Meet Sarah, who bought a brand new Tesla Model 3 for $55,000. She was thrilled, but her excitement was short-lived. A year later, her car was involved in an accident, and the insurance company valued it at $35,000. Sarah still owed $45,000 on her loan, leaving her with a $10,000 gap. That one stung. Fast forward to now, Sarah's got a new BMW iX, and she's not making the same mistake twice - she's got gap insurance. Sound familiar?

MYTH_BUST — Gap Insurance is a Scam

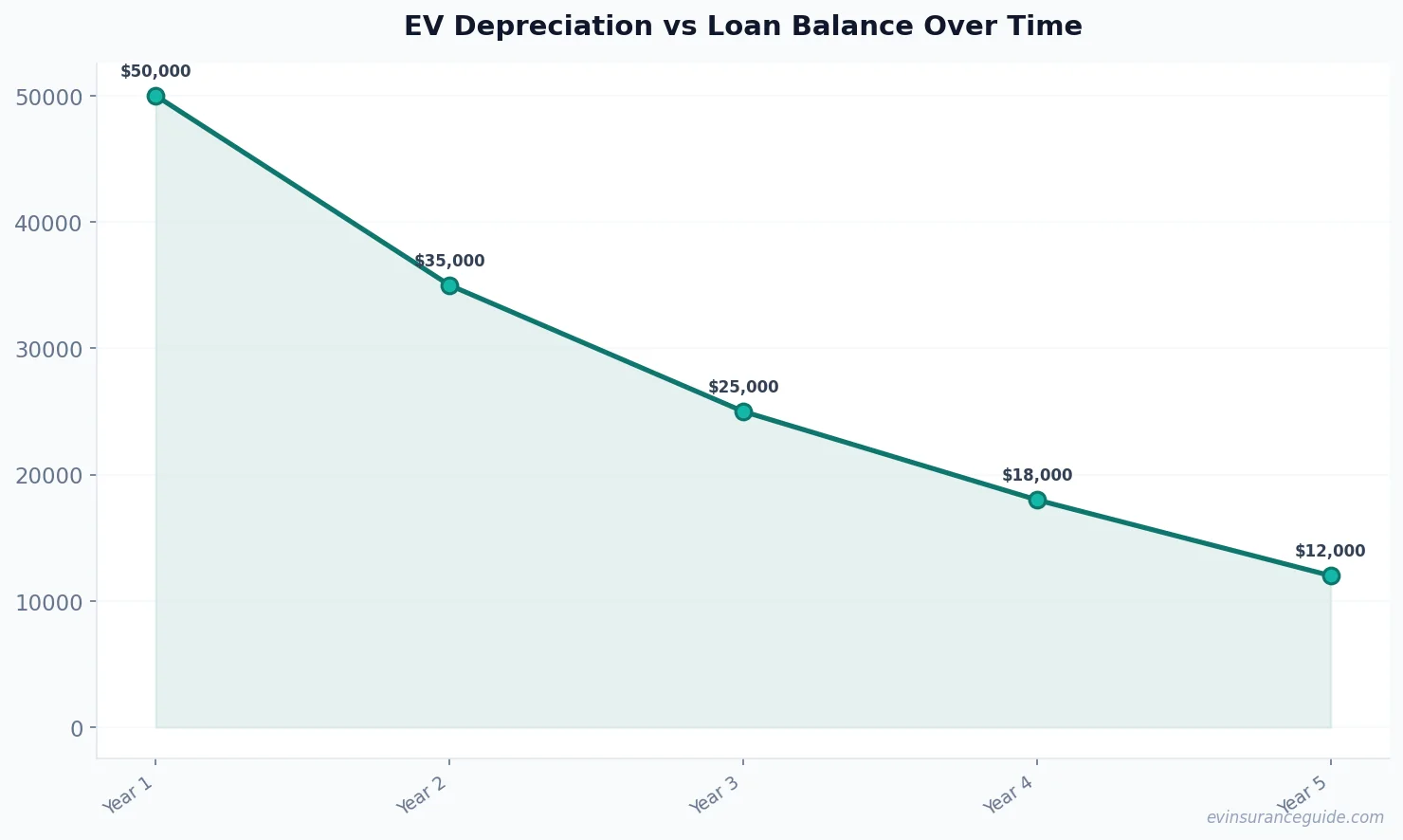

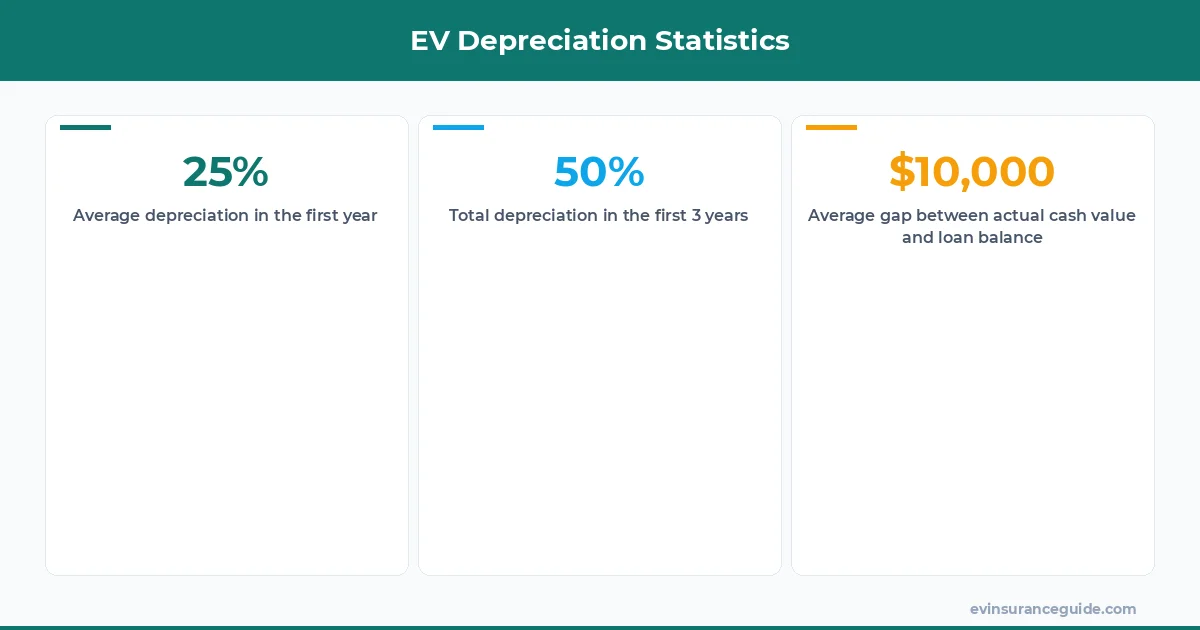

You've probably heard that gap insurance is a waste of money, but that's just not true. Gap insurance can be a lifesaver, especially when you're buying a rapidly depreciating asset like an EV. Know what the kicker is? Most people don't even realize they need gap insurance until it's too late. Take the Hyundai Ioniq 5, for example - it can lose up to 50% of its value within the first three years. Wild, right? That's why gap insurance is crucial, especially if you're planning to own your EV for an extended period.

The average Tesla insurance cost can range from $1,500 to $3,000 per year, depending on your location, driving history, and other factors. But what's often overlooked is the potential gap between your car's actual cash value and the amount you still owe on your loan. This is where gap insurance comes in - it can help you avoid financial disaster. So, how much does gap insurance cost? Well, it's usually around $20 to $30 per year, which is a small price to pay for peace of mind.

