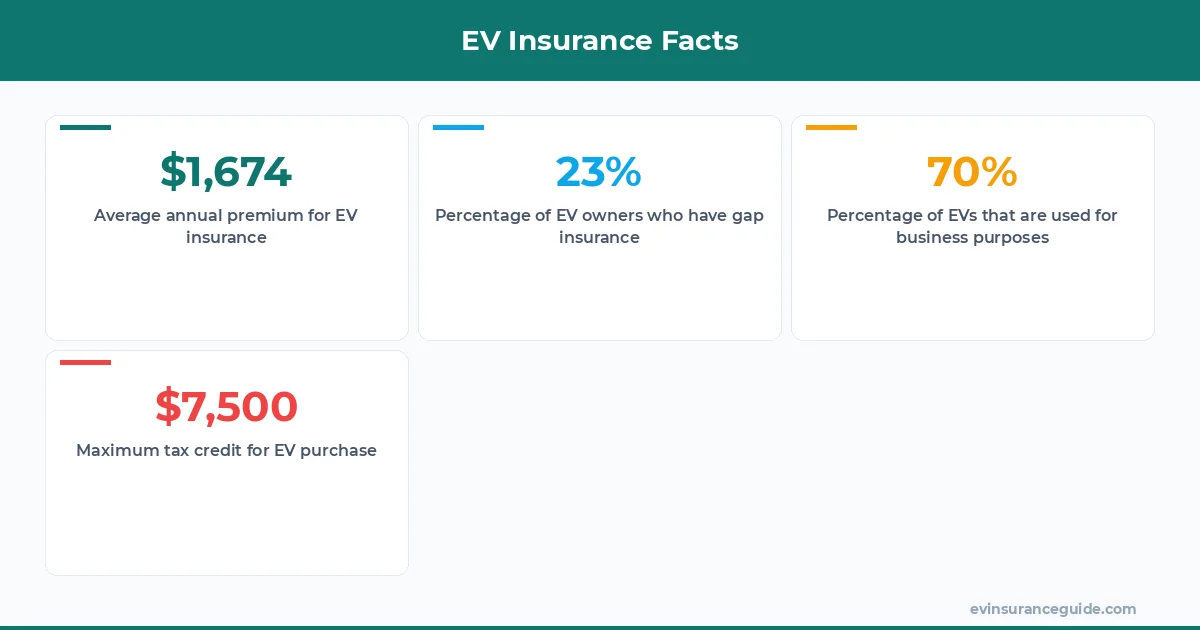

Meet Emily, a freelancer who's been driving a Tesla Model 3 for her business. Before switching to an EV, she was paying around $1,200 per year for insurance, and none of it was tax-deductible. But after making the switch, she was able to deduct around $800 of her insurance costs as a business expense. That's a significant savings, especially considering she's also eligible for a tax credit of up to $7,500 for her EV purchase. Sound familiar?

