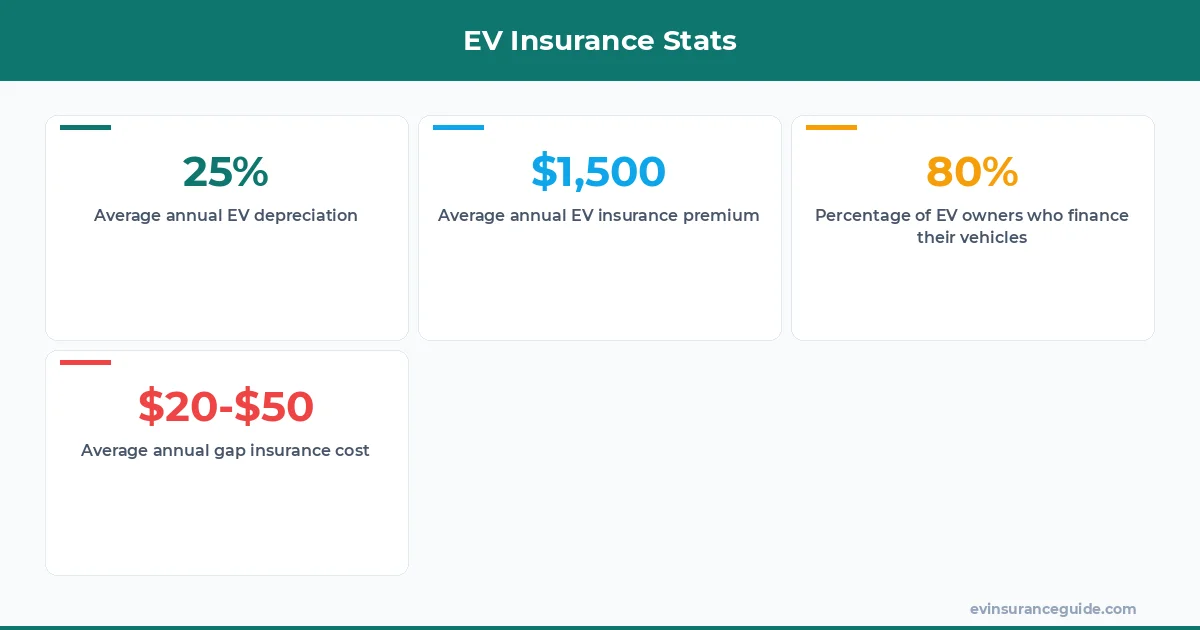

Looking at the numbers, it's clear that EV depreciation is a major concern. Over the past 5 years, we've seen an average annual depreciation of 20-25% for many EV models. That's compared to 10-15% for gas-powered cars. This disparity is largely due to the rapid advancements in EV technology, which can make older models seem outdated and less desirable.

For instance, the Hyundai Ioniq 5 has seen a significant price drop since its release, with some trim levels losing up to 30% of their value within the first year. This kind of depreciation can be devastating for owners who are still paying off their loans. That's where gap insurance comes in – to fill the gap between the car's actual value and the loan balance.

Now, I know what you're thinking: 'Isn't gap insurance just an added expense?' Well, actually, it's a necessary evil for many EV owners. The cost of gap insurance can range from $20 to $50 per year, depending on the provider and the vehicle. It's a small price to pay for the peace of mind that comes with knowing you're protected against depreciation.

OK So Here's the Deal With EV Road Trip Insurance

If you're planning an EV road trip, you need to consider the insurance implications. EV road trip insurance is a specialized type of coverage that takes into account the unique needs of electric vehicle owners. It often includes gap insurance, roadside assistance, and other perks that can make your trip more enjoyable and stress-free.

But here's the thing: not all EV road trip insurance policies are created equal. Some providers, like Geico and Progressive, offer more comprehensive coverage options than others. You'll want to shop around and compare rates to find the best policy for your needs. And don't even get me started on the importance of reading the fine print – you don't want any surprises down the line.

For example, let's say you're planning a cross-country road trip in your Tesla Model Y. You'll want to make sure your insurance policy covers you in case of an emergency, whether it's a flat tire or a totaled car. EV road trip insurance can provide that extra layer of protection, giving you the freedom to enjoy your trip without worrying about the what-ifs.

Pro tip: When shopping for EV road trip insurance, look for policies that include gap insurance, roadside assistance, and rental car coverage. These perks can save you a fortune in the long run.

Honestly, Gap Insurance is a No-Brainer

I'm gonna be blunt: if you own an EV, you need gap insurance. It's not just a nicety; it's a necessity. The cost of gap insurance is a small fraction of the overall cost of owning an EV, and the peace of mind it provides is priceless.

But don't just take my word for it. Let's look at some numbers. According to a recent study, the average EV owner can expect to pay around $1,500 per year in insurance premiums. That's compared to around $1,200 for gas-powered cars. However, with gap insurance, you can avoid paying out of pocket for depreciation-related losses.

And let's not forget about the environmental benefits of EVs. With the increasing focus on sustainability, EVs are becoming more popular by the day. But as the demand for EVs grows, so does the risk of depreciation. That's why gap insurance is crucial for EV owners who want to protect their investment.

Busting the Myth That Gap Insurance is a Waste of Money

One common myth about gap insurance is that it's a waste of money. But the truth is, gap insurance can save you thousands of dollars in the long run. By covering the difference between the car's actual cash value and the outstanding loan balance, gap insurance gives EV owners a financial safety net.

For instance, let's say you buy a Rivian for $80,000 and finance the entire amount. If the car depreciates by 30% within the first year, you'll be left with a $24,000 gap to pay off the loan. Without gap insurance, you'll be on the hook for that amount. But with gap insurance, you'll be covered – and that's a huge relief.

So, the next time someone tells you that gap insurance is a waste of money, you can set them straight. It's a vital component of EV ownership, and it can save you a fortune in the long run.

FAQs

#### What is gap insurance, and how does it work?

Gap insurance is a type of insurance that covers the difference between the car's actual cash value and the outstanding loan balance. It's designed to protect EV owners from depreciation-related losses. The cost of gap insurance can range from $20 to $50 per year, depending on the provider and the vehicle.

#### How much does EV road trip insurance cost?

The cost of EV road trip insurance varies depending on the provider and the level of coverage. On average, you can expect to pay around $100 to $300 per year for a basic policy. However, more comprehensive policies can cost upwards of $500 to $1,000 per year.

#### Do all EV owners need gap insurance?

Not all EV owners need gap insurance, but it's highly recommended for those who finance their vehicles. If you pay cash for your EV or have a low loan balance, you may not need gap insurance. However, if you have a high loan balance or are concerned about depreciation, gap insurance can provide valuable protection.

#### Can I buy gap insurance from any insurance provider?

No, not all insurance providers offer gap insurance. You'll need to shop around to find a provider that offers this type of coverage. Some popular providers, like Geico and Progressive, offer gap insurance as an add-on to their standard policies.

#### How do I know if I have gap insurance?

Check your insurance policy documents to see if you have gap insurance. If you're not sure, contact your insurance provider to ask about their gap insurance options.

#### What's the difference between gap insurance and comprehensive insurance?

Gap insurance and comprehensive insurance are two separate types of coverage. Comprehensive insurance covers damages to your vehicle, while gap insurance covers the difference between the car's actual cash value and the outstanding loan balance.

#### Is gap insurance worth the cost?

Yes, gap insurance is worth the cost for many EV owners. The cost of gap insurance is a small fraction of the overall cost of owning an EV, and the peace of mind it provides is priceless.

The best policy is the one you actually understand. — Alex