I'm sipping coffee at a charging station, eavesdropping on a conversation between two EV owners. They're discussing their insurance rates, and one of them mentions how his Geico EV insurance premium dropped by $200 after improving his credit score. Sound familiar? We've all heard stories like this, but what's the real deal? Can a good credit score really save you that much on EV insurance?

WARNING — Hidden Credit Score Fees

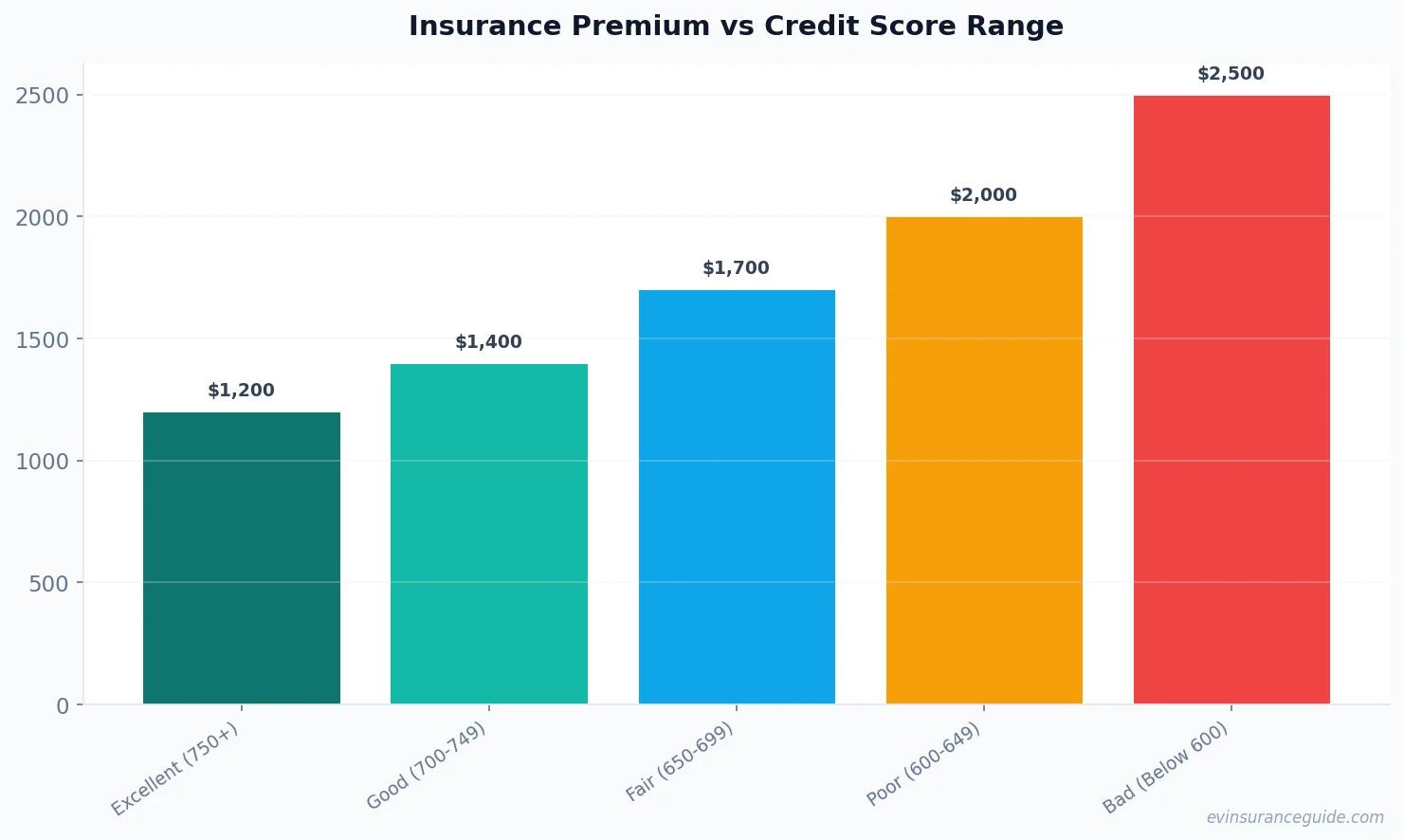

You think you're getting a good deal on your Geico EV insurance, but are you? What about the hidden fees and rate hikes based on your credit score? It's a trap many drivers fall into. For instance, if you've got a poor credit score, your Geico EV insurance premium could be as high as $2,500 per year, compared to $1,200 for someone with an excellent credit score. That's a whopping $1,300 difference. Know what the kicker is? Most insurance companies, including Geico, don't clearly disclose how they use credit scores to determine premiums. You'll be lucky to find a transparent explanation on their website.

