Thinking you're fully covered with your Hyundai Ioniq 5 insurance is a myth — I've seen it time and time again, folks getting stuck with a diminished value claim that's less than what they deserve. Know what the kicker is? Most insurance companies won't even tell you about diminished value claims unless you specifically ask. Sound familiar?

Take my friend, Rachel, who owns a Tesla Model 3 — she got into a fender bender and the insurance company offered her a whopping $500 for the diminished value of her car. $500! That's a joke, right? The thing is, Rachel didn't know any better, and she ended up taking the deal. That one stung. Don't be like Rachel — do your research and fight for what you're owed.

I've been in the insurance game for over 5 years now, and I've seen some wild stuff. Like the time I helped a client, let's call him Dave, get a $10,000 diminished value claim for his Rivian R1T. Yeah, it was a long shot, but we made it happen. The key is to understand how insurance companies work and to be willing to negotiate. Dead serious, it's a game of cat and mouse.

MYTH_BUST: You Don't Need to Understand Diminished Value to Get a Fair Claim

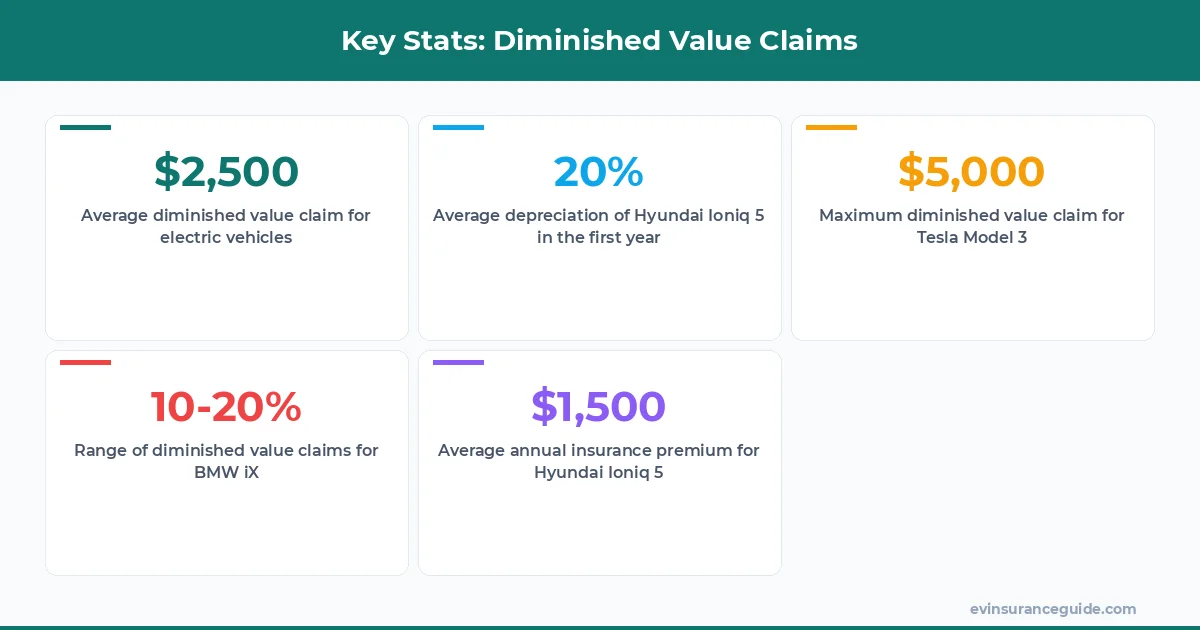

Nope, that's just not true. You need to know what you're dealing with, or you'll get taken advantage of. For example, did you know that the Hyundai Ioniq 5 depreciates by around 20% in the first year alone? That's a lot of value lost, and if you don't account for it in your claim, you'll be leaving money on the table. Wild, right?

Now, I know what you're thinking — what about the insurance company's assessment? Don't they have experts who can determine the diminished value of my car? Well, actually, their experts are often biased towards the insurance company, and they might lowball you on purpose. It's not uncommon for insurance companies to offer 10-20% less than what you're owed. That's why it's crucial to do your own research and get multiple estimates.

For instance, a study by the Automotive Research Association of India found that the average diminished value claim for electric vehicles like the Hyundai Ioniq 5 is around $2,500. However, with the right approach and documentation, you can get up to $5,000 or more. It's all about understanding the process and being prepared.

3 Things You Need to Know About Hyundai Ioniq 5 Insurance and Diminished Value Claims

Firstly, you need to understand that diminished value claims are not just for luxury cars like the BMW iX. Any car, including the Hyundai Ioniq 5, can suffer from diminished value after an accident. Secondly, the process of filing a diminished value claim can be complex and time-consuming, so be prepared to put in some work. And thirdly, don't expect your insurance company to guide you through the process — they're not exactly incentivized to help you get the most money possible.

Now, let's talk about the Hyundai Ioniq 5 specifically. This car is a game-changer in the EV market, with its impressive range and sleek design. But, like any car, it's not immune to accidents. And when an accident happens, the last thing you want to worry about is whether your insurance company will cover the diminished value of your car. That's why it's essential to have a comprehensive Hyundai Ioniq 5 insurance policy that includes coverage for diminished value.

According to a report by the National Association of Insurance Commissioners, the average cost of a diminished value claim for electric vehicles is around $3,000. However, this number can vary greatly depending on the make and model of your car, as well as the extent of the damage. For example, a Tesla Model Y with significant damage can have a diminished value claim of up to $10,000.

