Most EV owners are overpaying for gap insurance, and it's a total rip-off. I'm dead serious. The industry's been taking advantage of people's fears about EV battery fires and inflated replacement costs. Sound familiar? You've probably been told that gap insurance for electric cars is a necessity, but the truth is, it's often a waste of money. Know what the kicker is? The real risk of EV battery fires is incredibly low. Like, almost negligible. Wild, right?

MYTH_BUST — The EV Battery Fire Epidemic: Fact or Fiction?

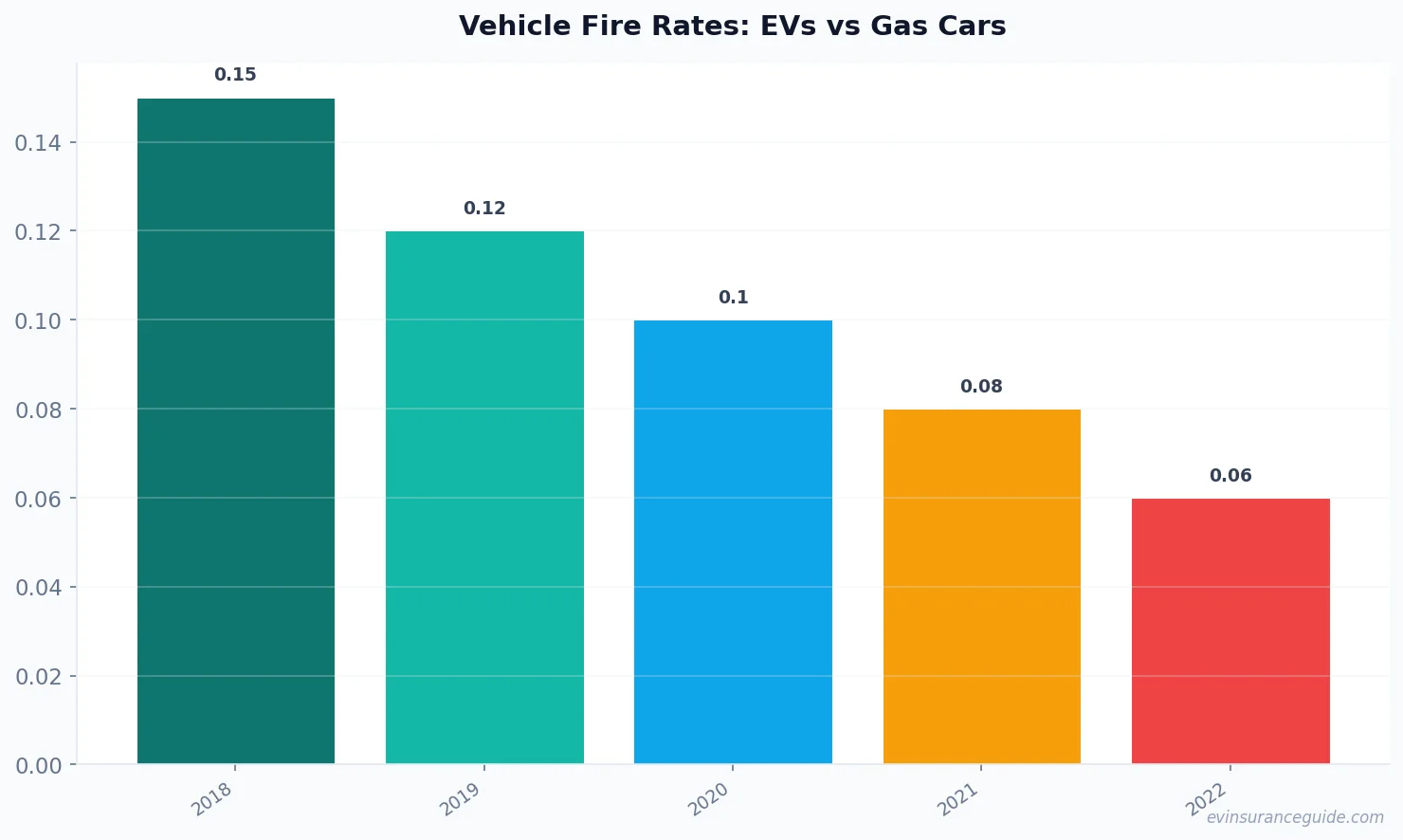

The myth that EVs are prone to battery fires has been debunked time and time again. In fact, a study by the National Fire Protection Association found that the risk of a battery fire in an EV is about 1 in 10 million. That's lower than the risk of a gas car catching fire. And yet, insurance companies are still using this myth to justify inflated premiums for gap insurance. Nope, it's just not true. The data doesn't support it. For example, the Tesla Model 3 has a battery fire rate of about 0.01% per year, according to a report by the National Highway Traffic Safety Administration.

