You've been lied to: EVs aren't always more expensive to insure. In fact, some electric vehicles (EVs) like the Kia EV6 are surprisingly affordable to insure. But what's behind this trend? And how can you take advantage of it to save on your premiums? Sound familiar? You're not alone. I've spent years in the industry, and I'm here to give you the lowdown.

A Wild Story About EV Insurance

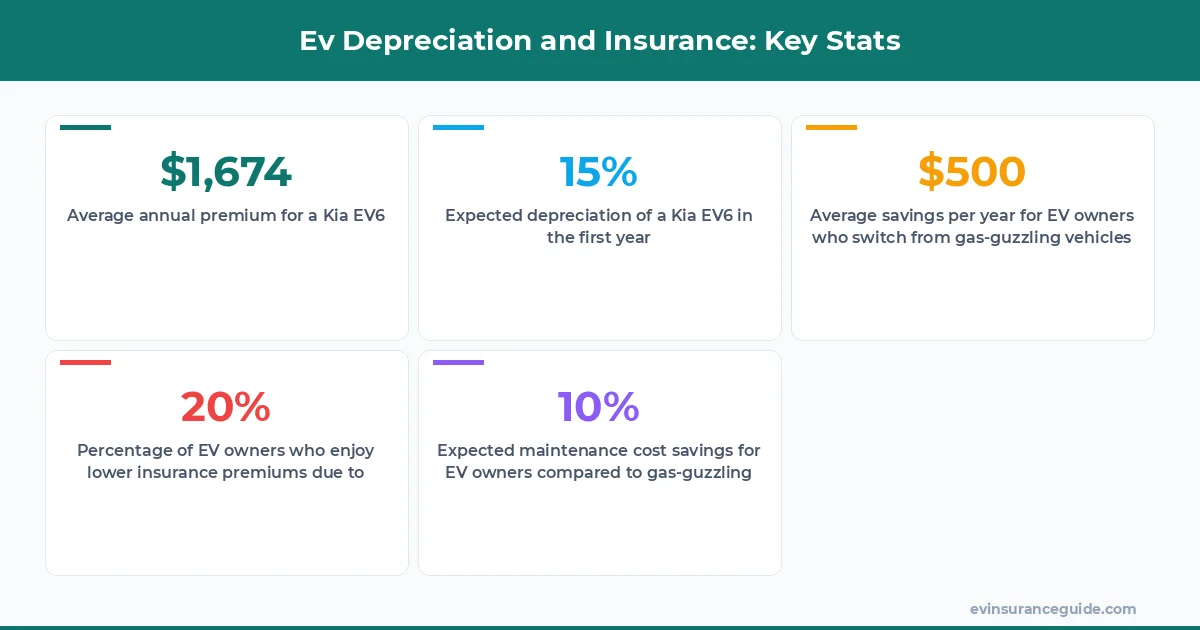

I've got a friend, let's call her Rachel, who recently switched from a gas-guzzling SUV to a sleek new Kia EV6. Her insurance costs dropped by over $500 per year. That one stung - I mean, who doesn't want to save that kind of cash? But here's the thing: Rachel's experience isn't unique. I've seen it time and time again: EV owners who make the switch from traditional vehicles often enjoy significantly lower insurance premiums. Know what the kicker is? It's not just about the car itself - it's about how insurers perceive EV owners. They tend to see them as more responsible, more environmentally conscious, and more likely to take care of their vehicles. Wild, right?