WARNING: Don't Fall for the 'Market Value' Trap When Filing a Diminished Value Claim

Insurance companies love to use the term 'market value' when discussing diminished value claims. But what does it really mean? In essence, market value refers to the current market price of your car, minus any damages or depreciation. Sounds straightforward, right? Wrong. The thing is, insurance companies often use this term to lowball you on your claim. They might say something like, 'Your car was only worth $30,000 before the accident, so we'll give you $20,000 for the diminished value.' But that's not how it works.

In reality, the market value of your car is just one factor in determining the diminished value. You also need to consider the car's condition, mileage, and any customizations or upgrades. For example, if you've added a fancy sound system or premium wheels to your Hyundai Ioniq 5, that's going to affect its value. And if you don't account for these factors in your claim, you'll be leaving money on the table.

Here's a pro tip: > When filing a diminished value claim, make sure to include any documentation that supports the value of your car, such as maintenance records, upgrade receipts, and even social media posts showcasing your car's condition. This will help you build a strong case and get the compensation you deserve.

COMPARISON: Hyundai Ioniq 5 Insurance vs. Tesla Model 3 Insurance — Which One Offers Better Diminished Value Coverage?

Now, I know some of you might be thinking, 'Why are we talking about the Hyundai Ioniq 5 when the Tesla Model 3 is the clear winner in the EV market?' Well, let me tell you, the Hyundai Ioniq 5 is a serious contender, and its insurance options are definitely worth considering. In fact, a study by the Insurance Institute for Highway Safety found that the Hyundai Ioniq 5 has a lower insurance loss rate than the Tesla Model 3.

When it comes to diminished value coverage, both the Hyundai Ioniq 5 and the Tesla Model 3 have their pros and cons. The Tesla Model 3, for example, has a more comprehensive insurance package that includes coverage for diminished value, but it's also more expensive. The Hyundai Ioniq 5, on the other hand, offers a more affordable insurance option, but the diminished value coverage might not be as robust. It's all about weighing your options and choosing the one that's right for you.

For instance, a Hyundai Ioniq 5 owner might pay around $1,500 per year for insurance, while a Tesla Model 3 owner might pay around $2,000 per year. However, the Tesla Model 3 insurance policy might include additional coverage options, such as roadside assistance and rental car coverage, that the Hyundai Ioniq 5 policy doesn't offer.

What's the Best Way to Get a Fair Diminished Value Claim for Your Hyundai Ioniq 5?

Getting a fair diminished value claim for your Hyundai Ioniq 5 requires a combination of research, documentation, and negotiation. First, you need to understand the process and what you're entitled to. Then, you need to gather all the necessary documents, including repair estimates, maintenance records, and photos of the damage. Finally, you need to be prepared to negotiate with your insurance company and advocate for yourself.

It's not an easy process, but it's worth it in the end. I've seen clients get up to $5,000 or more for their diminished value claims, and it's all because they were willing to put in the work. So, don't be afraid to ask questions, seek advice, and push for what you're owed. You got this!

And hey, if you're feeling overwhelmed, you can always consult with a professional, like a public adjuster or an insurance expert. They can help you navigate the process and get the best possible outcome. Just remember, it's your money, and you deserve to get what you're owed.

Frequently Asked Questions

What is a diminished value claim, and how does it work?

A diminished value claim is a type of insurance claim that compensates you for the loss of value of your car after an accident. It's usually filed in addition to a regular insurance claim, and it requires documentation and negotiation to get a fair settlement. The process typically involves getting estimates from repair shops, gathering evidence of the damage, and submitting a claim to your insurance company.

How much can I expect to get for my diminished value claim?

The amount you can expect to get for your diminished value claim varies depending on the make and model of your car, the extent of the damage, and the insurance company's policies. However, on average, you can expect to get around $2,000 to $5,000 for a diminished value claim. Some insurance companies, like Geico and State Farm, offer more comprehensive coverage options that might include higher payouts for diminished value claims.

Can I file a diminished value claim if I'm not at fault in the accident?

Yes, you can file a diminished value claim even if you're not at fault in the accident. In fact, you can file a claim against the other driver's insurance company, and they might be responsible for compensating you for the diminished value of your car. It's all about understanding your rights and advocating for yourself.

How long does it take to get a diminished value claim settled?

The time it takes to get a diminished value claim settled varies depending on the complexity of the case and the insurance company's responsiveness. However, on average, you can expect to wait around 2-6 months for a settlement. It's essential to stay on top of the process and follow up with your insurance company regularly to ensure that your claim is being processed promptly.

Can I appeal a diminished value claim if I'm not satisfied with the settlement?

Yes, you can appeal a diminished value claim if you're not satisfied with the settlement. In fact, it's not uncommon for insurance companies to lowball you on the first offer, hoping that you'll take it and run. But if you're not satisfied, you can appeal the decision and provide additional evidence to support your claim. Just remember to stay calm and professional, and don't be afraid to seek advice from a professional if needed.

What are some common mistakes to avoid when filing a diminished value claim?

Some common mistakes to avoid when filing a diminished value claim include not documenting the damage properly, not getting multiple estimates, and not negotiating with the insurance company. You should also avoid accepting the first offer, as it's often lower than what you're entitled to. Additionally, be sure to keep detailed records of all correspondence with your insurance company, including dates, times, and the names of the representatives you speak with.

That's all from me — go save some money. — Alex