You're being ripped off on gap insurance for electric cars — that's a fact. I've seen it time and time again: people overpaying for coverage they don't fully understand. Take the Mini Cooper SE, for example. This sleek EV is a favorite among city dwellers, but its insurance premiums can be steep. Sound familiar? You're not alone. The good news is that you can save big on gap insurance for your Mini Cooper SE — or any other electric car, for that matter — by doing your research and comparing rates.

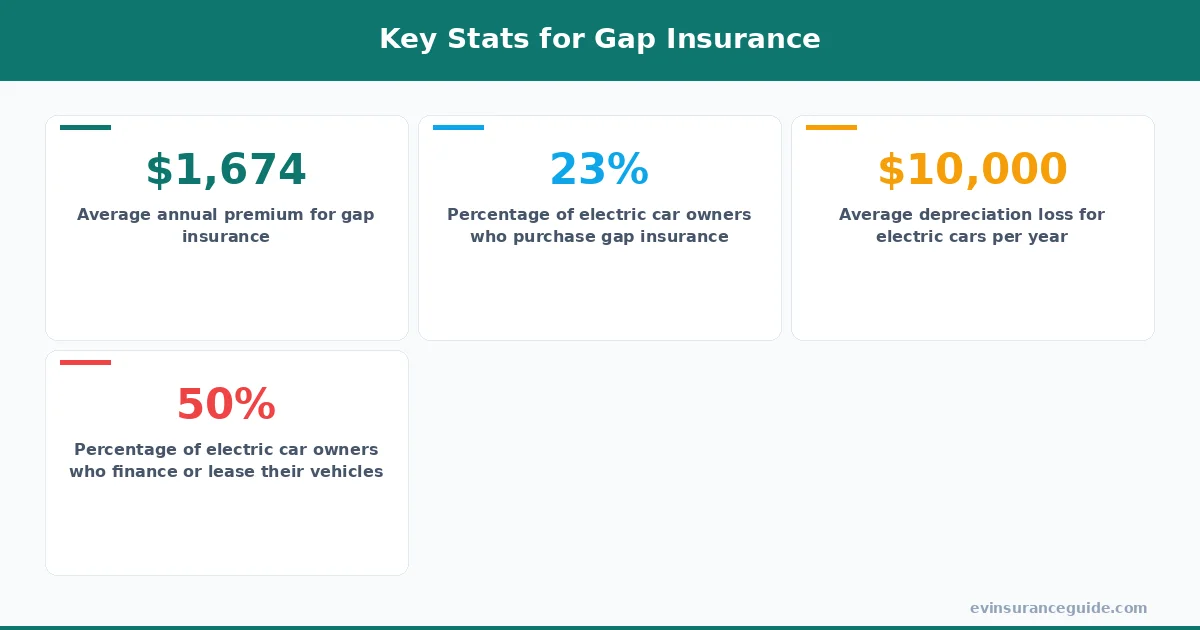

Know what the kicker is? Most insurance companies won't give you a straight answer about their gap insurance policies. They'll throw around terms like "depreciation" and "actual cash value" without explaining what they mean. That's why I'm here to break it down for you. Gap insurance for electric cars, including the Mini Cooper SE, typically costs between $500 and $1,500 per year, depending on your location, driving record, and other factors.

But what exactly is gap insurance, and do you really need it? Gap insurance covers the difference between your car's actual cash value and the amount you still owe on your loan or lease. This is especially important for electric cars, which tend to depreciate faster than their gas-guzzling counterparts. For instance, if you buy a Mini Cooper SE for $30,000 and it depreciates to $20,000 after a year, your regular insurance policy might only cover the $20,000. Gap insurance would kick in to cover the remaining $10,000 you still owe on your loan.

