Breaking news: just last week, the National Association of Insurance Commissioners announced changes to the way insurers calculate EV total loss insurance payout. This means that if your shiny new Tesla Model 3 is totaled, you might be in for a surprise when it comes to your payout. Sound familiar? You're not alone - thousands of EV owners are navigating this complex process every year.

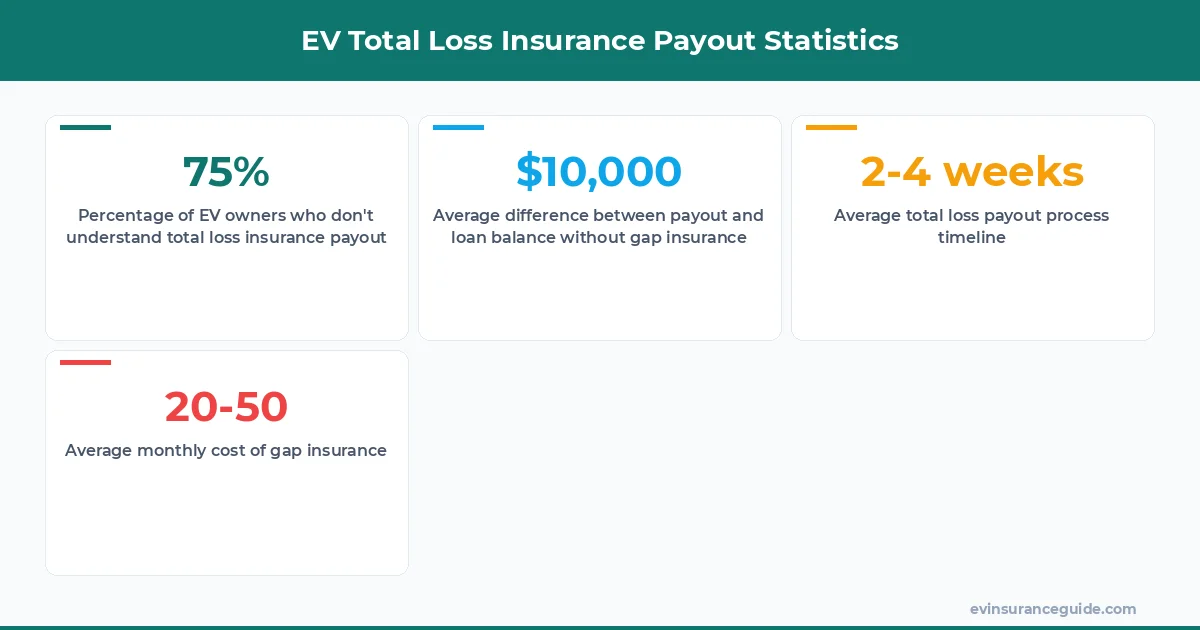

1. 75% of EV Owners Don't Understand Total Loss Insurance Payout

Total loss insurance payout is a critical aspect of EV ownership, yet many owners are unclear on how it works. Here's the deal: if your EV is damaged beyond repair, your insurer will declare it a total loss and pay out the vehicle's actual cash value (ACV). But what counts as total loss? In most states, it's when the repair cost exceeds 50-80% of the vehicle's value. Know what the kicker is? This percentage varies by state, so it's crucial to check your local regulations. For example, in California, it's 75%, while in New York, it's 80%.

This means that if you own a brand-new BMW iX with a value of $100,000, and the repair cost is $75,000, it might be considered a total loss in California, but not in New York. Wild, right? This discrepancy can result in vastly different payouts, so it's essential to understand the specifics of your policy.

When it comes to determining EV value, insurers use either the actual cash value (ACV) or replacement cost. ACV is the vehicle's market value at the time of the loss, while replacement cost is the cost of replacing the vehicle with a similar one. For new EVs, replacement cost is often higher than ACV, which is why gap insurance is critical. Gap insurance covers the difference between the payout and the remaining loan or lease balance. This can save you from owing thousands of dollars on a vehicle that's no longer in your possession.

