Buying gap insurance for your new Tesla Model 3 can cost anywhere from $600 to $1,200 per year - but what if you're driving a BYD Tang, NIO ES6, or XPeng P7? That's where things get interesting. Sound familiar? You're not alone - thousands of EV owners are scratching their heads, trying to figure out why their insurance premiums are through the roof. Dead serious, it's like they're being punished for going green.

MYTH_BUST: Gap Insurance for Electric Cars is Always More Expensive

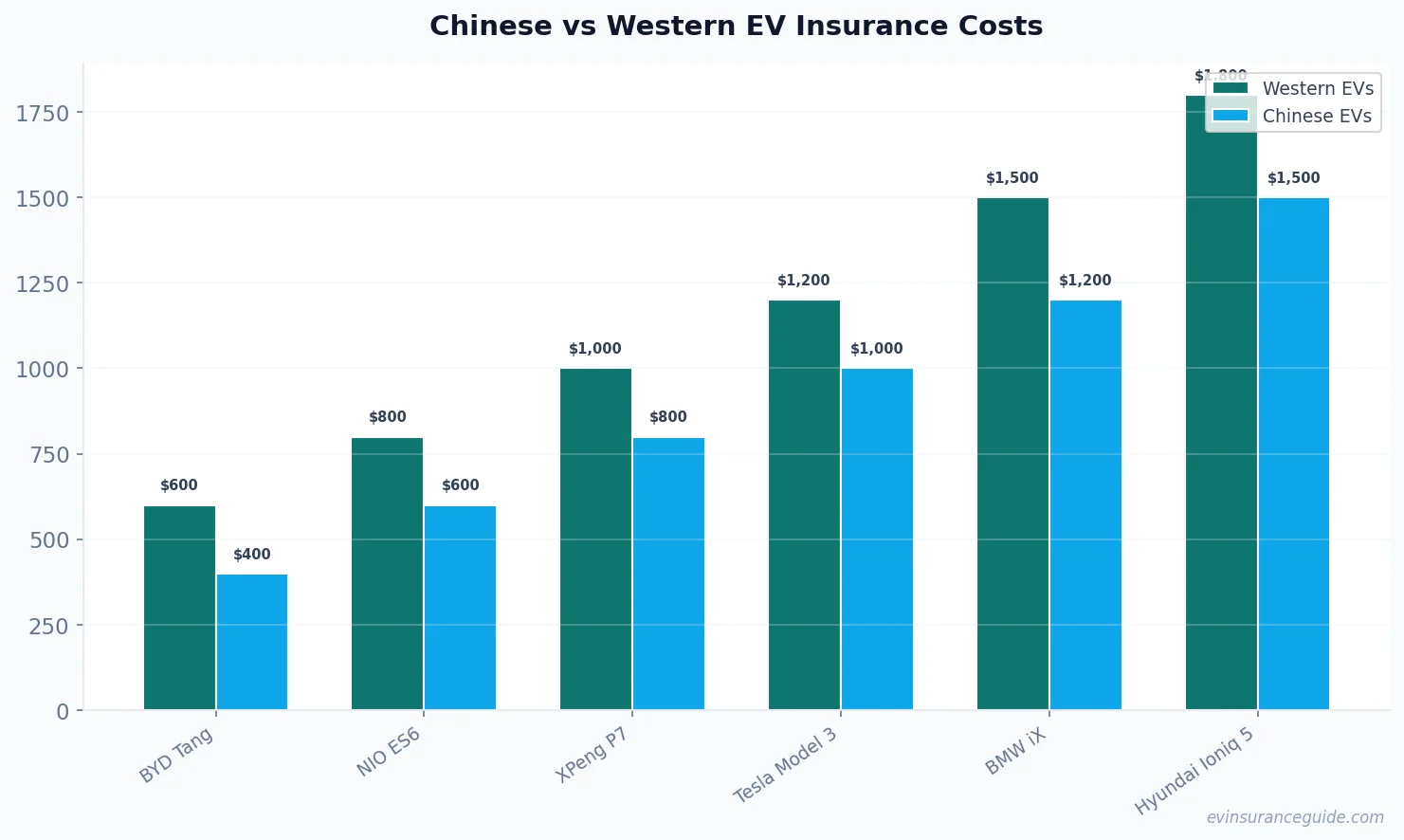

I've gotta bust a myth here: just because you're driving an electric car, doesn't mean you'll always pay more for gap insurance. In fact, some Chinese EVs like the BYD Han are actually cheaper to insure than their Western counterparts, like the BMW iX. Know what the kicker is? It's not just about the car - it's about the insurance company, too. Some providers, like GEICO, are offering specialized gap insurance for electric cars, with premiums starting at around $400 per year. That's a far cry from the $1,200 I mentioned earlier. Wild, right?

