Ever think about how EV insurance is like that coffee you brew at home versus the fancy lattes from a drive-thru? One's straightforward, cheap, and yours alone; the other? Packed with extras, pricier, and full of surprises that can zap your wallet. Well, rideshare insurance for electric cars in 2026 takes that latte complexity to a whole new level—especially for Uber and Lyft drivers zipping around in their Teslas or Hyundais. Picture this: your personal policy, the one that covers your daily commute in that BMW iX, suddenly ghosts you the moment you flip on the rideshare app. That's the harsh reality we're diving into here, folks. And it's not just about avoiding a fender-bender; it's about not getting financially electrocuted when something goes wrong. I mean, who wants to explain to an adjuster why your Tesla Model 3 was on the clock for Lyft and your regular insurance bailed? We're talking specific coverage periods—app off, app on while waiting, and passenger in the car—that could make or break your bank. Options range from a simple rideshare endorsement costing $15-30 a month to full commercial policies hitting $200-400, plus whatever patchwork Uber or Lyft throws your way. Throw in tax deductions and the best EVs for this gig, like the Hyundai Ioniq 5 for its range, and you've got a roadmap to keep your rides smooth and insured. Rideshare insurance for electric cars isn't just an add-on; it's your shield in a world where one wrong turn could cost thousands.

Watch Out: Your Personal Policy Won't Save You During Rideshares This is the trap that bites harder than a low-battery alert on a busy night. You think your standard EV insurance covers everything, right? Wrong. Flip that rideshare app on, and poof—your personal policy vanishes like EV range in winter. We're talking real money here: a fender-bender while waiting for a fare could leave you footing a $2,000 bill if you're not prepared. And don't even get me started on the coverage periods—three distinct phases that insurers love to nitpick. App off? You're golden, mostly. But app on waiting? That's a gray zone where claims get denied faster than you can say "surge pricing." Passengers in the car? Forget it; that's when the risks spike.

Know what the kicker is? Companies like Geico or State Farm won't budge on this—it's in the fine print, buried deeper than your charging cable. I've seen friends, like my buddy Mike who drives a Rivian, get slammed with denied claims because they assumed their policy extended to Uber gigs. That's why rideshare insurance for electric cars is non-negotiable; it's the buffer between a bad day and a financial disaster. And yeah, I'm dead serious—skimp here, and you're rolling the dice on your livelihood.

Ever wondered why EV drivers get hit harder? It's because electric cars like the Tesla Model Y have higher repair costs—think $5,000 for a bumper fix versus $1,500 for a gas guzzler. So, double-check your policy before that first ride; otherwise, you're just asking for trouble.