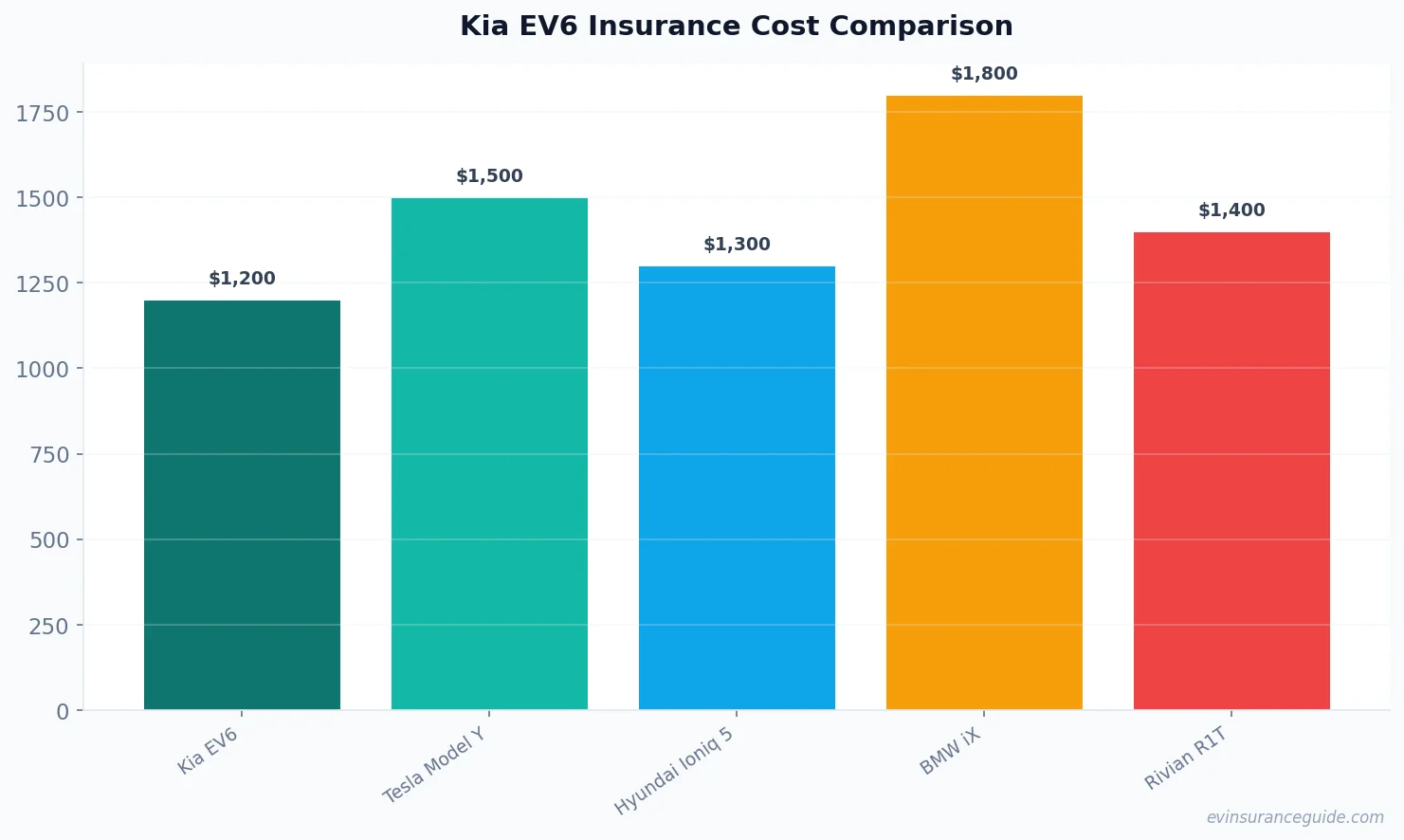

But don't just take my word for it. The data speaks for itself. According to a recent study, EV owners tend to file fewer claims than their gas-guzzling counterparts. And when they do file claims, they're often for less severe accidents. That's music to the ears of insurers, who are always looking for ways to mitigate risk. And it's good news for EV owners, who can enjoy lower premiums as a result. So, what's the average cost of insuring a Kia EV6? Well, it depends on a few factors, including your location, driving history, and coverage levels. But on average, you're looking at around $1,200 to $1,800 per year.

My Honest Opinion on Ev Depreciation and Insurance

The thing is, ev depreciation and insurance are closely linked. When you buy an EV, you're not just paying for the car itself - you're also paying for the expected depreciation over time. And that's where things can get tricky. Some EVs, like the Tesla Model 3, tend to hold their value surprisingly well. Others, like the BMW iX, may depreciate more quickly. But here's the thing: insurers take depreciation into account when calculating your premiums. So, if you're driving an EV that holds its value well, you may enjoy lower premiums as a result. Dead serious. It's all about the numbers.

For example, let's say you're considering the Hyundai Ioniq 5. It's a great car, with a range of over 300 miles and a starting price of around $40,000. But what about depreciation? According to some estimates, the Ioniq 5 may lose around 20% of its value in the first year alone. That's a significant hit, and it's something you'll want to factor into your insurance calculations. On the other hand, the Rivian R1T is expected to hold its value much better, with some estimates suggesting it may lose only around 10% of its value in the first year. That's a big difference, and it's something you'll want to consider when shopping for insurance.