Comparing Gap Insurance for Electric Cars to Traditional Vehicles

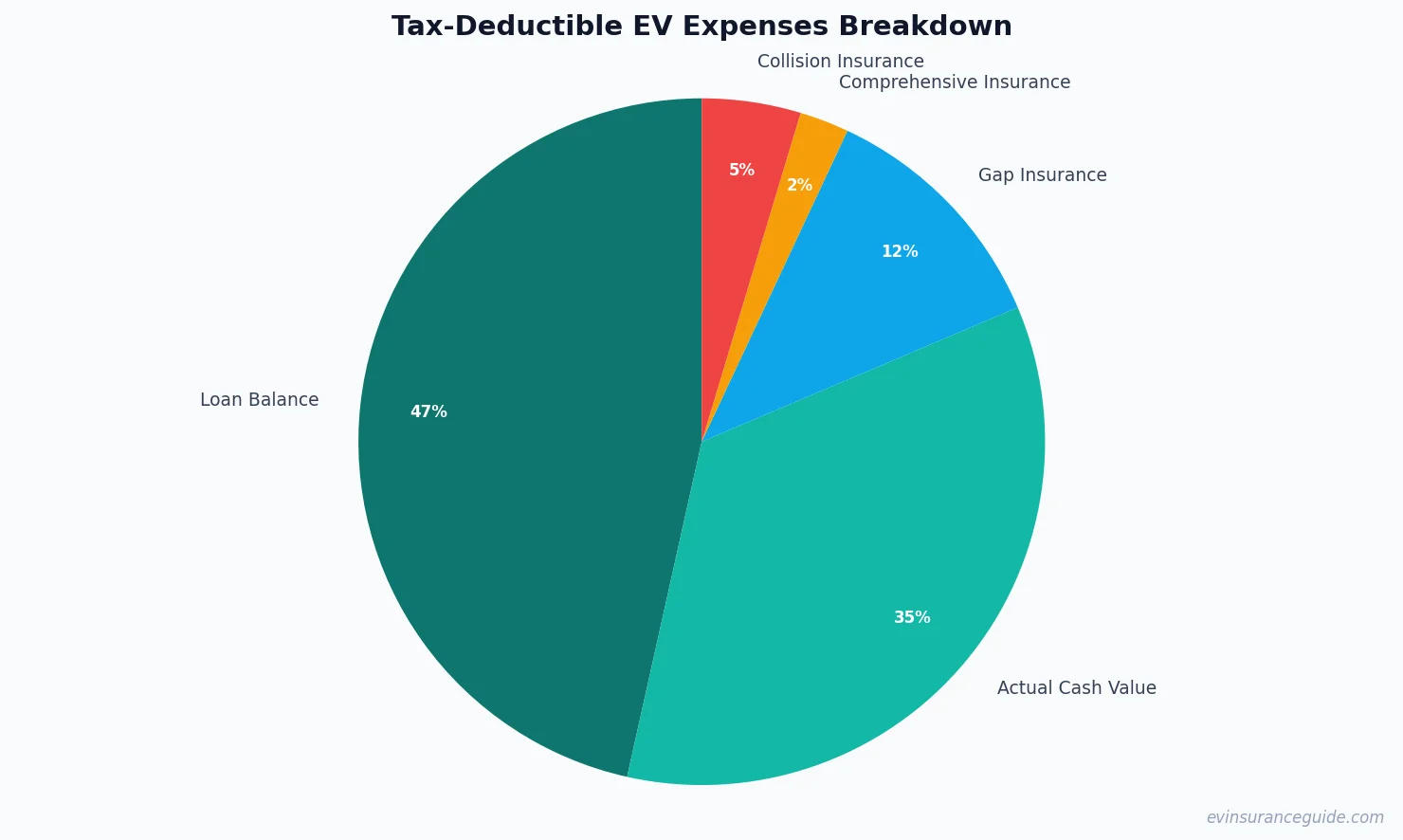

Gap insurance for electric cars is a type of insurance that covers the difference between the actual cash value of the vehicle and the remaining loan balance in the event of a total loss. But how does it compare to traditional vehicles? Well, for one, EVs tend to hold their value better than gas-powered cars, which means the gap between the actual cash value and the loan balance is typically smaller. For example, a Tesla Model Y might retain around 70% of its value after three years, while a comparable gas-powered SUV might retain only around 50%. Know what the kicker is? Gap insurance for electric cars can be more expensive than traditional gap insurance, with premiums ranging from $20 to $50 per month.

But here's the thing: gap insurance for electric cars can be a smart investment, especially for business owners who use their EVs for work. Not only can it provide peace of mind in the event of a total loss, but it can also help to reduce the financial burden of replacing the vehicle. And, as we mentioned earlier, it may be tax-deductible as a business expense. Dead serious, it's worth exploring.

For instance, let's say you're a business owner who uses a Rivian R1T for work. You've got a loan balance of $60,000, and the actual cash value of the vehicle is $50,000. If you're in an accident and the vehicle is totaled, you'd be on the hook for the $10,000 difference. But with gap insurance, you'd be covered for that amount, which could be a huge relief. And, if you're using the vehicle for business, you may be able to deduct the cost of the gap insurance as a business expense.

Can You Deduct Gap Insurance for Electric Cars as a Business Expense?

So, can you deduct gap insurance for electric cars as a business expense? The answer is, it depends. If you're using your EV for business purposes, you may be able to deduct a portion of your insurance costs, including gap insurance. But, you'll need to keep detailed records of your business use, including mileage logs and receipts for insurance premiums. And, you'll need to file Form 2106 with the IRS to claim the deduction.

For example, let's say you're a freelancer who uses a Hyundai Ioniq 5 for work. You've got a gap insurance policy that costs $30 per month, and you use the vehicle for business 80% of the time. You could potentially deduct $24 per month (80% of $30) as a business expense. That's $288 per year, which may not seem like a lot, but it can add up. And, if you're also eligible for a tax credit for your EV purchase, you could be looking at some significant savings.

Pro tip: Keep detailed records of your business use, including mileage logs and receipts for insurance premiums. This will help you to accurately calculate your deduction and avoid any potential audits.