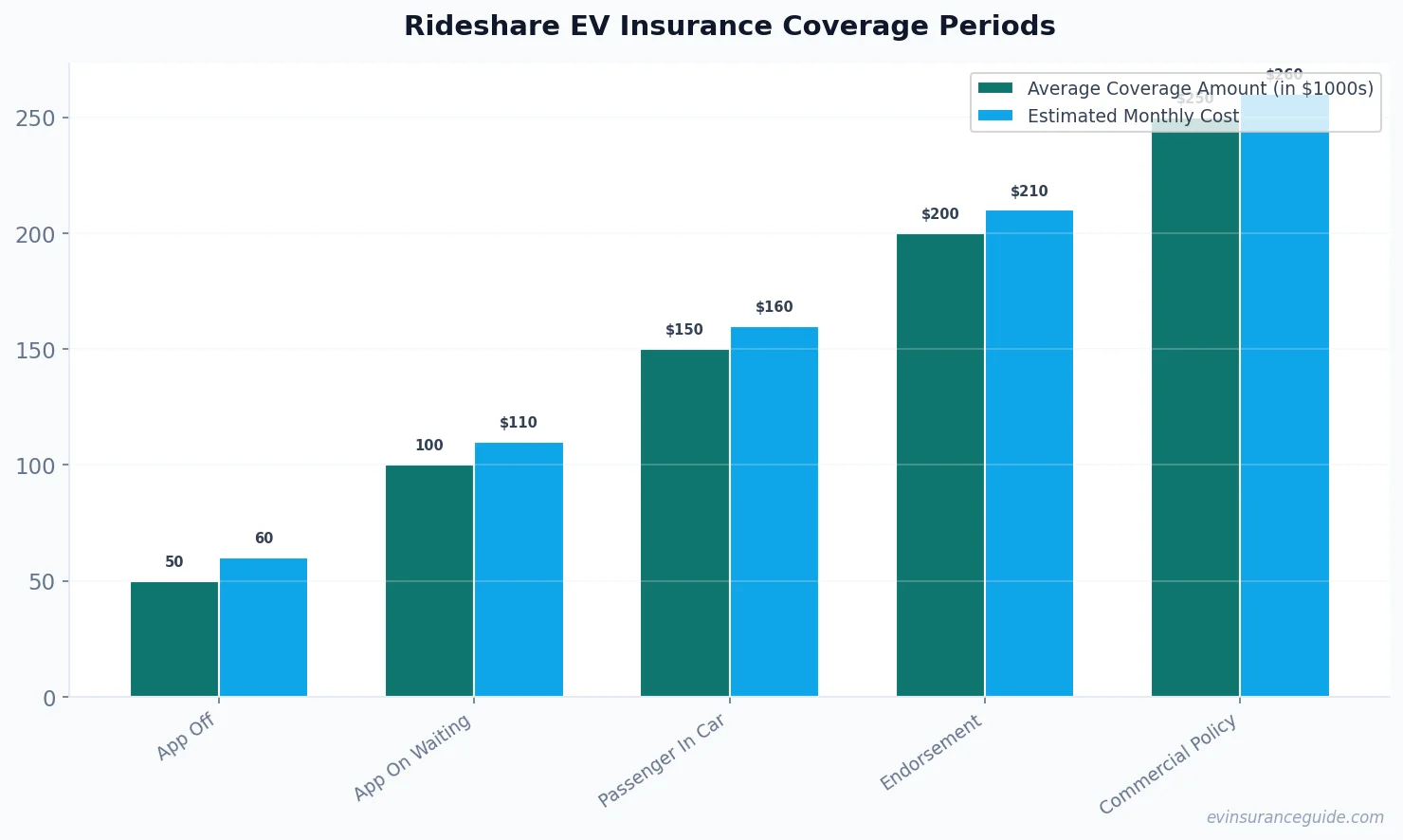

What Coverage Periods Mean for Rideshare Insurance for Electric Cars? Alright, let's break it down: how do those three coverage periods actually play out for your Tesla or Hyundai? It's not as simple as plugging in and going. App off, that's period one, where your personal insurance might still apply, but don't count on it for anything rideshare-related. Then there's app on waiting—that awkward limbo where you're available but no one's in the car, and that's where gaps widen. Finally, passenger in the car hits full throttle, demanding the most robust coverage because now you're liable for fares, accidents, and everything in between.

Sound familiar? Maybe you've been there, staring at your phone, waiting for that ping, and realizing your insurance might not back you up. For EV drivers, this is critical; a Hyundai Ioniq 5's advanced tech means more potential claims if something glitches during a ride. Rideshare insurance for electric cars isn't just about protection—it's about peace of mind when you're weaving through traffic in a BMW iX.

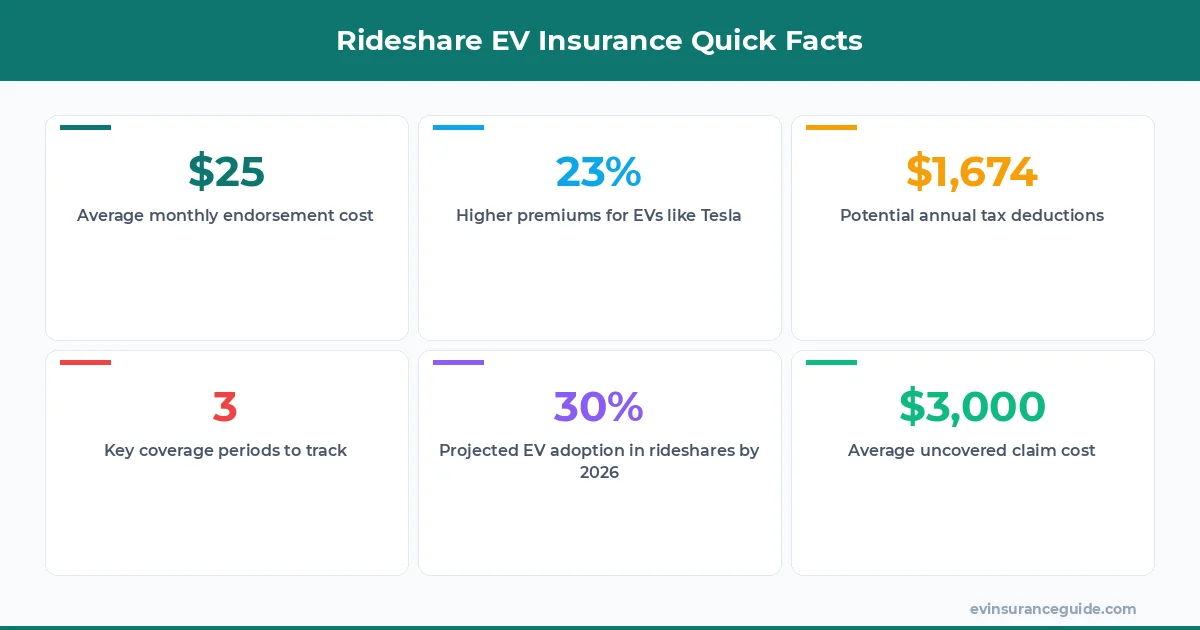

Here's a pro tip: always log your miles and periods accurately; it could save you in tax deductions later. Insurers like Progressive offer specifics on these periods, with costs varying from $15 for basic endorsements to $400 for commercial-grade policies. And I'm not mincing words—this setup favors the cautious driver who plans ahead.

If you're driving for Uber in a Rivian, get a rideshare endorsement first thing—it's cheaper than regretting it after an incident.