Geico EV insurance rates are influenced by a range of factors, including your driving history, location, and vehicle type. But, your credit score plays a significant role in determining your premium. If you own a Tesla Model 3, for example, your insurance rate will likely be higher than for a Hyundai Ioniq 5. And, if you've got a poor credit score, you can expect to pay even more. According to data, drivers with poor credit scores pay an average of 30% more for EV insurance than those with good credit scores.

A friend of mine, let's call him Ryan, recently purchased a Rivian R1T. He was shocked when he received his Geico EV insurance quote, which was $500 higher than expected. It turned out that his credit score had taken a hit due to some unexpected medical bills. He ended up shopping around and found a better deal with another insurer, but not before learning a valuable lesson about the importance of credit scores in EV insurance.

STORY_TEASE — The Credit Score Conundrum

Imagine you're in the market for a new EV, and you've got your heart set on a BMW iX. You've done your research, and you think you've found a great deal on Geico EV insurance. But, what if your credit score is not as good as you thought? Will you still be able to afford the premium? This is the situation many drivers face, and it's not just about the money. A poor credit score can also limit your insurance options and increase your rates. For instance, if you've got a credit score below 600, you may be considered a high-risk driver, and your Geico EV insurance premium could skyrocket.

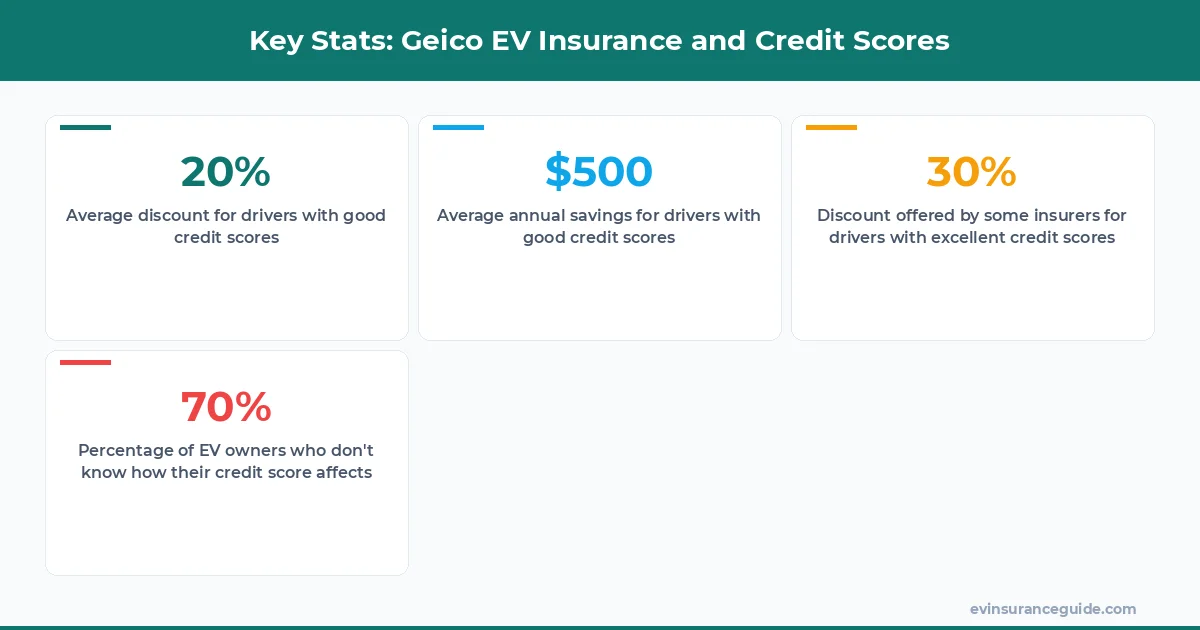

Ryan's story is not unique. Many drivers are unaware of the impact their credit score has on their EV insurance rates. In fact, a recent survey found that 70% of EV owners don't know how their credit score affects their insurance premium. This lack of knowledge can lead to some nasty surprises when it comes time to renew your policy. So, what can you do to avoid this? Start by checking your credit report regularly and disputing any errors you find. You can also work on improving your credit score by paying your bills on time and reducing your debt.

One of the most frustrating things about credit scores and EV insurance is the lack of transparency. Insurers like Geico often use complex algorithms to determine premiums, making it difficult for drivers to understand how their credit score is being used. This is why it's essential to shop around and compare rates from different insurers. You might be surprised at how much you can save by switching to a different provider.

MYTH_BUST — The Credit Score Myth

There's a common myth that credit scores don't matter when it comes to EV insurance. But, this couldn't be further from the truth. Your credit score plays a significant role in determining your premium, and ignoring it can cost you big time. For example, if you've got an excellent credit score, you may be eligible for discounts on your Geico EV insurance premium. On the other hand, a poor credit score can lead to higher rates and even policy cancellations.

