Last Tuesday, a guy named Marcus emailed me asking why his Ioniq 5 quote jumped 40%. He figured a three-year-old electric car would slash his bills like clockwork. Turns out his insurer nailed him on replacement costs for that big battery pack. Marcus learned the hard way that older EV cheaper to insure holds true most days but not every single time.

I've seen this pattern for five years now. New EVs carry sky-high values and fresh tech that scares adjusters. Roll the clock forward a couple years and the price drops fast. Still, one nasty surprise keeps popping up on comprehensive coverage. Battery swaps run ten to twenty grand even on older packs. That detail alone stops some policies from falling as low as a gas car would.

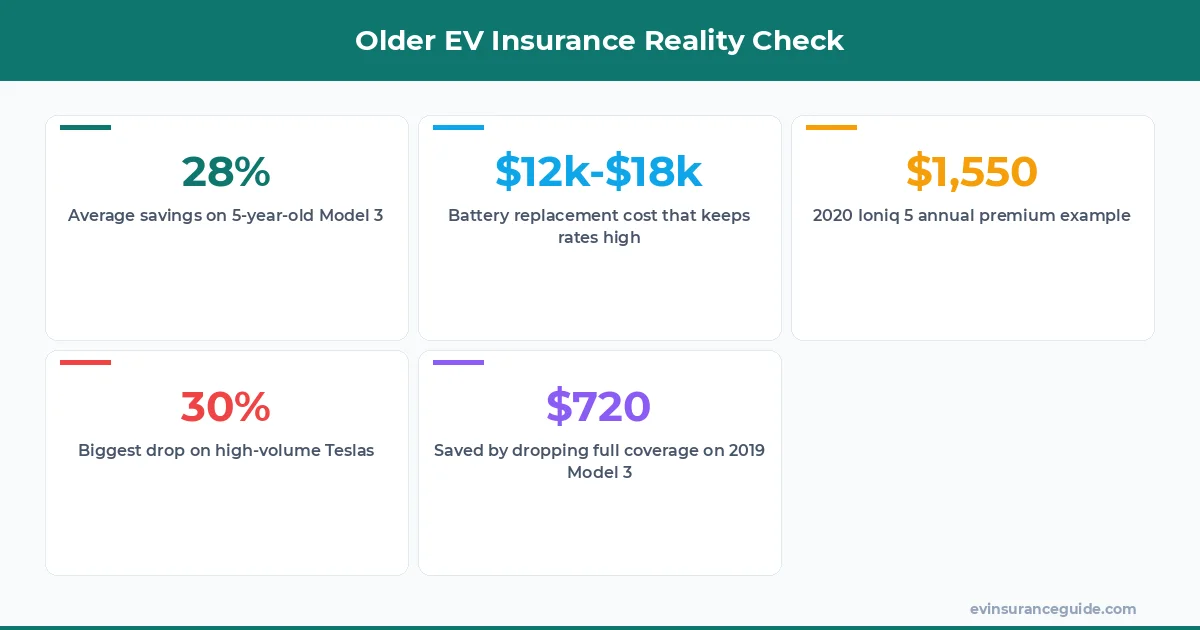

Sound familiar if you've shopped around lately? Drivers expect massive cuts the second they buy used. Reality sits somewhere in the middle. A five-year-old Tesla Model 3 lands 25-35% below new-car rates at most carriers. Hyundai Ioniq 5 owners report similar drops once the original MSRP fades from the books. The savings feel real once you see the actual numbers.

Gas Camry vs Tesla Model 3: The Insurance Surprise After Year Three

People assume any older car saves money the same way. Nope. A five-year-old Toyota Camry drops insurance roughly 45% from new. The same age Tesla Model 3 only saves 28% on average. That gap comes straight from repair complexity and parts pricing. Progressive and Allstate both flag EV-specific labor rates that stay elevated longer than anyone expects.

