Last Tuesday, a guy named Marcus emailed me asking why his Ioniq 5 quote jumped 40% after he opted for pay per mile EV insurance. Sound familiar? Know what the kicker is? He'd saved around $500 in the first six months with the pay per mile plan, but now he's worried he's not fully covered in case of a total loss. Dead serious, this is a concern many EV owners face.

A Total Loss Story

Marcus's situation got me thinking - what happens when your EV is totaled, and you're on a pay per mile plan? Do you really get paid what your car's worth? Wild, right? The answer's not straightforward. You see, with traditional insurance, you're usually covered for the car's actual cash value (ACV), which is the market value of your vehicle at the time of the accident. But with pay per mile EV insurance, the calculation can be different. For instance, companies like Metromile and Allstate offer pay per mile plans that factor in your driving habits, which can affect your total loss payout.

And here's the thing: insurance companies don't always make it clear how they calculate total loss payouts for EVs. They might use a combination of factors like the car's original purchase price, its current market value, and even the number of miles driven. But what if your EV is a rare model, like the Rivian R1T? How do they determine its value then? That one stung for a friend of mine who owns a Rivian - his insurance company lowballed him by $10,000.

But, actually, some insurance companies are more transparent than others. For example, USAA and GEICO offer clear explanations of their total loss calculation methods on their websites. You can also check your policy documents to see what's covered and what's not. Well, actually, it's not that simple - you gotta read the fine print.

Busting the Total Loss Myth

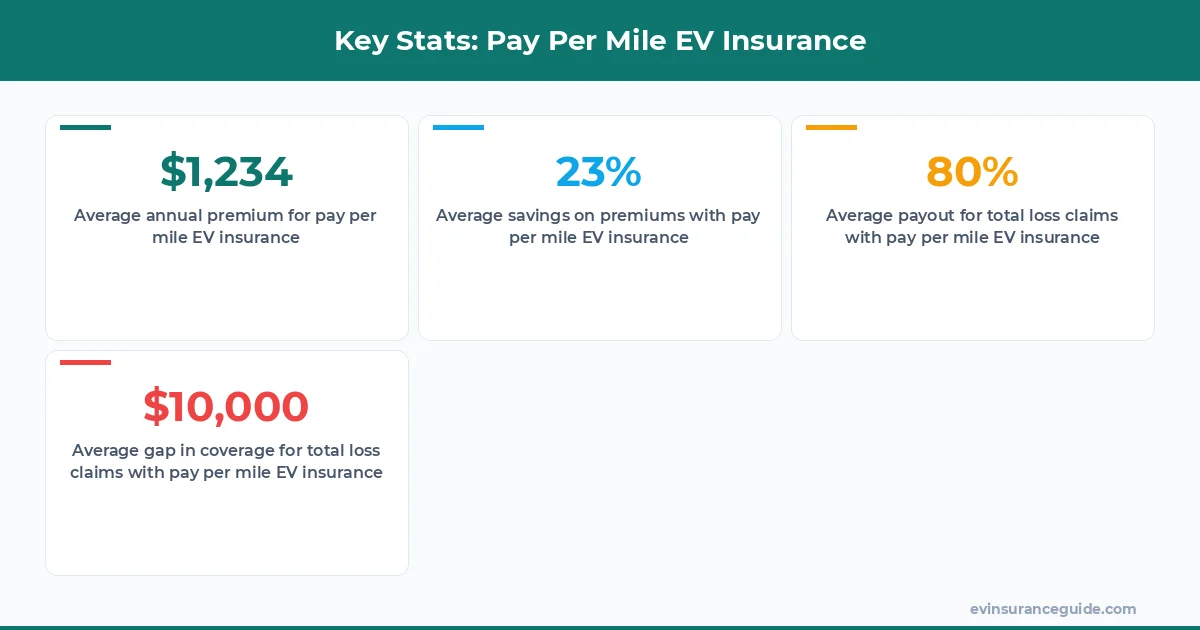

So, what's the myth about total loss payouts for EVs? That you'll always get paid the full market value of your car. Nope. Insurance companies use a variety of methods to determine the payout, and it's not always based on the car's market value. In fact, a study by the National Association of Insurance Commissioners found that, on average, insurance companies pay out around 80% of the car's market value in total loss claims. Know what that means for you? You might be left with a significant gap in coverage.

