Last Tuesday, a guy named Marcus emailed me asking why his Ioniq 5 quote jumped 40%. He'd upgraded from a gas-guzzler to this sleek Hyundai EV, expecting a similar insurance rate. Nope. The insurer quoted him $2,300/year – a whopping $800 more than his old car. Sound familiar? You buy an EV, thinking you're saving the planet and some cash, only to get slammed with higher insurance premiums. Know what the kicker is? It's not just the car's eco-friendliness that affects the rate – it's the performance.

HONEST_OPINION: EV vs Gas Insurance Cost is a Wild Ride

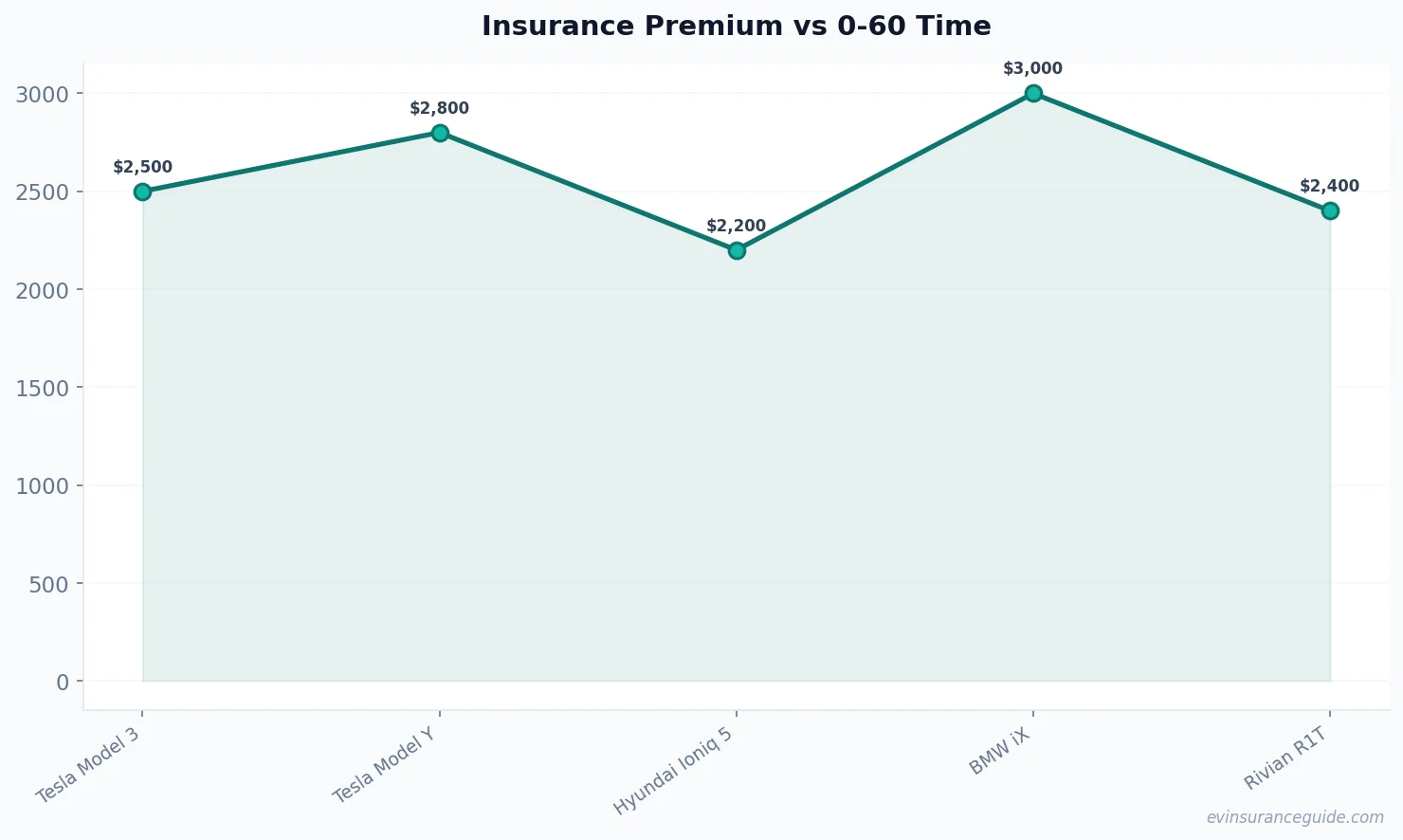

The EV vs gas insurance cost debate is heated, and for good reason. Insurers are still figuring out how to price these new, high-tech vehicles. That's why you'll see such a huge range in quotes – from $1,500 to $3,500/year for the same car model, depending on the insurer. Dead serious, some companies are overcharging EV owners by as much as 50%. Take the Tesla Model 3, for instance. Its 0-60 time is a blistering 3.2 seconds, which is music to enthusiasts' ears but a nightmare for insurers. They're gonna charge you more for that kind of performance – we're talking an extra $500-$700/year.