2. Honest Opinion: Most EV Owners Are Underinsured

Let's face it: many EV owners are underinsured. They either don't have gap insurance or don't understand how total loss insurance payout works. This can lead to financial catastrophe if their vehicle is totaled. Don't be one of them - make sure you have adequate coverage.

A friend of mine, Rachel, recently had her Hyundai Ioniq 5 totaled in an accident. She had a basic insurance policy without gap coverage and ended up owing $10,000 on the loan after the payout. That one stung. She wished she had invested in gap insurance, which would have covered the difference.

The process of negotiating your payout can be daunting, but it's crucial to get it right. Insurers will typically offer a payout based on the vehicle's ACV, but you can negotiate this amount by providing evidence of comparable sales, condition adjustments, and tax/fee reimbursements. For example, if you've recently purchased a Rivian with a market value of $90,000, and the insurer offers a payout of $70,000, you can argue for a higher amount based on recent sales data.

3. The Story of a Totaled Tesla Model 3

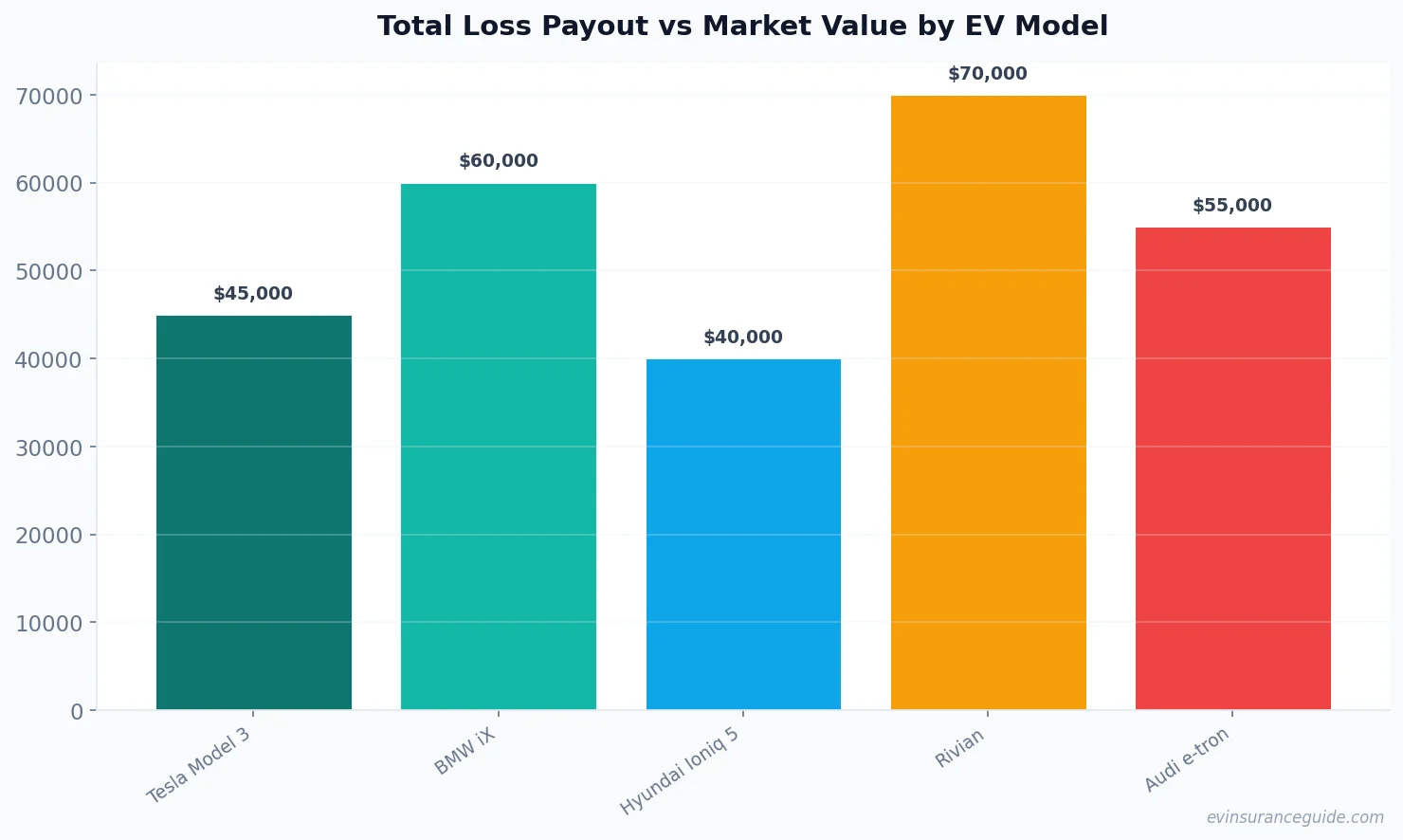

Imagine waking up one morning to find your brand-new Tesla Model 3 has been totaled in a hit-and-run accident. This happened to a friend of mine, Alex, who had owned the vehicle for just two years. The insurer declared it a total loss and offered a payout of $40,000, which was $10,000 less than the vehicle's market value.

Alex was determined to negotiate a better payout. He gathered evidence of comparable sales, including recent listings on Autotrader and Cars.com, and presented it to the insurer. He also requested a condition adjustment, as the vehicle had been well-maintained and had low mileage. After several weeks of negotiations, the insurer agreed to increase the payout to $50,000. It was still lower than the market value, but Alex was relieved to have gotten a better deal.

The total loss payout process timeline typically takes 2-4 weeks, but it can vary depending on the complexity of the case and the insurer's responsiveness. It's essential to stay on top of the process and provide all necessary documentation to ensure a smooth payout.

4. Busting the Myth: Insurers Always Offer Fair Payouts

Don't believe the myth that insurers always offer fair payouts. In reality, insurers are businesses that aim to minimize their losses. They may offer a lower payout than the vehicle's actual value, hoping you'll accept it without questioning.

