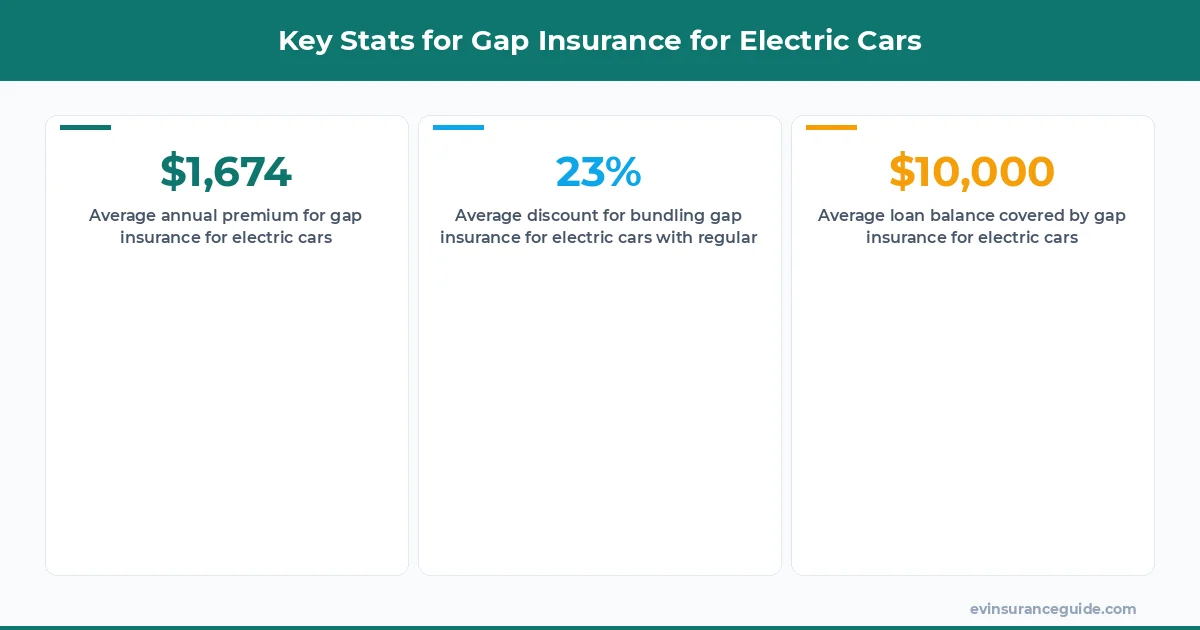

Filing an insurance claim for your electric vehicle (EV) can be a daunting task, but what if I told you that it's actually less complicated than trying to assemble IKEA furniture? Yeah, that's a thing. I mean, have you seen the instructions for a MALM dresser? It's like they want you to fail. But, I digress. Filing a claim for your EV, especially with gap insurance for electric cars, can be a relatively smooth process if you know what you're doing. Sound familiar? You buy a brand new Tesla Model 3, and a few months later, it's totaled in an accident. You're left with a loan balance of $40,000, but the insurance company only pays out $30,000. That's where gap insurance for electric cars comes in - to cover that $10,000 difference.

MYTH_BUST: Gap Insurance is a Scam

One common myth about gap insurance for electric cars is that it's a waste of money. But, let's be real, if you're financing a car like the BMW iX, which can cost upwards of $100,000, you're gonna want that extra protection. I mean, who can afford to pay out of pocket for a $20,000 loan balance? Not me, that's for sure. Gap insurance for electric cars can provide peace of mind, knowing that you're covered in case your car is totaled or stolen. Know what the kicker is? Some insurance companies, like Geico, offer gap insurance for electric cars as an add-on to your regular policy. It's usually around $20-$30 per year, which is a small price to pay for the protection it provides.

But, what about the process of filing a claim? It's not as painful as getting a root canal, I promise. Most insurance companies have a streamlined process for filing claims, and some even offer online portals or mobile apps to make it easier. For example, State Farm has a mobile app that allows you to file a claim and upload photos of the damage. It's quick, easy, and relatively painless. And, with gap insurance for electric cars, you can rest assured that you're covered, even if your car is totaled.