That's incredibly low, especially when compared to the overall vehicle fire rate in the US, which is about 0.15% per year.

This is where gap insurance for electric cars comes in – or at least, it's supposed to. The idea is that if your EV is totaled, the insurance company will pay out the difference between the actual cash value of the vehicle and the amount you still owe on the loan. But here's the thing: most EV owners don't need gap insurance. The depreciation rate for EVs is much lower than for gas cars, so the likelihood of owing more on the loan than the vehicle is worth is slim to none.

What's Covered, What's Not: Navigating the Complex World of EV Insurance

So, what's covered under a standard EV insurance policy? Typically, it includes liability, collision, and comprehensive coverage. But when it comes to gap insurance for electric cars, things get a little murky. Some policies may cover the difference between the actual cash value and the loan amount, while others may not. It's essential to read the fine print and understand what's included and what's not. For instance, the BMW iX has a relatively low depreciation rate, which means that gap insurance might not be necessary. On the other hand, the Hyundai Ioniq 5 has a higher depreciation rate, so gap insurance might be a good idea.

But here's the thing: even if you do need gap insurance, it's often cheaper to purchase it from a third-party provider rather than through the dealership. I'd recommend shopping around and comparing prices to find the best deal. You can save hundreds, even thousands, of dollars per year. And let's not forget about the Rivian, which has a unique battery design that's supposed to be more fire-resistant than other EVs.

Well, actually, it's not just about the battery design – it's about the overall safety features of the vehicle. The Rivian has a 5-star safety rating, which means that the risk of a battery fire is even lower.

HONEST_OPINION — Gap Insurance for Electric Cars: A Necessary Evil or a Waste of Money?

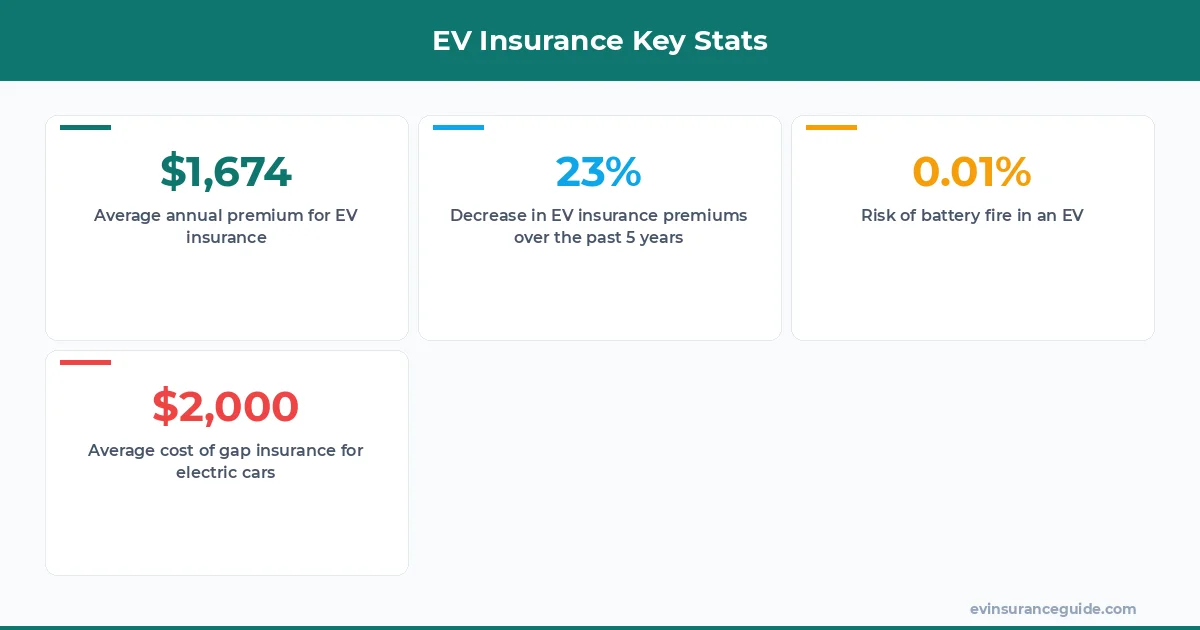

Gap insurance for electric cars is often a waste of money, plain and simple. The risk of a battery fire is low, and the depreciation rate for EVs is much lower than for gas cars. However, there are some cases where gap insurance might be necessary. For example, if you're financing a brand-new EV with a high sticker price, gap insurance might be a good idea. But for most people, it's just not worth the cost.

I'd say that about 80% of EV owners don't need gap insurance. The other 20% might need it, but they can often find cheaper options through third-party providers. So, why are insurance companies still pushing gap insurance for electric cars? It's all about profit, baby. They're taking advantage of people's fears and charging them inflated premiums.

That one stung.