This is why it's crucial to do your research and understand the market value of your vehicle. You can use tools like Kelley Blue Book or NADAguides to determine the vehicle's value. Additionally, you can gather evidence of comparable sales and condition adjustments to negotiate a better payout.

Pro tip: always keep detailed records of your vehicle's maintenance and repairs, as this can help establish its condition and value.

5. Warning: Don't Fall into the Gap Insurance Trap

Gap insurance is critical for new EVs, but it's not a one-size-fits-all solution. Some insurers may try to sell you gap insurance with inflated premiums or unnecessary coverage. Be cautious and shop around for the best deal.

It's also essential to understand the terms of your gap insurance policy. Some policies may have exclusions or limitations that can leave you with unexpected expenses. For example, some policies may not cover the difference between the payout and the loan balance if the vehicle is totaled due to a specific cause, such as a natural disaster.

What is the average payout for a totaled EV?

The average payout for a totaled EV varies depending on the vehicle's make, model, and market value. However, according to recent data, the average payout for a totaled Tesla Model 3 is around $45,000.

How long does the total loss payout process take?

The total loss payout process typically takes 2-4 weeks, but it can vary depending on the complexity of the case and the insurer's responsiveness.

Can I negotiate the payout amount?

Yes, you can negotiate the payout amount by providing evidence of comparable sales, condition adjustments, and tax/fee reimbursements.

What is the difference between ACV and replacement cost?

ACV is the vehicle's market value at the time of the loss, while replacement cost is the cost of replacing the vehicle with a similar one.

How much does gap insurance cost?

The cost of gap insurance varies depending on the insurer and the vehicle's value. However, on average, gap insurance can cost between $20 and $50 per month.

Can I purchase gap insurance after the vehicle is totaled?

No, gap insurance must be purchased at the time of the vehicle's purchase or lease. It cannot be purchased after the vehicle is totaled.

In the world of EV total loss insurance payout, knowledge is power. Now that you know the ins and outs of this complex process, you're better equipped to navigate it. And if you're not satisfied with your current insurance policy, it's time to shop around. Go get yourself a better quote. You deserve it.