But, let's get real - gap insurance isn't always necessary. If you're buying a used EV, or if you've paid off your loan, you might not need it. However, if you're buying a brand new EV, or if you're financing your vehicle, gap insurance is a no-brainer. And, if you're wondering how to lower your Tesla insurance cost, gap insurance can actually help you do that in the long run. Think about it - if you don't have gap insurance and your car gets totaled, you'll be stuck paying off the remaining balance on your loan, which can be financially devastating.

WARNING — Don't Get Caught Off Guard

Don't assume that your regular insurance policy will cover the gap between your car's actual cash value and the amount you still owe on your loan. That's just not how it works. Your regular insurance policy will only cover the actual cash value of your car, which can leave you with a significant gap. For example, let's say you bought a Rivian for $70,000, and a year later, it's involved in an accident. The insurance company values your car at $40,000, but you still owe $60,000 on your loan. Without gap insurance, you'll be stuck paying off the remaining $20,000. That's a huge financial burden, especially if you're not prepared.

And, if you're thinking that gap insurance is only necessary for luxury EVs, think again. All EVs depreciate rapidly, regardless of their price tag. In fact, according to a study by Kelley Blue Book, the average EV loses around 30% of its value within the first year. That's a lot of value to lose, especially if you're not prepared. So, don't get caught off guard - make sure you've got gap insurance to protect yourself from financial disaster.

But, how do you know if you need gap insurance? Well, it's actually pretty simple. If you're financing your EV, or if you're leasing it, you'll probably need gap insurance. And, if you're buying a brand new EV, you should definitely consider it. The cost of gap insurance is relatively low, and it can save you a lot of financial hassle in the long run.