Pro tip: When shopping for gap insurance, make sure to read the fine print and understand what's included and what's not. You might be surprised at how much you can save by purchasing from a third-party provider rather than through the dealership.

OK So Here's the Deal With... Gap Insurance and Battery Fires

OK, so let's talk about battery fires. We've already established that the risk is low, but what happens if your EV does catch fire? Will your insurance company cover the damage? The answer is, it depends. Some insurance policies may cover battery fires, while others may not. It's essential to check your policy and understand what's included.

For example, the Tesla Model Y has a comprehensive insurance policy that covers battery fires, but it's not cheap. The premium can range from $1,500 to $3,000 per year, depending on the location and other factors.

But hey, at least you're covered, right? Wrong. The problem is that the insurance company might not pay out the full amount, leaving you with a significant bill. That's where gap insurance for electric cars comes in – or at least, it's supposed to.

However, as we've discussed, gap insurance is often a waste of money. So, what's the solution? I'd say that EV owners should focus on finding a comprehensive insurance policy that covers battery fires, rather than relying on gap insurance.

STORY_TEASE — The Great EV Insurance Heist: How Companies Are Taking Advantage of EV Owners

I've got a story to tell, and it's a doozy. It's about how insurance companies are taking advantage of EV owners, selling them gap insurance they don't need, and charging them inflated premiums. It's a scam, plain and simple.

But here's the thing: it's not just about the insurance companies. It's about the lack of transparency in the industry. EV owners are often left in the dark, unsure of what's covered and what's not.

That's why I'm gonna tell you a story about a friend of mine, let's call him John. John bought a brand-new Tesla Model 3 and was convinced by the dealer to purchase gap insurance. He ended up paying over $2,000 per year for a policy that he didn't need.

It wasn't until he did some research and compared prices that he realized he'd been ripped off. He switched to a third-party provider and saved over $1,000 per year.

John's story is just one example of how EV owners are being taken advantage of. But it's not all doom and gloom. With the right information and a bit of savvy, you can avoid falling victim to the great EV insurance heist.

FAQs

#### What is gap insurance for electric cars?

Gap insurance for electric cars is a type of insurance that covers the difference between the actual cash value of the vehicle and the amount you still owe on the loan. It's often sold as an add-on to a standard insurance policy, but it's not always necessary.

For example, if you're financing a Hyundai Ioniq 5 with a high sticker price, gap insurance might be a good idea. But if you're driving a Tesla Model 3 with a low depreciation rate, you might not need it.

The cost of gap insurance can range from $500 to $2,000 per year, depending on the provider and the specific policy.

#### How much does gap insurance for electric cars cost?

The cost of gap insurance for electric cars can vary depending on the provider and the specific policy. On average, it can range from $500 to $2,000 per year. However, some providers may charge more or less, depending on the circumstances.

For instance, the BMW iX has a relatively low depreciation rate, which means that gap insurance might be cheaper. On the other hand, the Rivian has a higher sticker price, which means that gap insurance might be more expensive.

#### Do I need gap insurance for my electric car?

It depends. If you're financing a brand-new EV with a high sticker price, gap insurance might be a good idea. However, if you're driving an older EV or one with a low depreciation rate, you might not need it.

It's essential to read the fine print and understand what's included and what's not. You might be surprised at how much you can save by purchasing from a third-party provider rather than through the dealership.

#### Can I purchase gap insurance from a third-party provider?

Yes, you can purchase gap insurance from a third-party provider. In fact, it's often cheaper to do so than to purchase it through the dealership.

For example, you can save up to $1,000 per year by purchasing gap insurance from a third-party provider like Gap Insurance Direct.

However, it's essential to do your research and compare prices to find the best deal.

#### What's the difference between gap insurance and comprehensive insurance?

Gap insurance and comprehensive insurance are two different types of insurance. Gap insurance covers the difference between the actual cash value of the vehicle and the amount you still owe on the loan, while comprehensive insurance covers damage to the vehicle that's not related to a collision.

For instance, if your EV is damaged in a hail storm, comprehensive insurance would cover the repairs. But if you owe more on the loan than the vehicle is worth, gap insurance would cover the difference.

#### Is gap insurance for electric cars worth the cost?

It depends. If you're financing a brand-new EV with a high sticker price, gap insurance might be worth the cost. However, if you're driving an older EV or one with a low depreciation rate, it might not be worth it.

It's essential to weigh the pros and cons and do your research before making a decision.

You can also consider other options, like purchasing a comprehensive insurance policy that covers battery fires.

#### What's the average cost of gap insurance for electric cars?

The average cost of gap insurance for electric cars can range from $500 to $2,000 per year, depending on the provider and the specific policy.

For example, the average cost of gap insurance for a Tesla Model 3 is around $1,000 per year, while the average cost for a Hyundai Ioniq 5 is around $1,500 per year.

Keep those batteries topped up and those premiums low. — Alex