HONEST_OPINION: Don't Skimp on Gap Insurance for Electric Cars

Listen, I know what you're thinking - "Do I really need gap insurance for electric cars?" And my honest opinion is, yes, you do. I mean, think about it, if you're financing a car like the Hyundai Ioniq 5, which can cost around $40,000, you're gonna want that extra protection. Gap insurance for electric cars can provide peace of mind, knowing that you're covered in case your car is totaled or stolen. And, let's be real, accidents can happen to anyone, at any time. It's not just about the cost of the car, it's about the loan balance, and gap insurance for electric cars can help cover that.

For example, let's say you buy a Rivian R1T, which can cost upwards of $70,000. You put down $10,000 and finance the rest. A few months later, the car is totaled in an accident. The insurance company pays out $50,000, but you still owe $60,000 on the loan. That's where gap insurance for electric cars comes in - to cover that $10,000 difference. It's a small price to pay for the protection it provides. And, with some insurance companies, like Allstate, you can even customize your policy to fit your needs.

5 Key Steps to Filing a Claim

Filing a claim can seem like a daunting task, but it's actually relatively straightforward. Here are the 5 key steps to filing a claim:

- 1. Notify your insurance company as soon as possible. Most companies have a 24-hour hotline for reporting claims.

- 2. Provide detailed information about the accident, including photos and witness statements.

- 3. Get an estimate for the repairs from a reputable body shop.

- 4. Review and sign the claim settlement agreement.

- 5. Follow up with your insurance company to ensure the claim is being processed.

Pro tip: Keep a record of all correspondence with your insurance company, including dates, times, and details of conversations. This can help avoid any disputes down the line.

But, what about the cost of gap insurance for electric cars? It's usually around $20-$30 per year, which is a small price to pay for the protection it provides. And, with some insurance companies, like Progressive, you can even bundle gap insurance for electric cars with your regular policy for a discount.

WARNING: Don't Assume Your Regular Policy Covers Everything

One common mistake people make is assuming that their regular insurance policy covers everything. But, that's not always the case. Regular policies usually only cover the actual cash value of the car, which can leave you with a significant loan balance if your car is totaled. That's where gap insurance for electric cars comes in - to cover that difference. Know what the worst part is? If you don't have gap insurance for electric cars, you could be left with a loan balance of $10,000 or more. That's a lot of money to pay out of pocket.

For example, let's say you buy a Tesla Model Y, which can cost around $50,000. You put down $10,000 and finance the rest. A few months later, the car is totaled in an accident. The insurance company pays out $30,000, but you still owe $40,000 on the loan. That's where gap insurance for electric cars comes in - to cover that $10,000 difference.

COMPARISON: Gap Insurance for Electric Cars vs Regular Insurance

So, what's the difference between gap insurance for electric cars and regular insurance? Well, regular insurance usually only covers the actual cash value of the car, which can leave you with a significant loan balance if your car is totaled. Gap insurance for electric cars, on the other hand, covers the difference between the loan balance and the actual cash value of the car. It's like the difference between a iPhone and a Samsung - they both do the same thing, but one has more features. Gap insurance for electric cars is like the iPhone of insurance policies - it provides more protection and peace of mind.

And, with some insurance companies, like USAA, you can even get a discount on your regular policy if you bundle it with gap insurance for electric cars. It's a win-win situation. But, don't just take my word for it - do your research and compare policies from different insurance companies. You might be surprised at how much you can save.

FAQs

#### What is gap insurance for electric cars?

Gap insurance for electric cars is a type of insurance that covers the difference between the loan balance and the actual cash value of the car. It's usually around $20-$30 per year, which is a small price to pay for the protection it provides.

#### How do I file a claim?

Filing a claim is relatively straightforward. You'll need to notify your insurance company as soon as possible, provide detailed information about the accident, get an estimate for the repairs, review and sign the claim settlement agreement, and follow up with your insurance company to ensure the claim is being processed.

#### What is the average cost of gap insurance for electric cars?

The average cost of gap insurance for electric cars is around $20-$30 per year. However, this can vary depending on the insurance company and the type of policy you have.

#### Do I need gap insurance for electric cars if I have a regular policy?

Yes, you should consider getting gap insurance for electric cars, even if you have a regular policy. Regular policies usually only cover the actual cash value of the car, which can leave you with a significant loan balance if your car is totaled. Gap insurance for electric cars can provide peace of mind, knowing that you're covered in case your car is totaled or stolen.

#### Can I customize my policy to fit my needs?

Yes, with some insurance companies, like Allstate, you can customize your policy to fit your needs. This can include adding gap insurance for electric cars, roadside assistance, or other features.