CASUAL_DIRECT — OK So Here's the Deal With Gap Insurance

Gap insurance is actually pretty straightforward. It's an additional insurance policy that covers the gap between your car's actual cash value and the amount you still owe on your loan. It's usually sold as an add-on to your regular insurance policy, and it can be purchased from most insurance companies. The cost of gap insurance varies depending on the insurance company and the value of your vehicle, but it's usually around $20 to $30 per year.

For example, let's say you buy a Tesla Model Y for $50,000, and you finance it through Tesla's financing program. If you don't have gap insurance, and your car gets totaled, you'll be stuck paying off the remaining balance on your loan, which can be financially devastating. But, if you have gap insurance, you'll be protected from that financial burden. And, the best part is, gap insurance can actually help you lower your Tesla insurance cost in the long run.

Pro tip: When shopping for gap insurance, make sure you read the fine print. Some insurance companies might have exclusions or limitations on their gap insurance policies, so it's essential to understand what you're getting. For instance, some policies might not cover vehicles that are more than 5 years old, or vehicles with high mileage.

5 Reasons Why You Need Gap Insurance

You might be wondering why you need gap insurance, especially if you're buying a used EV. But, here are 5 reasons why gap insurance is essential:

- 1. Rapid depreciation - EVs depreciate rapidly, which means that their value can drop significantly within the first few years.

- 2. Financial protection - Gap insurance can protect you from financial disaster if your car gets totaled and you still owe money on your loan.

- 3. Peace of mind - Gap insurance can give you peace of mind, knowing that you're protected from financial burdens.

- 4. Lower Tesla insurance cost - Gap insurance can actually help you lower your Tesla insurance cost in the long run.

- 5. Flexibility - Gap insurance can be purchased as an add-on to your regular insurance policy, which makes it easy to customize your coverage.

HONEST_OPINION — Gap Insurance is a Must-Have

Let's be real - gap insurance is a must-have for anyone buying a new EV. It's not just a nicety, it's a necessity. With the rapid depreciation of EVs, it's essential to have gap insurance to protect yourself from financial disaster. And, if you're thinking that gap insurance is only necessary for luxury EVs, think again. All EVs depreciate rapidly, regardless of their price tag.

In fact, according to a study by the National Automobile Dealers Association, the average EV loses around 25% of its value within the first year. That's a lot of value to lose, especially if you're not prepared. So, don't wait until it's too late - get gap insurance and protect yourself from financial disaster.

FAQs

#### What is gap insurance?

Gap insurance is an additional insurance policy that covers the gap between your car's actual cash value and the amount you still owe on your loan. It's usually sold as an add-on to your regular insurance policy.

#### How much does gap insurance cost?

The cost of gap insurance varies depending on the insurance company and the value of your vehicle, but it's usually around $20 to $30 per year.

#### Do I need gap insurance if I'm buying a used EV?

It depends. If you're buying a used EV, you might not need gap insurance, especially if you're paying cash or if you've paid off your loan. However, if you're financing your vehicle, or if you're leasing it, you should consider gap insurance.

#### Can I purchase gap insurance from any insurance company?

Most insurance companies offer gap insurance, but it's essential to shop around and compare prices. Some insurance companies might offer better rates or more comprehensive coverage, so it's crucial to do your research.

#### How do I know if I need gap insurance?

If you're financing your EV, or if you're leasing it, you'll probably need gap insurance. And, if you're buying a brand new EV, you should definitely consider it. The cost of gap insurance is relatively low, and it can save you a lot of financial hassle in the long run.

#### What's the difference between gap insurance and regular insurance?

Gap insurance covers the gap between your car's actual cash value and the amount you still owe on your loan, while regular insurance covers the actual cash value of your car. Regular insurance won't cover the gap, which can leave you with a significant financial burden.

#### Can I cancel my gap insurance policy at any time?

It depends on the insurance company and the policy. Some insurance companies might allow you to cancel your gap insurance policy at any time, while others might have penalties or fees for early cancellation. It's essential to read the fine print and understand the terms and conditions of your policy.

Well, actually, gap insurance is a pretty simple concept, but it's often misunderstood. And, OK wait, scratch that - it's not that simple. There are a lot of factors to consider, like the value of your vehicle, the length of your loan, and the cost of gap insurance. But, the bottom line is, gap insurance can save you a lot of financial hassle in the long run.

And, if you're still not convinced, just think about it - what's the worst that could happen if you don't have gap insurance? You could end up owing thousands of dollars on a loan for a car that's no longer worth anything. That's a pretty scary thought, especially if you're living on a tight budget.

Stay charged and stay covered! — Alex