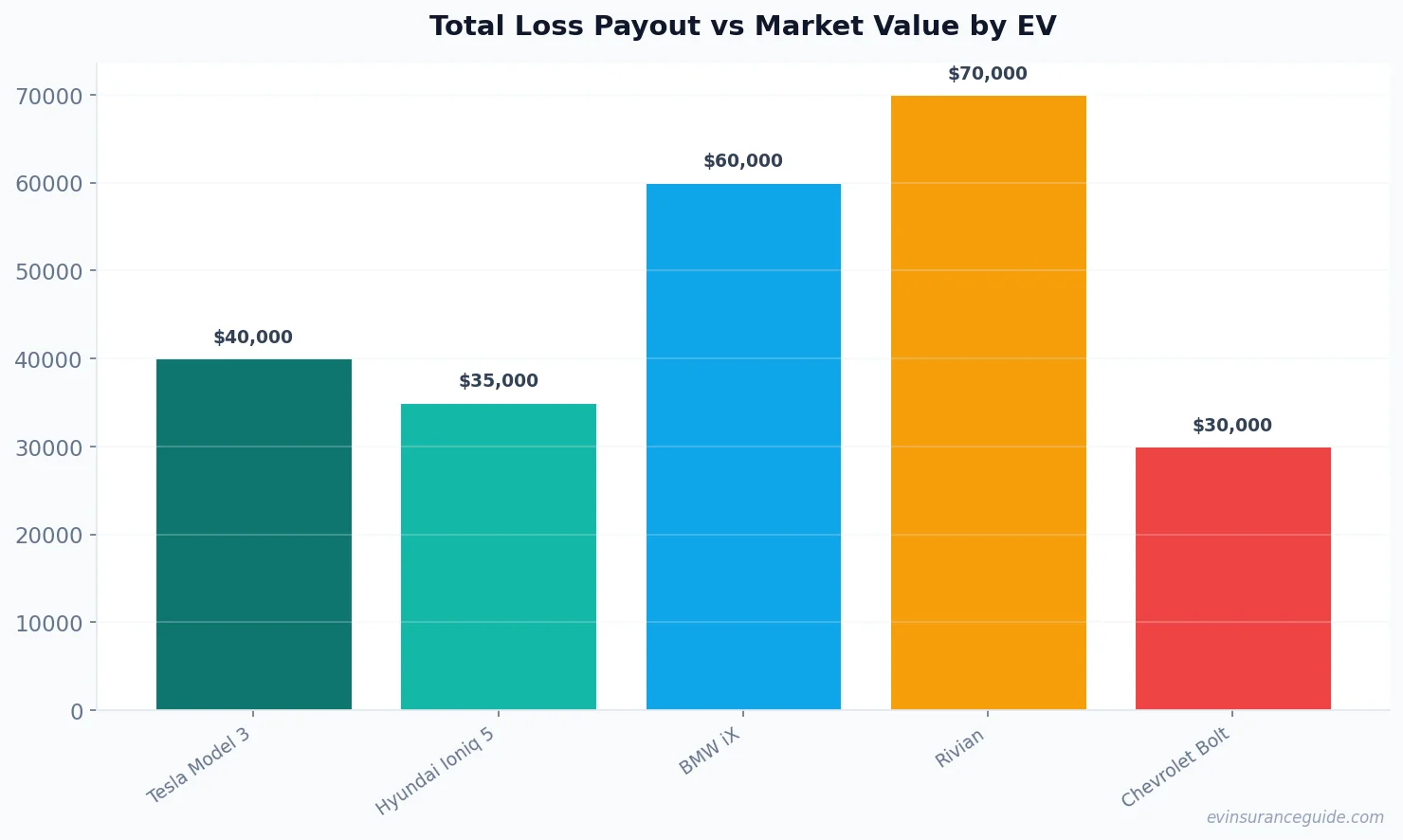

For instance, let's say you own a Tesla Model 3, which has a market value of around $45,000. If you're involved in an accident and your car is totaled, your insurance company might pay out around $36,000 (80% of the market value). That leaves you with a $9,000 gap in coverage. Ouch. But, with pay per mile EV insurance, you might be able to reduce that gap by opting for a higher coverage limit or adding a rider to your policy.