Myth-Busting: Gap Insurance for Electric Cars is Only for High-End Vehicles

There's a common myth that gap insurance for electric cars is only for high-end vehicles, like the Tesla Model S or the BMW iX. But, that's just not true. Gap insurance can be beneficial for any EV owner, regardless of the vehicle's price point. For instance, a Honda Clarity Electric owner may still benefit from gap insurance, especially if they've got a loan balance that's higher than the actual cash value of the vehicle.

And, it's not just about the vehicle's price point. It's about the potential financial burden of replacing the vehicle in the event of a total loss. For example, let's say you're a business owner who uses a Nissan Leaf for work. You've got a loan balance of $20,000, and the actual cash value of the vehicle is $15,000. If you're in an accident and the vehicle is totaled, you'd be on the hook for the $5,000 difference. But with gap insurance, you'd be covered for that amount, which could be a huge relief.

Warning: Don't Assume All Gap Insurance Policies are Created Equal

When it comes to gap insurance for electric cars, don't assume that all policies are created equal. Some policies may have exclusions or limitations that could leave you with a significant financial burden in the event of a total loss. For example, some policies may not cover certain types of damage, like flood or fire damage. Others may have a deductible or a maximum payout limit.

For instance, let's say you've got a gap insurance policy that covers up to $10,000 in damages, but you've got a loan balance of $20,000. If you're in an accident and the vehicle is totaled, you'd still be on the hook for the $10,000 difference. That's why it's so important to carefully review your policy and understand what's covered and what's not.

OK So Here's the Deal With Gap Insurance for Electric Cars and Tax Credits

So, what's the deal with gap insurance for electric cars and tax credits? Well, it's complicated. But, essentially, if you're eligible for a tax credit for your EV purchase, you may be able to deduct the cost of gap insurance as a business expense. But, you'll need to keep detailed records of your business use and file the appropriate paperwork with the IRS.

For example, let's say you're a business owner who uses a Tesla Model 3 for work, and you're eligible for a tax credit of up to $7,500. You've also got a gap insurance policy that costs $30 per month. You could potentially deduct the cost of the gap insurance as a business expense, which could help to reduce your tax liability. And, if you're using the vehicle for business, you may be able to depreciate the vehicle over time, which could provide additional tax savings.

Frequently Asked Questions

What is gap insurance for electric cars?

Gap insurance for electric cars is a type of insurance that covers the difference between the actual cash value of the vehicle and the remaining loan balance in the event of a total loss. It's a smart investment for business owners who use their EVs for work, as it can help to reduce the financial burden of replacing the vehicle.

How much does gap insurance for electric cars cost?

The cost of gap insurance for electric cars varies depending on the provider and the vehicle. But, on average, you can expect to pay between $20 to $50 per month. For example, a policy from Geico might cost $25 per month, while a policy from Progressive might cost $35 per month.

Can I deduct gap insurance for electric cars as a business expense?

If you're using your EV for business purposes, you may be able to deduct a portion of your insurance costs, including gap insurance. But, you'll need to keep detailed records of your business use and file the appropriate paperwork with the IRS. For instance, if you're a freelancer who uses a Hyundai Ioniq 5 for work, you could potentially deduct $24 per month (80% of $30) as a business expense.

What's the difference between gap insurance and comprehensive insurance?

Gap insurance and comprehensive insurance are two different types of insurance that serve different purposes. Comprehensive insurance covers damages to the vehicle that are not related to a collision, such as theft or vandalism. Gap insurance, on the other hand, covers the difference between the actual cash value of the vehicle and the remaining loan balance in the event of a total loss.

Do all EV owners need gap insurance?

Not all EV owners need gap insurance. But, if you've got a loan balance that's higher than the actual cash value of the vehicle, it may be a smart investment. For example, if you've got a loan balance of $40,000 and the actual cash value of the vehicle is $30,000, you may want to consider gap insurance to cover the $10,000 difference.

How do I choose the right gap insurance policy for my EV?

When choosing a gap insurance policy for your EV, you'll want to consider a few factors, including the cost of the policy, the coverage limits, and the deductible. You'll also want to read the fine print and understand what's covered and what's not. For instance, some policies may have exclusions or limitations that could leave you with a significant financial burden in the event of a total loss.

And, that one stung... but we've got this. Gap insurance for electric cars can be a complex topic, but with the right information, you can make an informed decision. Wild, right?

Cheers from the EV insurance trenches. — Alex