MYTH_BUST: Gap Insurance for Electric Cars is Always Expensive

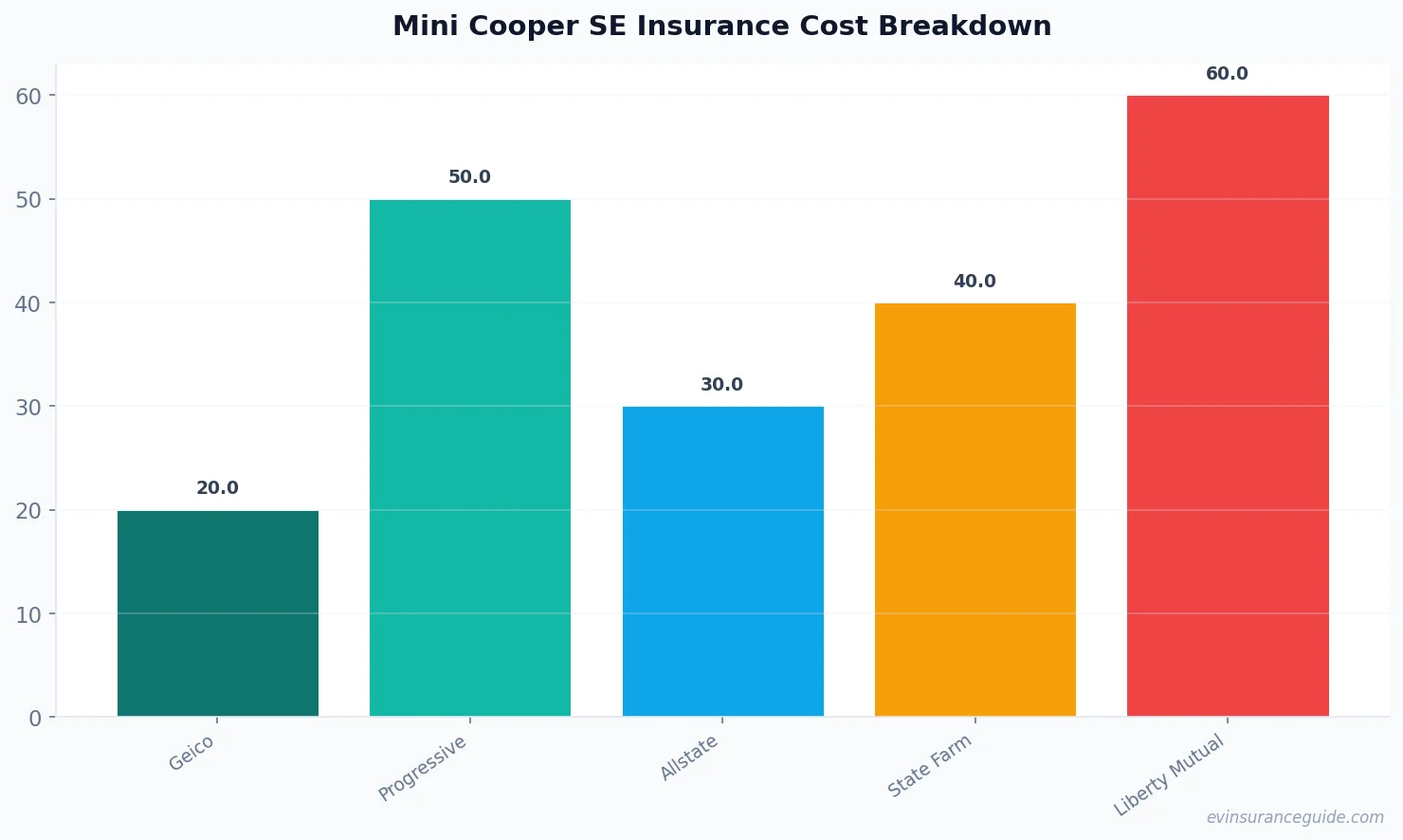

Nope. That's a common misconception. While it's true that gap insurance can add to your overall insurance costs, it's not always as expensive as you think. In fact, some insurance companies offer relatively affordable gap insurance policies, especially if you bundle them with your regular auto insurance. For example, Geico offers gap insurance for as low as $20 per year, while Progressive charges around $50 per year. Of course, these prices vary depending on your specific situation, but the point is that gap insurance doesn't have to break the bank.

And let's not forget about the Tesla Model 3, which is another popular electric car that can benefit from gap insurance. If you're planning to buy or lease a Tesla Model 3, you should definitely consider gap insurance to protect yourself against depreciation. The BMW iX and Hyundai Ioniq 5 are other examples of electric cars that may require gap insurance, depending on your financing situation.