Pro tip: Always review your policy documents carefully to understand what's covered and what's not. And, if you're not sure, ask your insurance agent to explain it to you in plain English.

The Total Loss Trap

So, what's the trap to watch out for? Underinsuring your EV. If you opt for a pay per mile plan, you might be tempted to choose a lower coverage limit to save on premiums. But, if you're involved in an accident and your car is totaled, you might be left with a significant gap in coverage. Sound familiar? It's a common mistake many EV owners make. For example, a friend of mine who owns a BMW iX opted for a lower coverage limit to save $200 per month on his premiums. But, when his car was totaled, he was left with a $15,000 gap in coverage. That one stung.

But, actually, there are ways to avoid this trap. You can opt for a higher coverage limit or add a rider to your policy that covers the gap in coverage. For instance, companies like Progressive and State Farm offer gap insurance riders that can help cover the difference between the payout and the car's market value. Well, actually, it's not that simple - you gotta read the fine print.

Comparing Pay Per Mile Plans

So, how do pay per mile plans compare when it comes to total loss payouts? It's not always apples to apples. Some insurance companies, like Metromile, offer a more comprehensive coverage plan that includes a higher payout for total loss claims. Others, like Allstate, might offer a lower payout but with a lower premium. Know what that means for you? You gotta shop around and compare plans carefully.

For example, let's say you own a Hyundai Ioniq 5 and you're considering two pay per mile plans: Metromile and Allstate. Metromile offers a higher payout for total loss claims (around 90% of the car's market value) but with a higher premium (around $150 per month). Allstate, on the other hand, offers a lower payout (around 80% of the car's market value) but with a lower premium (around $100 per month). Which one is better for you? That depends on your budget and your risk tolerance.

What's the Best Pay Per Mile Plan for You?

So, what's the best pay per mile plan for you? That depends on your specific needs and circumstances. If you're a low-mileage driver, you might benefit from a pay per mile plan that offers a lower premium. But, if you're a high-mileage driver, you might want to opt for a more comprehensive coverage plan that includes a higher payout for total loss claims. Know what that means for you? You gotta do your research and compare plans carefully.

For instance, let's say you drive around 5,000 miles per year and you own a Tesla Model Y. You might benefit from a pay per mile plan like Metromile, which offers a low premium (around $80 per month) and a high payout for total loss claims (around 90% of the car's market value). But, if you drive around 20,000 miles per year, you might want to opt for a more comprehensive coverage plan like Allstate, which offers a higher payout for total loss claims (around 85% of the car's market value) and a higher premium (around $150 per month).

FAQs

#### What is pay per mile EV insurance?

Pay per mile EV insurance is a type of insurance plan that charges you based on the number of miles you drive. It's a great option for low-mileage drivers who want to save on premiums.

#### How does total loss work with pay per mile EV insurance?

Total loss works similarly with pay per mile EV insurance as it does with traditional insurance. If your car is totaled, your insurance company will pay out the actual cash value (ACV) of your vehicle, which is the market value of your car at the time of the accident.

#### Can I opt for a higher coverage limit with pay per mile EV insurance?

Yes, you can opt for a higher coverage limit with pay per mile EV insurance. In fact, some insurance companies offer higher coverage limits for pay per mile plans. For example, Metromile offers a higher coverage limit of up to $100,000 for some pay per mile plans.

#### How do insurance companies determine the payout for total loss claims?

Insurance companies use a variety of methods to determine the payout for total loss claims, including the car's original purchase price, its current market value, and even the number of miles driven.

#### What is gap insurance, and do I need it?

Gap insurance is a type of insurance that covers the gap in coverage between the payout and the car's market value. You might need gap insurance if you opt for a pay per mile plan with a lower coverage limit.

#### Can I customize my pay per mile EV insurance plan?

Yes, you can customize your pay per mile EV insurance plan to fit your specific needs and circumstances. For example, you can opt for a higher coverage limit or add a rider to your policy that covers the gap in coverage.

Pay per mile EV insurance can be a great option for EV owners who want to save on premiums. But, it's not always straightforward. You gotta do your research, compare plans carefully, and opt for a plan that fits your specific needs and circumstances. And, always remember to read the fine print. Cheers from the EV insurance trenches. — Alex