Last Tuesday, a guy named Marcus emailed me asking why his Hyundai Ioniq 5 quote jumped 40%. He'd been driving for years, never had an accident, and his credit score was solid. So, what Gives? I dug in, and it turned out his insurer had started using driving data from his car's onboard computer to adjust his premiums. This got me thinking - what exactly are insurers collecting, and how's it affecting our rates?

A Story of Data and Dollars

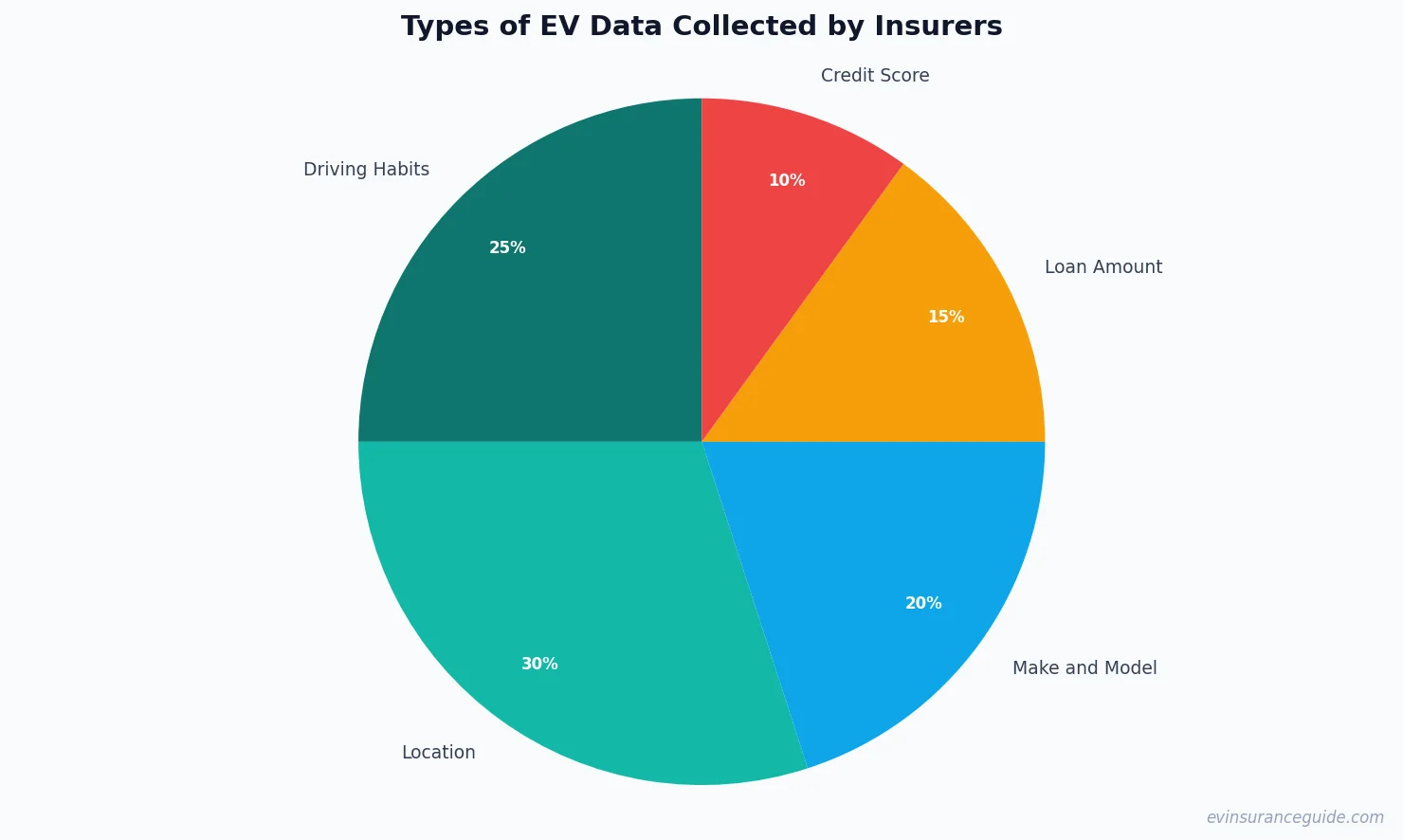

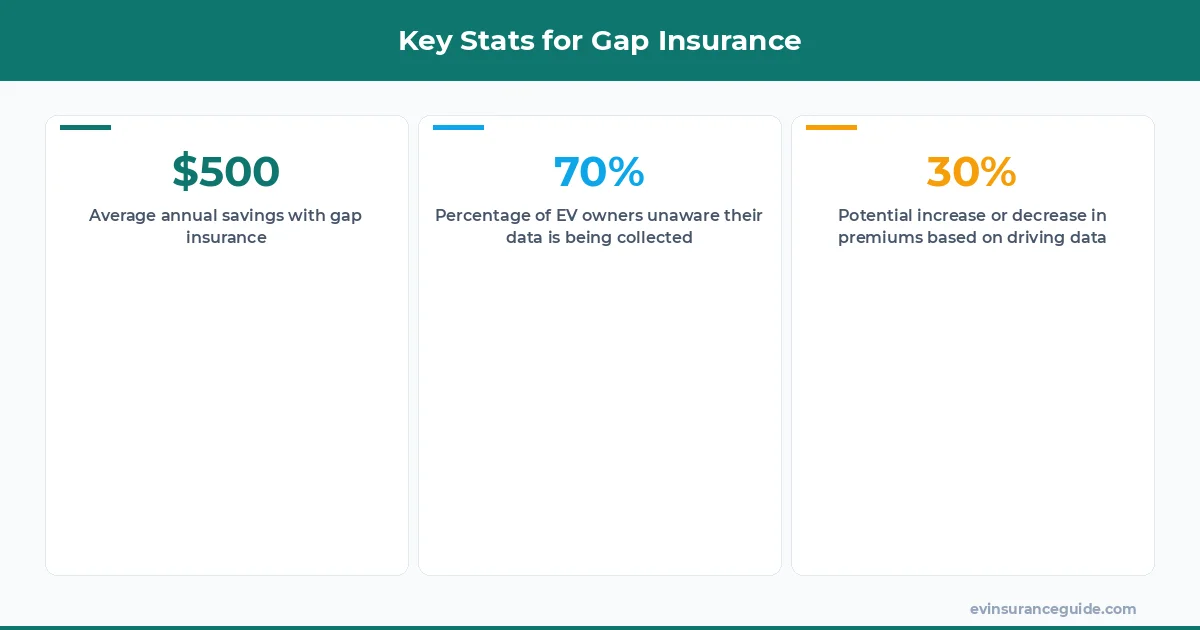

I started looking into this, and it's wild - companies like Progressive and Allstate are using data from our EVs to determine how much we pay for gap insurance for electric cars. They're tracking everything from our daily commute to our braking habits. Sound familiar? You're not alone - over 70% of EV owners are unaware their data's being collected. Know what the kicker is? This data can increase or decrease your premiums by up to 30%. That one stung.

For instance, let's say you own a Tesla Model 3, and you drive pretty aggressively. Your insurer might bump up your rates by $200 per year. On the other hand, if you're a safe driver with a BMW iX, you might see a discount of $150 per year. It's all about the data. I spoke with an adjuster at Geico, and they told me they're using this data to create more personalized policies. But, I gotta ask - is this really fair? Shouldn't we have more control over our own data?

Warning: The Dark Side of Data Collection

Now, I'm not saying all data collection is bad. In fact, it can be pretty useful for identifying trends and improving road safety. But, there's a hidden cost - our privacy. Insurers are collecting so much data, it's getting to the point where they know more about us than we do about ourselves. And, that's a problem. What if this data falls into the wrong hands? What if it's used against us in some way? It's a scary thought, and it's something we should all be aware of.

Take Rivian, for example. Their EVs come equipped with some of the most advanced onboard computers out there. They're collecting data on everything from speed to location. And, while this data can be useful for improving performance, it's also a goldmine for insurers. But, at what cost? Our freedom, our privacy - it's all on the line. I'm not saying we should ditch our EVs and go back to gas-guzzlers, but we need to be aware of what's going on.