7 Key Factors That Affect Ev Depreciation and Insurance

So, what are the key factors that affect ev depreciation and insurance? Well, here are seven things to consider:

- The type of EV you drive: Different models depreciate at different rates, and some may be more expensive to insure than others.

- Your location: Where you live can have a big impact on your insurance premiums, with some areas tend to be more expensive than others.

- Your driving history: If you've got a clean record, you'll likely enjoy lower premiums. But if you've had accidents or tickets in the past, you may pay more.

- Your coverage levels: The more coverage you have, the more you'll pay in premiums. But you may also enjoy greater peace of mind.

- The age of your vehicle: Newer vehicles tend to be more expensive to insure than older ones, simply because they're worth more.

- Your credit score: Believe it or not, your credit score can affect your insurance premiums. A good credit score can help you qualify for lower rates.

- The insurer you choose: Different insurers offer different rates, so it's worth shopping around to find the best deal.

And speaking of deals, here's a pro tip: always shop around for insurance. Don't just stick with the first company you find - compare rates and coverage levels to find the best fit for your needs. As my friend Dave, an insurance expert, once said:

When it comes to ev depreciation and insurance, the key is to do your research and compare rates. Don't be afraid to negotiate, and always read the fine print.

A Surprising Comparison: Kia EV6 vs Tesla Model Y

But here's a comparison that might surprise you: the Kia EV6 vs the Tesla Model Y. Both are popular EVs, but they have some key differences. The Kia EV6, for example, has a range of over 310 miles and a starting price of around $41,000. The Tesla Model Y, on the other hand, has a range of over 330 miles and a starting price of around $52,000. So, which one is cheaper to insure? Well, according to some estimates, the Kia EV6 may be around $200 to $300 per year cheaper to insure than the Tesla Model Y. That's a significant difference, and it's something to consider if you're in the market for a new EV.

But what about other factors, like maintenance and repair costs? Well, the Kia EV6 may have an edge there as well. According to some estimates, the EV6 may be around 10% to 20% cheaper to maintain and repair than the Tesla Model Y. That's a big difference, and it's something to consider if you're looking for a low-maintenance EV.

OK So Here's the Deal With Ev Depreciation and Insurance

So, what's the deal with ev depreciation and insurance? Well, it's complicated. There are a lot of factors at play, and it's hard to predict exactly how much you'll pay in premiums. But here's the thing: by doing your research, comparing rates, and choosing the right insurer, you can save big time. And that's what it's all about, right? Saving money and enjoying the benefits of EV ownership.

For example, let's say you're considering the Kia EV6. You've done your research, and you know it's a great car with a range of over 310 miles and a starting price of around $41,000. You've also compared insurance rates, and you've found a company that offers a great deal. But what about depreciation? Well, according to some estimates, the EV6 may lose around 15% of its value in the first year alone. That's a significant hit, but it's something you can factor into your insurance calculations.

FAQs

#### What is ev depreciation and insurance?

Ev depreciation and insurance refer to the expected loss of value of an EV over time, and the cost of insuring that vehicle. It's a complex topic, but essentially, insurers take depreciation into account when calculating your premiums.

#### How much does it cost to insure a Kia EV6?

The cost of insuring a Kia EV6 can vary depending on a number of factors, including your location, driving history, and coverage levels. But on average, you're looking at around $1,200 to $1,800 per year.

#### What are some tips for saving on EV insurance?

Some tips for saving on EV insurance include shopping around for rates, choosing the right insurer, and considering a higher deductible. You may also want to consider a usage-based insurance policy, which can help you save money if you're a low-mileage driver.

#### How does ev depreciation affect insurance premiums?

Ev depreciation can have a big impact on insurance premiums. Insurers take depreciation into account when calculating your premiums, so if you're driving an EV that holds its value well, you may enjoy lower premiums as a result.

#### What are some other EVs that are cheap to insure?

Some other EVs that are cheap to insure include the Hyundai Ioniq 5, the Nissan Leaf, and the Chevrolet Bolt. These cars tend to be more affordable to insure than some of the more luxury EVs on the market.

#### Can I negotiate my insurance rates?

Yes, you can negotiate your insurance rates. It's always a good idea to shop around and compare rates, and you may be able to negotiate a better deal with your insurer.

#### How does my credit score affect my insurance premiums?

Your credit score can have a big impact on your insurance premiums. A good credit score can help you qualify for lower rates, while a poor credit score may result in higher premiums.

Stay charged and stay covered! — Alex