So, I've got a friend, let's call her Rachel. She used to have a gas-guzzler, but then she switched to a brand-new Tesla Model 3. She was thrilled, and I was thrilled for her. But here's the thing: she was still paying an arm and a leg for insurance. I mean, we're talking over $2,500 a year. She was with some big-name insurer, and they were taking her for a ride. Then, she switched to a new insurer that specialized in EVs, and her premium dropped to $1,800. That's a $700 difference, just like that. And the best part? Her new policy had better coverage, including a more comprehensive ev total loss insurance payout.

MYTH_BUST — You Don't Need Gap Insurance for Your EV

Know what the kicker is? Most people think gap insurance is only for brand-new cars, but that's not entirely true. If you're financing or leasing an EV, gap insurance can be a lifesaver. I mean, let's say you get into an accident, and your EV is totaled. The insurer will only pay out the actual cash value (ACV) of your vehicle, which is usually lower than the purchase price. That's where gap insurance comes in – it covers the difference between the ACV and the amount you still owe on your loan or lease. For example, if you purchased a Tesla Model Y for $60,000, and it's only worth $40,000 after two years, gap insurance will cover the $20,000 difference. Wild, right? You don't want to be stuck paying off a loan for a car that's no longer on the road.

But, and this is a big but, gap insurance can be pricey. I've seen policies that cost upwards of $500 per year. That's why it's essential to shop around and compare rates from different insurers. You might be surprised at how much you can save. For instance, I found a policy from Geico that cost $200 per year, while a similar policy from State Farm cost $400. That's a $200 difference, just for doing your research. Dead serious, it's worth the effort.

What Counts as Total Loss for EVs?

So, what exactly counts as a total loss for EVs? Well, it's not as simple as you might think. In most states, if the repair cost exceeds 50-80% of the vehicle's value, it's considered a total loss. But, that threshold can vary depending on the state and the insurer. For example, in California, the threshold is 70%, while in Texas, it's 100%. Yep, you read that right – in Texas, the insurer will only declare a total loss if the repair cost exceeds the vehicle's value. That's why it's crucial to check your policy and understand the specifics.

Let's say you own a Hyundai Ioniq 5, and you get into a fender bender. The repair cost comes out to be $15,000, but the vehicle's value is only $20,000. In California, that would be considered a total loss, and the insurer would pay out the ACV of the vehicle. But, in Texas, the insurer might try to repair the vehicle instead of declaring it a total loss. That's why it's essential to have a good understanding of your policy and the laws in your state.

COMPARISON — EV Total Loss Payout vs Gas-Powered Vehicles

Now, let's compare ev total loss insurance payout to gas-powered vehicles. I mean, which one gets a better deal? Well, it's not exactly a fair comparison, since EVs tend to have higher purchase prices. But, if we look at the data, EVs actually have a lower total loss frequency than gas-powered vehicles. According to a study by the National Highway Traffic Safety Administration (NHTSA), EVs have a total loss frequency of 1.4%, compared to 2.1% for gas-powered vehicles. That's a 33% difference, which is significant.