But here's the thing: not all EVs are created equal. The BMW iX, with its 516 horsepower, is a beast on the road. Insurers know this and will charge you accordingly – around $2,800/year, on average. On the other hand, the Rivian R1T, with its more modest 754 horsepower, might get a slightly better rate, around $2,400/year. Wild, right? The same car, different trims, different prices. And don't even get me started on the Hyundai Ioniq 5 – that car's a real mixed bag when it comes to insurance costs.

You see, insurers use a complex algorithm to determine your premium, taking into account factors like the car's make, model, year, and performance specs. They're also looking at your driving history, location, and other personal factors. So, when you're shopping for EV insurance, it's crucial to compare rates from multiple providers. You might find that one insurer is more EV-friendly than others, offering discounts for green vehicles or low-mileage drivers.

OK So Here's the Deal With EV Insurance Rates

OK, so you've decided to go electric, and you're wondering how your insurance rates will be affected. Well, actually, it's not all doom and gloom. Some insurers, like Geico and Progressive, offer discounts for EV owners – up to 10% off your annual premium. That's a nice chunk of change, especially if you're driving a high-performance EV like the Tesla Model Y. But, and this is a big but, these discounts are usually only available if you meet certain criteria, like driving less than 7,500 miles per year or having a clean driving record.

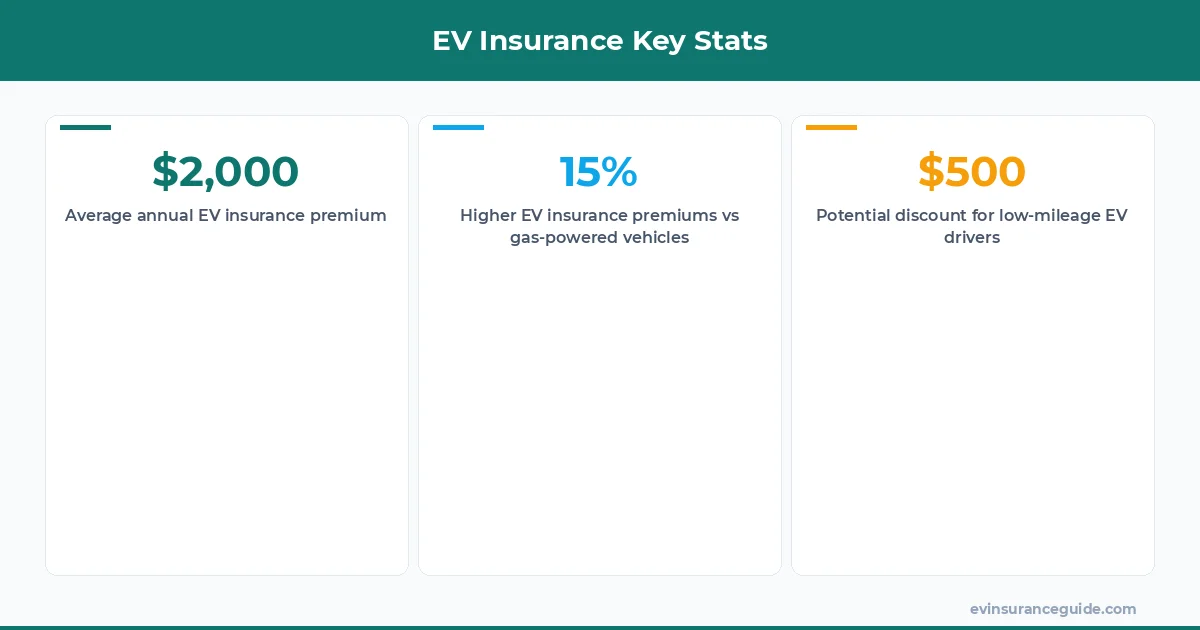

Now, let's talk about the cost of insuring an EV vs a gas-guzzler. On average, EV insurance premiums are around 15% higher than those for comparable gas-powered vehicles. That's because EVs are generally more expensive to repair or replace, and insurers factor this into their pricing. However, some studies suggest that EVs are actually safer than their gas-powered counterparts, with fewer accidents and lower claim rates. If insurers start to recognize this trend, we might see EV insurance rates decrease over time.