Geico EV insurance rates are influenced by a range of factors, including your credit score. But, what about other insurers? Do they use credit scores in the same way? The answer is yes. Most insurers, including Progressive and State Farm, use credit scores to determine premiums. However, the way they use credit scores can vary significantly. Some insurers may place more emphasis on credit scores than others, so it's essential to shop around and compare rates.

One thing that's often overlooked is the impact of credit score changes on EV insurance rates. If your credit score improves or declines significantly, your insurance premium may change accordingly. For instance, if you've recently paid off a large debt and your credit score has improved, you may be eligible for a discount on your Geico EV insurance premium. On the other hand, if your credit score has taken a hit due to unforeseen circumstances, your premium may increase.

Pro tip: Check your credit report regularly and dispute any errors you find. This can help improve your credit score and reduce your EV insurance premium.

OK So Here's the Deal With Geico EV Insurance and Credit Scores

Geico EV insurance rates are competitive, but they can be influenced by your credit score. If you've got a good credit score, you may be eligible for discounts on your premium. On the other hand, a poor credit score can lead to higher rates. So, what can you do to improve your credit score and reduce your Geico EV insurance premium? Start by paying your bills on time, reducing your debt, and avoiding new credit inquiries.

For example, let's say you've got a credit score of 650 and you're paying $2,000 per year for Geico EV insurance. If you improve your credit score to 750, you may be eligible for a discount of up to 20%. That's a savings of $400 per year. And, if you've got an excellent credit score, you may be eligible for even deeper discounts. Some insurers offer discounts of up to 30% for drivers with excellent credit scores.

It's also worth noting that some insurers specialize in EV insurance and may offer more competitive rates for drivers with good credit scores. For instance, Tesla's insurance arm offers discounts of up to 30% for drivers with good credit scores. And, some insurers, like Liberty Mutual, offer usage-based insurance programs that can help reduce your premium.

Can You Really Save Money on Geico EV Insurance With a Good Credit Score?

The answer is yes. A good credit score can save you money on Geico EV insurance. In fact, according to data, drivers with good credit scores pay an average of 20% less for EV insurance than those with poor credit scores. This can translate to significant savings over the life of your policy. For example, if you're paying $2,500 per year for Geico EV insurance, a 20% discount could save you $500 per year.

But, how do you improve your credit score and reduce your Geico EV insurance premium? Start by checking your credit report regularly and disputing any errors you find. You can also work on improving your credit score by paying your bills on time, reducing your debt, and avoiding new credit inquiries. And, don't forget to shop around and compare rates from different insurers. You might be surprised at how much you can save by switching to a different provider.

One thing to keep in mind is that credit scores are just one factor used to determine EV insurance rates. Other factors, such as your driving history and vehicle type, can also impact your premium. For instance, if you've got a history of accidents or tickets, your Geico EV insurance premium may be higher than someone with a clean driving record. And, if you own a high-performance EV, like a Tesla Model S, your premium may be higher than someone who owns a more modest EV, like a Hyundai Kona Electric.

FAQs

#### What is the average cost of Geico EV insurance?

The average cost of Geico EV insurance varies depending on a range of factors, including your credit score, driving history, and vehicle type. However, according to data, the average annual premium for Geico EV insurance is around $1,800.

#### How does my credit score impact my Geico EV insurance rate?

Your credit score can significantly impact your Geico EV insurance rate. Drivers with good credit scores may be eligible for discounts on their premium, while those with poor credit scores may face higher rates.

#### Can I improve my credit score to reduce my Geico EV insurance premium?

Yes, you can improve your credit score to reduce your Geico EV insurance premium. Start by checking your credit report regularly and disputing any errors you find. You can also work on improving your credit score by paying your bills on time, reducing your debt, and avoiding new credit inquiries.

#### What are some other factors that impact Geico EV insurance rates?

Other factors that impact Geico EV insurance rates include your driving history, vehicle type, and location. For instance, if you've got a history of accidents or tickets, your Geico EV insurance premium may be higher than someone with a clean driving record.

#### How can I compare Geico EV insurance rates with other insurers?

You can compare Geico EV insurance rates with other insurers by shopping around and getting quotes from different providers. You can also use online tools and calculators to compare rates and find the best deal.

#### What are some tips for reducing my Geico EV insurance premium?

Some tips for reducing your Geico EV insurance premium include improving your credit score, shopping around and comparing rates, and taking advantage of discounts and promotions. You can also consider increasing your deductible or reducing your coverage limits to lower your premium.

That's my two cents. Take it or leave it — but I hope it helps. — Alex