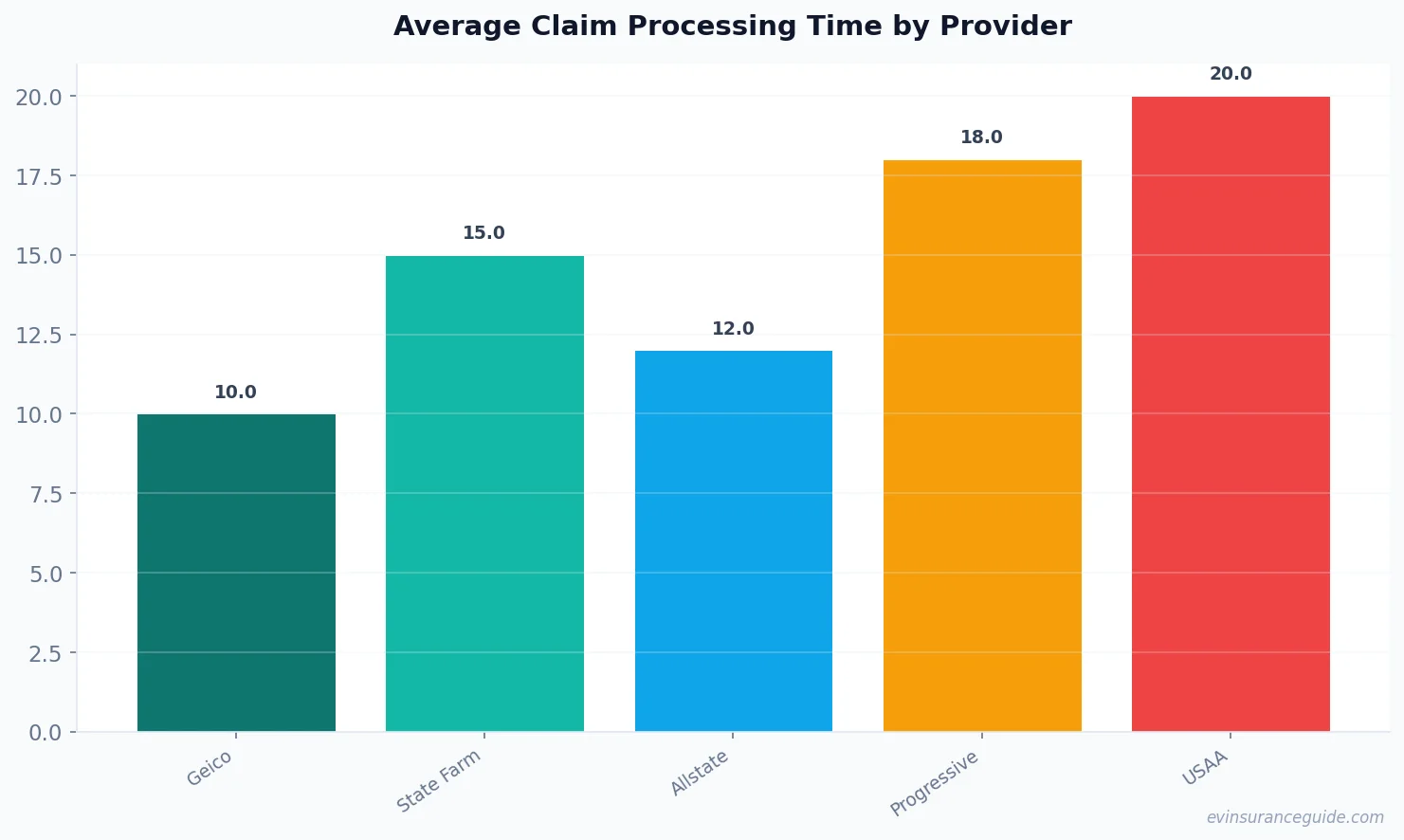

#### How long does it take to process a claim?

The time it takes to process a claim can vary depending on the insurance company and the complexity of the claim. However, most insurance companies have a streamlined process for filing claims, and some even offer online portals or mobile apps to make it easier.

And, finally, don't forget to shop around for insurance policies. You might be surprised at how much you can save by comparing policies from different insurance companies. For example, a study by the National Association of Insurance Commissioners found that drivers who shopped around for insurance policies saved an average of $400 per year.

Happy driving, and don't overpay! — Alex