But here's the thing: not all Chinese EVs are created equal. The NIO ES8, for example, is a luxury EV with a price tag to match - and its insurance premiums reflect that. You're looking at around $1,500 per year for gap insurance, which is actually higher than some Western EVs, like the Hyundai Ioniq 5. That one stung, right? On the other hand, the XPeng G3 is a more affordable option, with gap insurance premiums starting at around $800 per year.

And don't even get me started on the Rivian R1T - that thing is a beast, and its insurance premiums are accordingly...beastly. You're looking at around $2,000 per year for gap insurance, which is downright ridiculous. But hey, at least you'll have the peace of mind knowing you're covered, right?

OK So Here's the Deal With Gap Insurance for Electric Cars

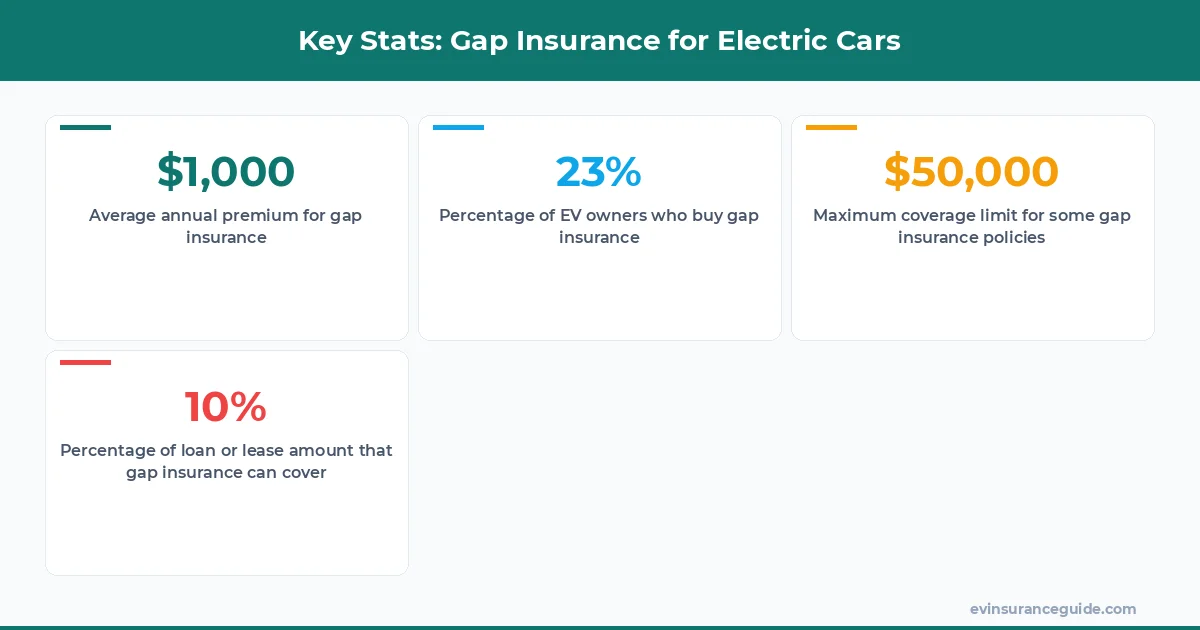

So, you wanna know the deal with gap insurance for electric cars? Well, it's pretty simple: gap insurance covers the difference between the actual cash value of your car and the amount you still owe on your loan or lease. For example, let's say you buy a new NIO ES6 for $70,000, and you put down 20% - that's $14,000. If you total the car, the insurance company will only pay out the actual cash value, which might be around $50,000. That leaves you with a gap of $20,000 - which is where gap insurance comes in. It's not required by law, but it's definitely a good idea, especially if you're financing or leasing your EV.

But here's the thing: not all gap insurance policies are created equal. Some providers, like State Farm, offer specialized gap insurance for electric cars, with coverage limits of up to $50,000. Others, like Allstate, offer more basic gap insurance policies with lower coverage limits. And then there are the Chinese EV manufacturers, like BYD and NIO, which are starting to offer their own gap insurance policies - with premiums that are often significantly lower than their Western counterparts.

Pro tip: always read the fine print on your gap insurance policy - you don't want to get stuck with a policy that doesn't cover what you think it does. For example, some policies might not cover the cost of a new battery, which can be a major expense for EV owners.

What Happens When You Total Your Chinese EV - Will Gap Insurance Cover You?

So, what happens when you total your Chinese EV - will gap insurance cover you? Well, it's not always a straightforward answer. Some insurance providers, like USAA, offer specialized gap insurance for electric cars that covers the full amount of the loan or lease - but only if you've had the policy for at least a year. Others, like Progressive, offer more basic gap insurance policies that only cover a percentage of the loan or lease. And then there are the Chinese EV manufacturers, which are starting to offer their own gap insurance policies with varying levels of coverage.