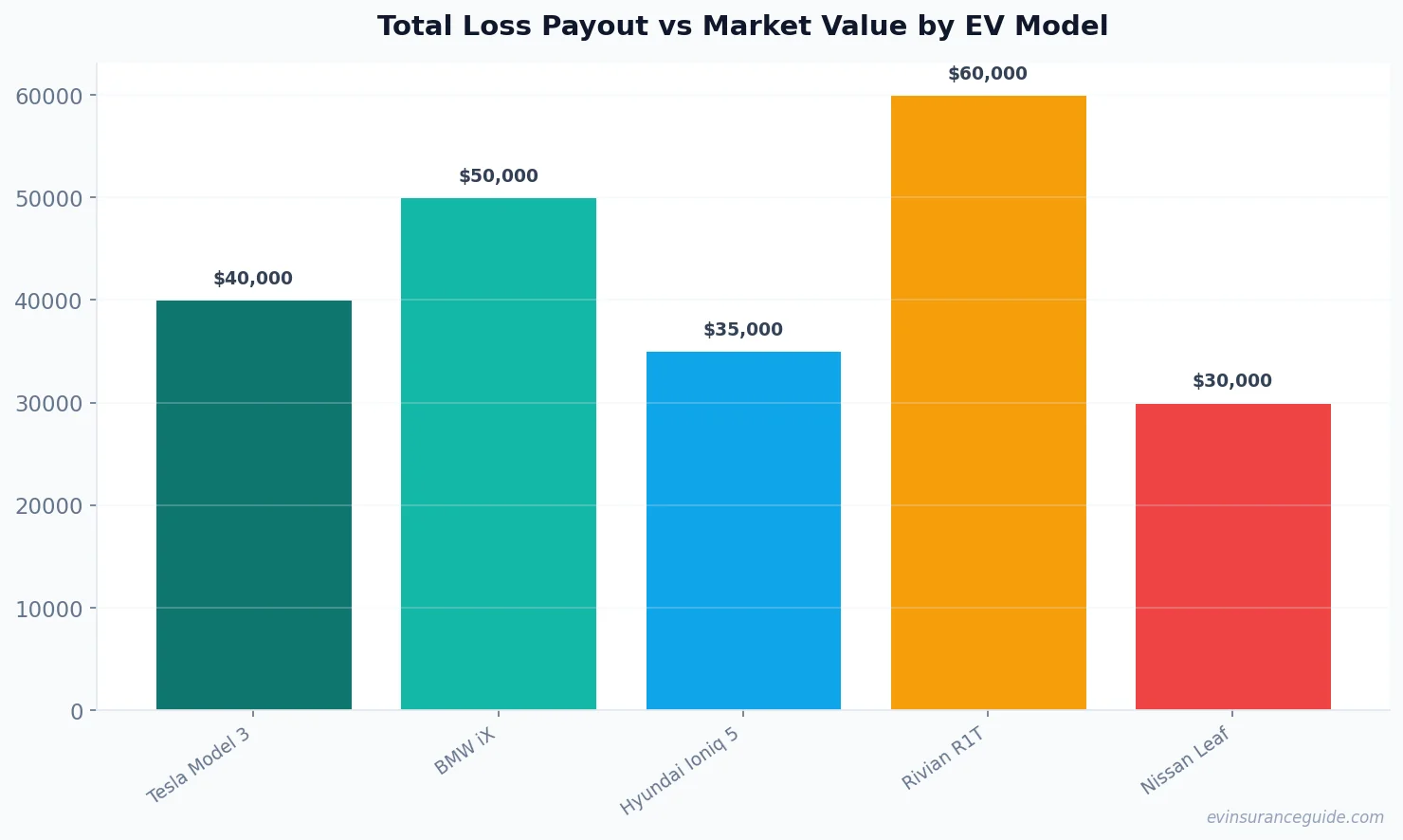

But, here's the thing: EVs tend to have higher repair costs. I mean, those batteries aren't cheap to replace. So, even if the total loss frequency is lower, the payout can still be higher for EVs. For example, if a Tesla Model 3 is totaled, the insurer might pay out $40,000, while a similar gas-powered vehicle might only get $30,000. That's a $10,000 difference, which is nothing to sneeze at.

WARNING — Don't Get Caught Off Guard with Low EV Total Loss Payout

Know what the worst part is? Some insurers will try to lowball you on the ev total loss insurance payout. I mean, they'll give you a payout that's lower than the actual value of your vehicle. That's why it's essential to do your research and understand the market value of your EV. You can use tools like Kelley Blue Book or NADAguides to determine the value of your vehicle. And, if you're not happy with the payout, don't be afraid to negotiate.

For instance, if you own a Rivian R1T, and the insurer offers you $50,000, but you know it's worth $60,000, you can negotiate for a higher payout. You can provide evidence of the vehicle's condition, maintenance records, and even get an independent appraisal. That's why it's crucial to have all the necessary documents and information ready.

7 Things to Know About EV Total Loss Payout Process

So, what's the process like for ev total loss insurance payout? Well, here are 7 things you need to know:

- 1. The average payout process takes 2-4 weeks, but it can vary depending on the insurer and the complexity of the claim.

- 2. You'll need to provide documentation, including the vehicle's title, registration, and proof of insurance.

- 3. The insurer will send an adjuster to assess the damage and determine the total loss payout.

- 4. You can negotiate the payout, but you'll need to provide evidence to support your claim.

- 5. The payout will be based on the actual cash value (ACV) of the vehicle, which is usually lower than the purchase price.

- 6. You may be eligible for additional compensation, such as rental car coverage or towing costs.

- 7. It's essential to review your policy and understand the specifics of the ev total loss insurance payout process.

FAQs

#### What is the average ev total loss insurance payout?

The average ev total loss insurance payout varies depending on the vehicle's make, model, and year. However, according to data from the Insurance Institute for Highway Safety (IIHS), the average payout for EVs is around $35,000.

#### How long does the ev total loss insurance payout process take?

The average payout process takes 2-4 weeks, but it can vary depending on the insurer and the complexity of the claim.

#### Can I negotiate the ev total loss insurance payout?

Yes, you can negotiate the payout, but you'll need to provide evidence to support your claim. This can include documentation of the vehicle's condition, maintenance records, and even an independent appraisal.

#### What is the difference between ACV and replacement cost?

The actual cash value (ACV) is the vehicle's value at the time of the loss, while the replacement cost is the cost of replacing the vehicle with a new one. The replacement cost is usually higher than the ACV.

#### Do I need gap insurance for my EV?

If you're financing or leasing an EV, gap insurance can be a lifesaver. It covers the difference between the ACV and the amount you still owe on your loan or lease.

#### How do I determine the market value of my EV?

You can use tools like Kelley Blue Book or NADAguides to determine the market value of your EV. You can also get an independent appraisal or check the prices of similar vehicles in your area.

#### Can I get a higher ev total loss insurance payout if I have a good driving record?

Yes, having a good driving record can help you get a higher payout. Insurers often offer better rates and higher payouts to drivers with clean records.

Pro tip: Always keep detailed records of your vehicle's maintenance and condition. This can help you negotiate a higher ev total loss insurance payout if your vehicle is ever totaled.

And, let me tell you, it's not just about the payout. It's about the process, the hassle, the stress. That's why it's essential to have a good insurer, one that'll work with you to get you the best deal possible. I mean, you don't want to be stuck with an insurer that's gonna lowball you or make you jump through hoops. You want an insurer that's gonna have your back, that's gonna help you get back on the road as quickly and easily as possible.

So, what's the takeaway? EV total loss insurance payout can be a complex and frustrating process, but it doesn't have to be. By understanding the process, knowing your rights, and having the right insurer, you can get the best deal possible. And, if you're not happy with the payout, don't be afraid to negotiate. You got this.

Drive safe out there.