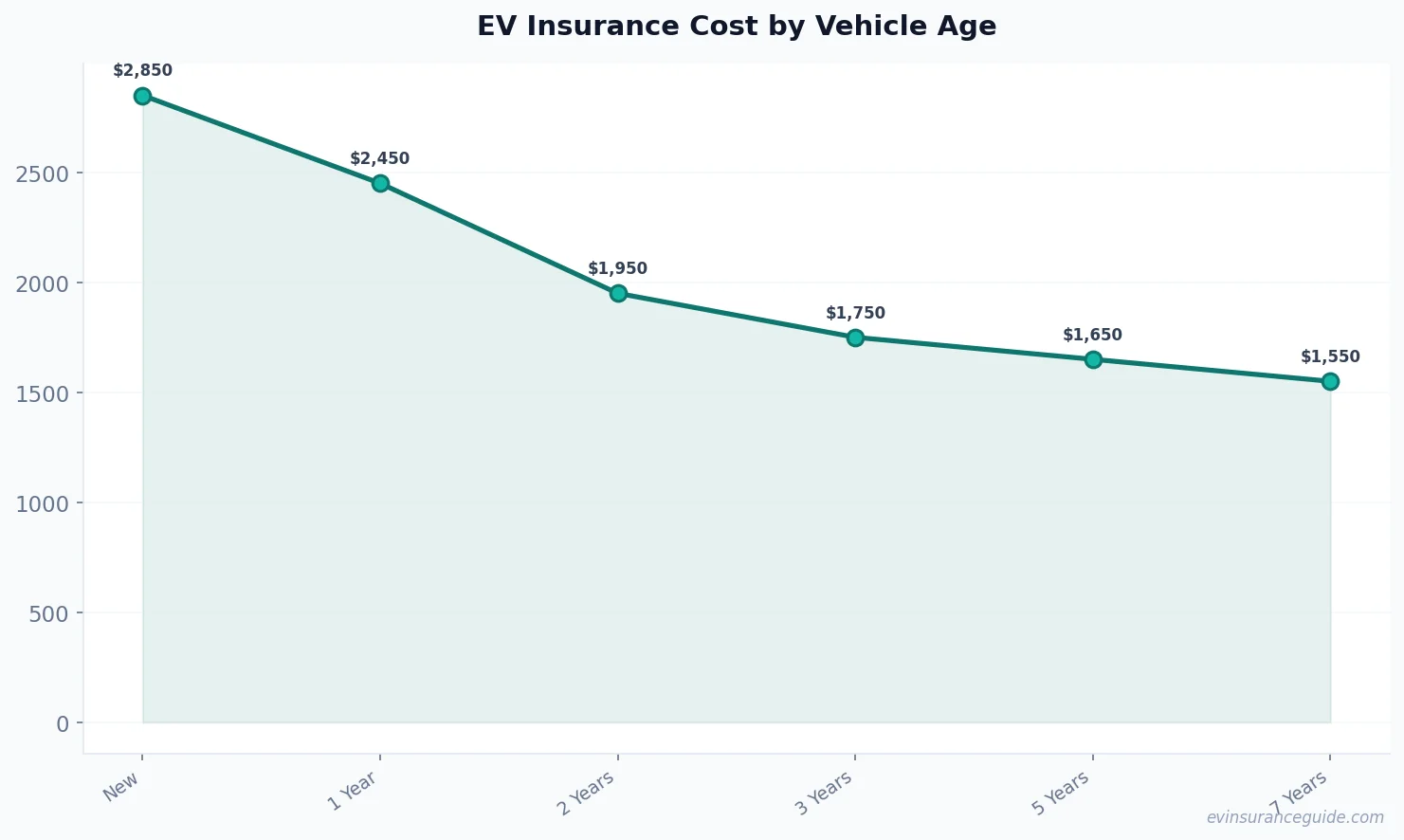

Yet the older EV cheaper to insure story still beats sticking with a brand-new electric. New Model Y policies at State Farm average $2,850 a year in most states. Jump to a two-year-old example and the quote falls to $1,950. The BMW iX follows the same curve but starts from a higher base because of its luxury parts. Rivian trucks hold value too well, which keeps their rates from falling quite as fast.

Know what the kicker is? Collision coverage shrinks faster than comprehensive on these vehicles. Once the car value dips under $25,000 the math changes. Many owners keep full coverage way too long and overpay by hundreds every year.

WARNING: Battery Replacement Costs That Refuse to Drop

Here's the trap nobody mentions until renewal hits. Comprehensive rates on older EVs stay stubbornly high because insurers still price in full battery replacement. Even a five-year-old pack can cost $12,000-$18,000 at Tesla service centers. Geico adds an extra line item for that risk on every policy over four years old.