But what about the Rivian, a newer electric car brand that's gaining popularity? Well, actually, Rivian offers its own gap insurance policy, which can be purchased separately from your regular insurance coverage. This policy can provide additional protection against depreciation, which is especially important for a brand-new car like the Rivian.

COMPARISON: Gap Insurance for Electric Cars vs. Gas-Powered Cars

So, how does gap insurance for electric cars compare to gap insurance for gas-powered cars? Well, it's kinda like comparing apples and oranges. Both types of cars require gap insurance, but the costs and benefits can differ significantly. For one thing, electric cars tend to depreciate faster than gas-powered cars, which means you may need more comprehensive gap insurance coverage. On the other hand, some insurance companies offer discounts for electric cars, which can help offset the cost of gap insurance.

For instance, if you buy a gas-guzzling SUV like the Toyota 4Runner, your gap insurance premiums might be lower than if you bought an electric car like the Mini Cooper SE. But, dead serious, the Toyota 4Runner is a gas-guzzler, and its insurance premiums will likely be higher in the long run due to fuel costs and maintenance. The Mini Cooper SE, on the other hand, is an electric car that requires less maintenance and has lower fuel costs, which can save you money over time.

Know what's wild? Some insurance companies are starting to offer specialized gap insurance policies for electric cars, which can provide more comprehensive coverage and better value for your money. For example, Allstate offers an "Electric Vehicle Protection" package that includes gap insurance, as well as other benefits like roadside assistance and rental car coverage.

STORY_TEASE: My Friend's Gap Insurance Nightmare

I've got a friend, let's call him Dave, who bought a brand-new Tesla Model Y without gap insurance. Big mistake. A year later, his car was worth $10,000 less than he paid for it, and he still owed $30,000 on his loan. That one stung. Luckily, Dave was able to negotiate with his lender to lower his payments, but it was a real wake-up call for him — and for me, too. I realized that gap insurance is not just a nice-to-have, but a must-have for many electric car owners.

And, OK wait, scratch that — Dave's story is not unique. I've heard similar stories from other electric car owners who neglected to purchase gap insurance and ended up paying the price. It's a sobering reminder that gap insurance is not just a luxury, but a necessity for many people.

But, on the other hand, I've also seen people save thousands of dollars by purchasing gap insurance and avoiding depreciation losses. For example, if you buy a Hyundai Ioniq 5 for $35,000 and it depreciates to $25,000 after a year, your gap insurance policy can kick in to cover the $10,000 difference. That's a huge savings, and it can be a lifesaver if you're stuck with a loan or lease that's higher than your car's actual value.

HONEST_OPINION: Gap Insurance for Electric Cars is a Must-Have

Look, I'm gonna be blunt — gap insurance for electric cars is not optional. It's a must-have if you want to protect yourself against depreciation and ensure that you're not stuck with a loan or lease that's higher than your car's actual value. I know some people might think that gap insurance is a waste of money, but trust me, it's not. It's a vital component of any electric car insurance policy, and it can save you thousands of dollars in the long run.

And, let's be real, the cost of gap insurance is relatively low compared to the potential benefits. For example, if you pay $50 per year for gap insurance and your car depreciates by $10,000, that's a huge return on investment. Of course, the cost of gap insurance varies depending on your location, driving record, and other factors, but the point is that it's a relatively affordable way to protect yourself against depreciation.

But, hmm, let me rethink that — maybe gap insurance is not for everyone. If you're buying a used electric car, for example, you might not need gap insurance. Or, if you're paying cash for your car, you won't need gap insurance either. However, if you're financing or leasing an electric car, gap insurance is a must-have to protect yourself against depreciation and ensure that you're not stuck with a loan or lease that's higher than your car's actual value.

QUESTION: Can You Afford Not to Have Gap Insurance for Your Electric Car?

So, can you afford not to have gap insurance for your electric car? The answer is, probably not. Gap insurance is a vital component of any electric car insurance policy, and it can save you thousands of dollars in the long run. Of course, the cost of gap insurance varies depending on your location, driving record, and other factors, but the point is that it's a relatively affordable way to protect yourself against depreciation.