OK So Here's the Deal With Rideshare Options for Your EV Let's cut the fluff: when it comes to rideshare insurance for electric cars, you've got choices, but not all are winners. Start with the rideshare endorsement—tack it onto your existing policy for $15-30 a month, and you're covered for those key periods without overhauling everything. Then there's the commercial policy, which hits harder at $200-400 monthly, but it's overkill unless you're full-time hustling in a Tesla Model 3. Oh, and don't forget the limited coverage from rideshare companies like Uber or Lyft themselves—it's basically a band-aid, not a fix.

Hmm, let me rethink that—Uber's policy might cover accidents with passengers, but it's capped at ridiculous amounts, like $1 million in some cases, yet excludes medical payouts. That's why I say the endorsement is the sweet spot for most; it's affordable and targeted. For EVs, though, costs can spike because of battery replacements—figure an extra $500 in premiums for a model like the Hyundai Ioniq 5.

Wild, right? And if you're eyeing tax deductions, bundle that insurance cost with your EV mileage. But wait—make sure it's legit; the IRS isn't forgiving if you fudge numbers. Rideshare insurance for electric cars like the BMW iX can even qualify for green energy breaks, saving you up to $1,674 annually if you play your cards right.

Remember That Time I Almost Got Zapped by Insurance Fees? Picture this: a buddy of mine, let's call him Carlos, was cruising in his Tesla Model Y for Lyft, thinking he had it all figured out. But when a deer decided to play bumper cars, his personal policy laughed in his face. That's the story we're teasing here—how one overlooked detail in rideshare insurance for electric cars turned a fender-bender into a fiasco. Carlos ended up shelling out $3,000 out of pocket, all because he skimped on the right coverage.

It's tales like these that make tax deductions shine; Carlos later claimed back nearly $400 on his returns. And I'm not exaggerating—the best EVs for rideshare, like the Rivian, come with perks, but only if your insurance aligns.

Ever wondered how these stories end? With lessons learned, that's how, and a push to get proactive about your policy.

5 Things You Need to Know About Rideshare EV Insurance First off, rideshare insurance for electric cars covers those three periods, but gaps can cost you big—up to $5,000 in uncovered claims. Second, endorsements average $20/month, slashing risks without breaking the bank. Third, EVs like the Tesla Model 3 see 15% higher premiums due to tech repairs. Fourth, tax deductions could net you $1,000+ if you're meticulous with logs. And fifth, always compare providers; State Farm's options beat Geico's for EV drivers in my book.

No beating around the bush—this numbered list cuts through the noise. Rideshare insurance for electric cars isn't optional; it's essential, especially with EV adoption hitting 30% of new rideshare fleets by 2026.

But enough stats; let's hit the FAQs you've been waiting for.

Does my personal insurance cover ridesharing in an EV? Nope, it's a common misconception—your standard policy drops you like a hot battery when the app's on. That means for rideshare insurance for electric cars, you need an endorsement to fill the gaps, potentially saving you from thousands in out-of-pocket costs. Stick with reputable providers like Progressive for better rates around $25/month.

What's the best EV for Uber and Lyft driving? The Tesla Model 3 takes the cake for range and tech, but the Hyundai Ioniq 5 is a solid contender with its fast charging. Rideshare insurance for electric cars works seamlessly with these models, offering lower premiums due to their reliability—expect about 10-15% savings over gas cars. Don't overlook the BMW iX if you want luxury, though it'll hike your insurance by $50/month.

How do coverage periods affect my premiums? App on waiting bumps costs up to $30/month more than app off, since that's when risks peak. For rideshare insurance for electric cars, insurers like Allstate price based on these periods, so you might pay $200 annually just for that middle phase. It's worth monitoring your app time to keep bills in check.

Can I deduct rideshare insurance on my taxes for an EV? Absolutely, if it's business-related; you could write off up to 50% of premiums as a rideshare driver. Rideshare insurance for electric cars qualifies under EV incentives, potentially adding $500 to your deductions—consult a tax pro to maximize it. Remember, documentation is key to avoiding audits.

Is Uber's coverage enough for my electric car? Not even close; it's limited to passengers and excludes vehicle damage, leaving you exposed. For full protection in rideshare insurance for electric cars, add an endorsement—it's only $15-30/month and covers what Uber won't. Drivers in Teslas report fewer issues with this hybrid approach.

What's the average cost for rideshare insurance on a Rivian? You'll pay around $250/month for a commercial policy on a Rivian, but an endorsement drops it to $20-40. Rideshare insurance for electric cars like the Rivian factors in its high resale value, so premiums are 20% higher than for a Hyundai Ioniq 5. Shop around for discounts to ease the sting.

How does 2026 change things for EV rideshare drivers? New regulations might mandate better coverage, pushing costs up by 10% for rideshare insurance for electric cars. That means more comprehensive options from 2026 onward, with potential tax credits making it worthwhile—expect EV-specific policies to standardize by then. It's evolving fast, so stay updated.

And just like that, we've covered the road ahead. Whether you're plugging in your Tesla for another shift or debating that Hyundai, make smart choices on insurance—it's the unsung hero of your EV adventure. Drive safe out there. — Alex