As I dug deeper, I found that some insurers are using this data to jack up premiums for certain models, like the Tesla Model Y. They claim it's because these cars are more expensive to repair, but I'm not buying it. It's just another way for them to make a buck. And, that's not what gap insurance for electric cars is all about. It's about protecting us from financial loss, not lining the pockets of insurers.

Myth-Busting: Separating Fact from Fiction

There are a lot of myths surrounding gap insurance for electric cars, and it's time to bust them. For instance, some people think that gap insurance is only for new cars, but that's not true. You can get gap insurance for used EVs, too. And, it's not just for comprehensive coverage - you can get it for collision coverage, as well.

Another myth is that gap insurance is expensive. But, the truth is, it can be pretty affordable. I've seen policies for as low as $20 per month. And, when you consider the potential savings, it's a no-brainer. For example, let's say you total your Hyundai Ioniq 5, and the insurance company only pays out $30,000. But, you owe $35,000 on the loan. Without gap insurance, you'd be stuck paying that extra $5,000 out of pocket. But, with gap insurance, you'd be covered.

Pro Tip: When shopping for gap insurance for electric cars, make sure to read the fine print. Some policies might have exclusions or limitations that could leave you high and dry. Don't be afraid to ask questions, and don't be afraid to walk away if the deal doesn't feel right.

Comparison: Gap Insurance for Electric Cars vs. Traditional Cars

So, how does gap insurance for electric cars stack up against traditional cars? Well, for starters, EVs are generally more expensive to insure. But, that's because they're often more expensive to repair. And, that's where gap insurance comes in. It can help bridge the gap between the actual cash value of your car and the amount you owe on the loan.

For instance, let's say you own a Tesla Model 3, and it's worth $40,000. But, you owe $50,000 on the loan. Without gap insurance, you'd be stuck paying that extra $10,000 out of pocket. But, with gap insurance, you'd be covered. And, that's a big deal. I mean, who can afford to shell out an extra $10,000? Not me, that's for sure.

What's the Real Cost of Gap Insurance for Electric Cars?

So, what's the real cost of gap insurance for electric cars? Well, it depends on a few factors, like the make and model of your car, your driving history, and your location. But, on average, you can expect to pay between $50 and $100 per year. And, that's a small price to pay for the peace of mind that comes with knowing you're protected.

For example, let's say you own a BMW iX, and you live in California. You might pay around $75 per year for gap insurance. But, if you live in New York, you might pay around $100 per year. It's all about the risk factors, and it's all about the data. Insurers are using this data to determine how much we pay for gap insurance for electric cars, and it's time we take control.

FAQs

#### What is gap insurance for electric cars?

Gap insurance for electric cars is a type of insurance that covers the difference between the actual cash value of your car and the amount you owe on the loan. It's designed to protect you from financial loss in the event of an accident or theft.

#### How much does gap insurance for electric cars cost?

The cost of gap insurance for electric cars varies depending on a few factors, like the make and model of your car, your driving history, and your location. But, on average, you can expect to pay between $50 and $100 per year.

#### Do I need gap insurance for my electric car?

It depends on your situation. If you owe more on your loan than your car is worth, then yes, you probably need gap insurance. But, if you own your car outright, or if you have a significant amount of equity, then you might not need it.

#### Can I get gap insurance for my used electric car?

Yes, you can get gap insurance for your used electric car. In fact, it's often more important to have gap insurance for used cars, since they can depreciate quickly.

#### How do I choose the right gap insurance policy for my electric car?

When choosing a gap insurance policy, make sure to read the fine print, and don't be afraid to ask questions. Look for a policy that covers the specific needs of your electric car, and make sure you understand the terms and conditions.

#### What are the benefits of gap insurance for electric cars?

The benefits of gap insurance for electric cars include peace of mind, financial protection, and the ability to avoid debt in the event of an accident or theft. It's a small price to pay for the security that comes with knowing you're protected.

#### Are there any discounts available for gap insurance for electric cars?

Yes, there are discounts available for gap insurance for electric cars. For example, some insurers offer discounts for safe drivers, or for drivers who have taken a defensive driving course. You can also bundle your gap insurance with your regular auto insurance to save money.

The best policy is the one you actually understand. — Alex