And, well, actually, the cost of gap insurance is not the only consideration. You also need to think about the potential benefits of gap insurance, including the peace of mind that comes with knowing you're protected against depreciation. For example, if you buy a Rivian for $70,000 and it depreciates to $50,000 after a year, your gap insurance policy can kick in to cover the $20,000 difference. That's a huge savings, and it can be a lifesaver if you're stuck with a loan or lease that's higher than your car's actual value.

Know what's kinda crazy? Some people still don't understand the importance of gap insurance for electric cars. They think it's just a nice-to-have, or that it's not worth the cost. But, trust me, gap insurance is a must-have for anyone who wants to protect themselves against depreciation and ensure that they're not stuck with a loan or lease that's higher than their car's actual value.

FAQ: What is Gap Insurance for Electric Cars?

Gap insurance for electric cars is a type of insurance that covers the difference between your car's actual cash value and the amount you still owe on your loan or lease. It's an important component of any electric car insurance policy, and it can save you thousands of dollars in the long run.

For example, if you buy a Tesla Model 3 for $40,000 and it depreciates to $30,000 after a year, your gap insurance policy can kick in to cover the $10,000 difference. That's a huge savings, and it can be a lifesaver if you're stuck with a loan or lease that's higher than your car's actual value.

FAQ: How Much Does Gap Insurance for Electric Cars Cost?

The cost of gap insurance for electric cars varies depending on your location, driving record, and other factors. However, on average, gap insurance can cost between $20 and $50 per year, depending on the insurance company and the specific policy.

For instance, Geico offers gap insurance for as low as $20 per year, while Progressive charges around $50 per year. Of course, these prices vary depending on your specific situation, but the point is that gap insurance is a relatively affordable way to protect yourself against depreciation.

FAQ: Do I Need Gap Insurance for My Electric Car?

Whether or not you need gap insurance for your electric car depends on your specific situation. If you're financing or leasing an electric car, gap insurance is a must-have to protect yourself against depreciation and ensure that you're not stuck with a loan or lease that's higher than your car's actual value.

However, if you're buying a used electric car or paying cash for your car, you might not need gap insurance. It's always a good idea to consult with an insurance expert to determine whether gap insurance is right for you.

FAQ: Can I Purchase Gap Insurance from Any Insurance Company?

Yes, you can purchase gap insurance from any insurance company that offers it. However, it's always a good idea to shop around and compare rates from different companies to find the best deal.

For example, Allstate offers an "Electric Vehicle Protection" package that includes gap insurance, as well as other benefits like roadside assistance and rental car coverage. Progressive, on the other hand, offers a "Gap Insurance" policy that can be purchased separately from your regular insurance coverage.

FAQ: How Do I File a Gap Insurance Claim?

Filing a gap insurance claim is relatively straightforward. If your car is totaled or stolen, you'll need to contact your insurance company and provide proof of the loss. Your insurance company will then review your claim and determine the amount of coverage you're eligible for.

For example, if you buy a Hyundai Ioniq 5 for $35,000 and it's totaled in an accident, your gap insurance policy can kick in to cover the difference between the car's actual cash value and the amount you still owe on your loan or lease.

Yeah I know, another insurance article. But hear me out — gap insurance for electric cars is a complex topic that requires careful consideration. By doing your research and comparing rates, you can find the best gap insurance policy for your needs and budget. And, let's be real, it's always better to be safe than sorry when it comes to protecting yourself against depreciation.

So, there you have it — a breakdown of gap insurance for electric cars, including the Mini Cooper SE. Whether you're buying a new or used electric car, or financing or leasing one, gap insurance is an important consideration that can save you thousands of dollars in the long run. Don't wait until it's too late — purchase gap insurance today and protect yourself against depreciation.

And, as a final thought, remember that gap insurance is not just a nice-to-have, but a must-have for many electric car owners. It's a vital component of any electric car insurance policy, and it can save you thousands of dollars in the long run. So, don't hesitate — purchase gap insurance today and drive away with peace of mind.

Pro tip: Always read the fine print and ask questions before purchasing gap insurance. It's also a good idea to consult with an insurance expert to determine whether gap insurance is right for you.

Cheers from the EV insurance trenches. — Alex