But here's the thing: gap insurance for electric cars is still a relatively new market, and there are a lot of unknowns. For example, what happens if you total your car and the insurance company says it's not covered under the policy? Or what if you need to replace a major component, like the battery or electric motor - will gap insurance cover that? These are all questions that you should be asking your insurance provider before you buy a policy.

And don't even get me started on the Hyundai Ioniq 5 - that thing is a game-changer, and its insurance premiums reflect that. You're looking at around $1,000 per year for gap insurance, which is actually lower than some Chinese EVs, like the XPeng P7. That's gotta make you wonder - what's the difference between these cars, and why are the insurance premiums so different?

How Do Chinese EVs Compare to Western EVs When it Comes to Gap Insurance

So, how do Chinese EVs compare to Western EVs when it comes to gap insurance? Well, it's a mixed bag. On the one hand, some Chinese EVs, like the BYD Tang, are actually cheaper to insure than their Western counterparts, like the Tesla Model Y. On the other hand, some Western EVs, like the BMW iX, are more expensive to insure than their Chinese counterparts, like the NIO ES6.

But here's the thing: it's not just about the car - it's about the insurance company, too. Some providers, like GEICO, are offering specialized gap insurance for electric cars that covers the full amount of the loan or lease - but only if you've had the policy for at least a year. Others, like Progressive, are offering more basic gap insurance policies that only cover a percentage of the loan or lease.

And then there's the Rivian R1T - that thing is a beast, and its insurance premiums reflect that. You're looking at around $2,500 per year for gap insurance, which is actually higher than some Chinese EVs, like the XPeng G3. That's gotta make you wonder - what's the difference between these cars, and why are the insurance premiums so different?

Being Honest About Gap Insurance for Electric Cars - It's Not Always a Good Deal

Being honest about gap insurance for electric cars - it's not always a good deal. I mean, think about it: if you're paying $1,000 per year for gap insurance, and you only owe $10,000 on your loan or lease, that's a pretty bad deal. You're essentially paying 10% of the loan or lease amount per year - which is ridiculous.

But here's the thing: gap insurance for electric cars is still a relatively new market, and there are a lot of unknowns. For example, what happens if you total your car and the insurance company says it's not covered under the policy? Or what if you need to replace a major component, like the battery or electric motor - will gap insurance cover that? These are all questions that you should be asking your insurance provider before you buy a policy.

And don't even get me started on the Tesla Model 3 - that thing is a game-changer, and its insurance premiums reflect that. You're looking at around $1,200 per year for gap insurance, which is actually higher than some Chinese EVs, like the BYD Han. That's gotta make you wonder - what's the difference between these cars, and why are the insurance premiums so different?

FAQs

#### What is gap insurance for electric cars?

Gap insurance for electric cars covers the difference between the actual cash value of your car and the amount you still owe on your loan or lease. It's not required by law, but it's definitely a good idea, especially if you're financing or leasing your EV.

#### How much does gap insurance for electric cars cost?

The cost of gap insurance for electric cars varies widely depending on the insurance provider, the type of car, and the loan or lease amount. On average, you can expect to pay between $600 and $1,200 per year for gap insurance.

#### Do all insurance providers offer gap insurance for electric cars?

No, not all insurance providers offer gap insurance for electric cars. Some providers, like GEICO and Progressive, offer specialized gap insurance for electric cars, while others do not.

#### Can I buy gap insurance for my used electric car?

Yes, you can buy gap insurance for your used electric car, but it may be more expensive than buying gap insurance for a new car. Some insurance providers, like State Farm, offer gap insurance for used cars, but the coverage limits may be lower than for new cars.

#### How do I know if I need gap insurance for my electric car?

If you're financing or leasing your electric car, you may need gap insurance to cover the difference between the actual cash value of the car and the amount you still owe on the loan or lease. You should also consider buying gap insurance if you've put down a low down payment or have a long loan or lease term.

#### Can I cancel my gap insurance policy at any time?

Yes, you can cancel your gap insurance policy at any time, but you may be subject to a penalty or cancellation fee. You should review your policy carefully before cancelling to make sure you understand the terms and conditions.

#### What are the benefits of buying gap insurance for my electric car?

The benefits of buying gap insurance for your electric car include peace of mind, financial protection, and the ability to avoid owing money on a totaled car. Gap insurance can also help you avoid financial hardship if you're involved in an accident or your car is stolen.

Gap insurance for electric cars is a complex and rapidly evolving market - and it's not always easy to navigate. But with the right information and the right insurance provider, you can find a policy that meets your needs and budget.

Until next time — Alex