The key is to shop around, compare rates, and find an insurer that understands the unique needs of EV owners. Don't be afraid to negotiate, either – if you've got a good driving record and low mileage, you might be able to convince your insurer to give you a better deal. And, of course, there are always ways to reduce your premium, like installing a dash cam or taking a defensive driving course.

What Affects EV Insurance Premiums, Anyway?

So, what exactly affects EV insurance premiums? Is it just the car's 0-60 time, or are there other factors at play? Well, it's a combination of things, really. The car's make, model, and year are all important, as is its safety rating and performance specs. Insurers also look at your driving history, including any accidents or claims you've made in the past. And, of course, your location plays a role – if you live in an area with high crime rates or congested roads, your premium will likely be higher.

But, let's be real, the biggest factor is probably the car's performance. A car that can go from 0-60 in under 3 seconds is a recipe for disaster, at least in the eyes of insurers. They're gonna charge you more for that kind of power, and rightly so – it's just more likely to be involved in an accident. That one stung, right? I mean, who doesn't want a fast car? But, if you're willing to sacrifice a bit of speed for a lower premium, you might consider opting for a more modest EV model.

According to a study by the National Highway Traffic Safety Administration (NHTSA), EVs are involved in fewer accidents than gas-powered vehicles. However, when they do get into accidents, the repair costs are often higher due to the complex technology involved. This is something insurers are still grappling with, and it's reflected in the higher premiums for EV owners.

5 Key Factors That Determine Your EV Insurance Premium

Here are the top 5 factors that determine your EV insurance premium:

- 1. Car make, model, and year

- 2. Performance specs (0-60 time, horsepower, etc.)

- 3. Driving history and claims record

- 4. Location and garage address

- 5. Annual mileage and usage patterns

These factors all play a role in determining your premium, and insurers weigh them differently. For example, a driver with a spotless record and low mileage might get a better rate than someone with a few accidents on their record, even if they're driving the same car.

WARNING: Don't Get Caught Out by Hidden EV Insurance Costs

Be careful when shopping for EV insurance – there are some hidden costs you need to watch out for. Some insurers might charge you extra for things like roadside assistance or rental car coverage, which can add up quickly. And, of course, there are the usual suspects: comprehensive and collision coverage, which can be pricey for high-performance EVs.

But, the biggest trap to avoid is probably the 'EV surcharge'. Some insurers will slap you with an extra fee just for driving an EV, which can range from $200 to $500 per year. Know what the kicker is? This surcharge is often not explicitly stated in the policy documents, so you need to read the fine print carefully.

FAQs

#### What is the average cost of insuring an EV?

The average cost of insuring an EV is around $2,000/year, although this can vary widely depending on the make, model, and performance specs of the car.

#### Do all EVs have higher insurance premiums?

No, not all EVs have higher insurance premiums. Some models, like the Nissan Leaf, might have similar or even lower premiums than comparable gas-powered vehicles.

#### Can I get a discount on my EV insurance premium?

Yes, some insurers offer discounts for EV owners, especially if you meet certain criteria like driving less than 7,500 miles per year or having a clean driving record.

#### How does the 0-60 time affect EV insurance premiums?

The 0-60 time is a significant factor in determining EV insurance premiums. Cars with faster 0-60 times are generally considered higher-risk and will attract higher premiums.

#### What is the EV surcharge, and how can I avoid it?

The EV surcharge is an extra fee some insurers charge for driving an EV. To avoid it, you need to carefully review your policy documents and shop around for insurers that don't charge this fee.

#### Are EVs more expensive to repair than gas-powered vehicles?

Yes, EVs can be more expensive to repair than gas-powered vehicles, especially when it comes to complex components like the battery or electric motor.

Pro tip: when shopping for EV insurance, make sure to ask about any available discounts or promotions. Some insurers offer loyalty discounts or bundle deals that can save you hundreds of dollars per year.

That's all from me — go save some money. — Alex