That single factor stops older EV cheaper to insure from matching gas-car discounts dollar for dollar. A 2019 Model 3 might save $800 a year versus new, yet comprehensive alone eats $300 of those gains. Hyundai Ioniq 5 owners see the same math unless they switch to a carrier that offers EV battery riders at lower rates.

Dead serious about cutting costs? Check your policy declarations page. If comprehensive still lists the original battery value you're leaving money on the table. Ask for a revised valuation using current used-pack prices and watch the premium move.

Myth Busted: Not Every Older EV Gets the Same Discount

The internet loves blanket statements. "Buy any used EV and insurance plummets." That's garbage. A loaded Rivian R1T holds value so well that its insurance barely budges after three years. Meanwhile a base Tesla Model 3 sheds value quicker and drops rates accordingly.

Insurance companies run their own actuarial tables. Tesla Model Y from 2021 sees 30% savings at most carriers. The same-year BMW iX only manages 18% because repair networks stay expensive. Older EV cheaper to insure works best on high-volume models with cheap aftermarket parts. Low-volume luxury EVs fight that trend every renewal cycle.

One more data point: 2022 Ioniq 5 policies averaged $2,100 last quarter at Progressive. Drop to a 2020 model and the same driver pays $1,550. The difference isn't just age. It's parts availability and how many body shops already know the car.

5 Older EVs That Actually Cut Insurance the Most

Start with the Tesla Model 3 from 2020-2021. High volume means lower repair costs and better data for underwriters. Next comes the Hyundai Ioniq 5 2022 models once they clear the initial depreciation wave. Both routinely beat new-car quotes by 30% or more.

Third pick: 2021 Tesla Model Y. Slightly higher than the sedan but still strong savings. Fourth: early BMW iX examples if you can find one with clean history. The discount isn't huge but the car itself qualifies for some specialty EV discounts at USAA and Liberty Mutual. Fifth spot goes to any low-mileage 2019-2020 Model 3 Performance. These already lost most of their value so the insurance math works in your favor.

Question is which one fits your driving habits and local repair options. Run quotes on two or three before you commit.

OK So Here's the Deal With Dropping Comprehensive on Older EVs

Once the car value falls below $20,000 the conversation changes. Comprehensive and collision together can add $600-$900 a year on a five-year-old Model 3. If you're okay self-insuring the battery and body damage, dropping both coverages often makes sense.

Still keep liability solid. That's non-negotiable. But older EV cheaper to insure reaches its maximum when you stop paying for full replacement on a car that's already depreciated hard. State Farm lets you request a valuation adjustment at renewal. Do it.

One client saved $720 last year by switching to liability-only after her 2019 Model 3 appraisal came back at $18,400. The math was simple once she saw the actual numbers.

How much can I realistically save on a five-year-old Tesla Model 3?

Expect 25-35% off new-car rates at carriers like Progressive and Geico. Real quotes for a clean-record driver in a mid-cost state land between $1,400 and $1,700 annually. Battery valuation adjustments can trim another $150-$250 if you request them.

When should I drop comprehensive coverage on an older EV?

Consider it once the car's market value dips under $22,000. At that point the premium often exceeds the risk. Keep liability and uninsured motorist coverage in place though.

Do all insurers treat battery replacement the same way?

No. State Farm and Allstate still price full pack replacement even on older vehicles. Some regional carriers use depreciated values and save you money. Shop three quotes minimum.

Is a 2-3 year old EV the real sweet spot?

Yes. You keep most factory warranty coverage while the car has already lost 30-40% of original value. Insurance drops noticeably without the oldest-battery headaches.

Which EV model sees the biggest insurance drop after year four?

The Tesla Model 3 wins here because of parts volume and body-shop familiarity. Expect closer to 35% savings versus new. The BMW iX trails at roughly 20%.

Can I get EV-specific discounts on older models?

Many carriers still offer them. Ask about green-vehicle or safety-feature credits even on used Teslas and Ioniqs. These small breaks add up over time.

Does mileage affect older EV insurance more than gas cars?

Sometimes. Low-mileage older EVs can qualify for extra discounts because batteries degrade slower. High-mileage examples may see slight increases once you pass 80,000 miles.

Pro tip: Request a current battery valuation at every renewal. One phone call with your agent can save hundreds without changing carriers.

Older EV cheaper to insure works when you match the right model with the right coverage limits. The 2-3 year window gives the cleanest math for most drivers.

Happy driving, and don't overpay! — Alex