EV insurance is a rip-off — or at least, that's what I thought before I dug into the world of telematics data. You see, most insurance companies are still using outdated methods to determine your premium, like your age, location, and driving history. But what if I told you that your car can report back to the insurance company, giving them a real-time snapshot of your driving habits? Wild, right? That's where telematics data comes in — and it's changing the game for EV owners like you.

MYTH_BUST: Telematics Data is Invasive

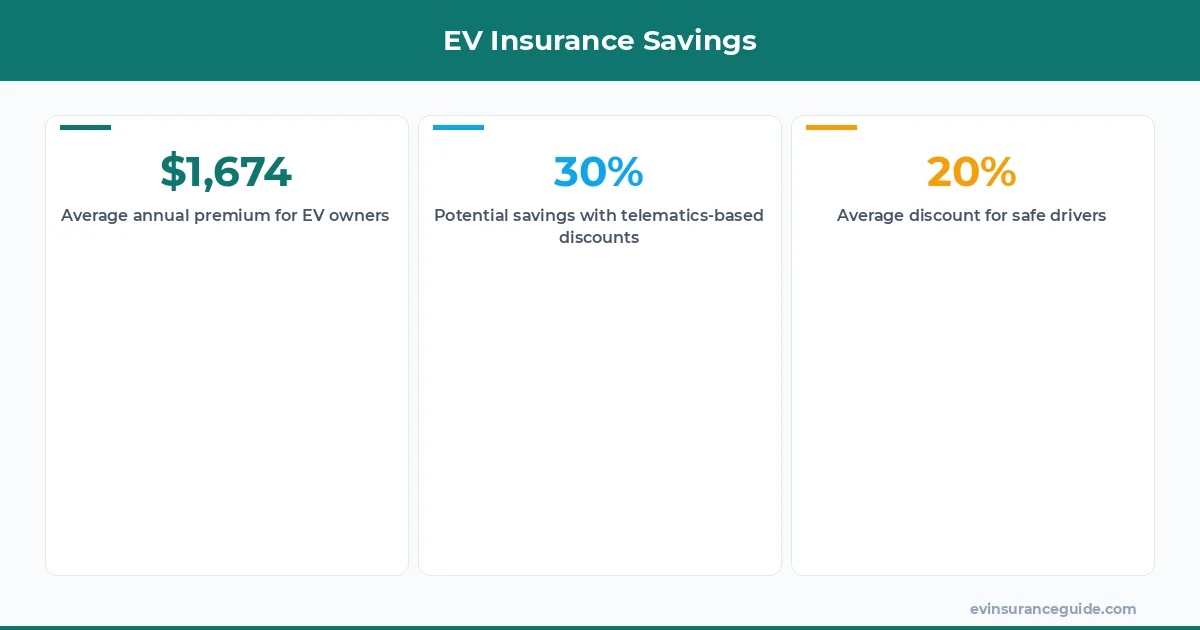

I know what you're thinking: "Isn't telematics data just a way for insurance companies to spy on me?" Nope. It's actually a way for you to prove that you're a safe driver and earn discounts on your premium. For example, if you own a Tesla Model 3, you can opt-in to Tesla's telematics program, which tracks your driving habits and reports back to the insurance company. This can lead to significant savings — we're talking up to 20% off your annual premium.

But here's the thing: not all insurance companies are created equal. Some, like Geico and Progressive, are already using telematics data to offer personalized rates. Others, like State Farm and Allstate, are still playing catch-up. So, if you're looking to save money on your EV insurance, it's worth shopping around and finding a company that offers telematics-based discounts. Know what the kicker is? You can save even more if you bundle your EV insurance with other policies, like home or renters insurance.

For instance, let's say you're a 35-year-old driver with a clean record, and you own a BMW iX. Your annual premium could range from $1,500 to $3,000, depending on the insurance company and the level of coverage you choose. But with telematics data, you could potentially save up to $600 per year. That's a significant chunk of change — and it's all because you're willing to share your driving data with the insurance company.

OK So Here's the Deal With Telematics Data

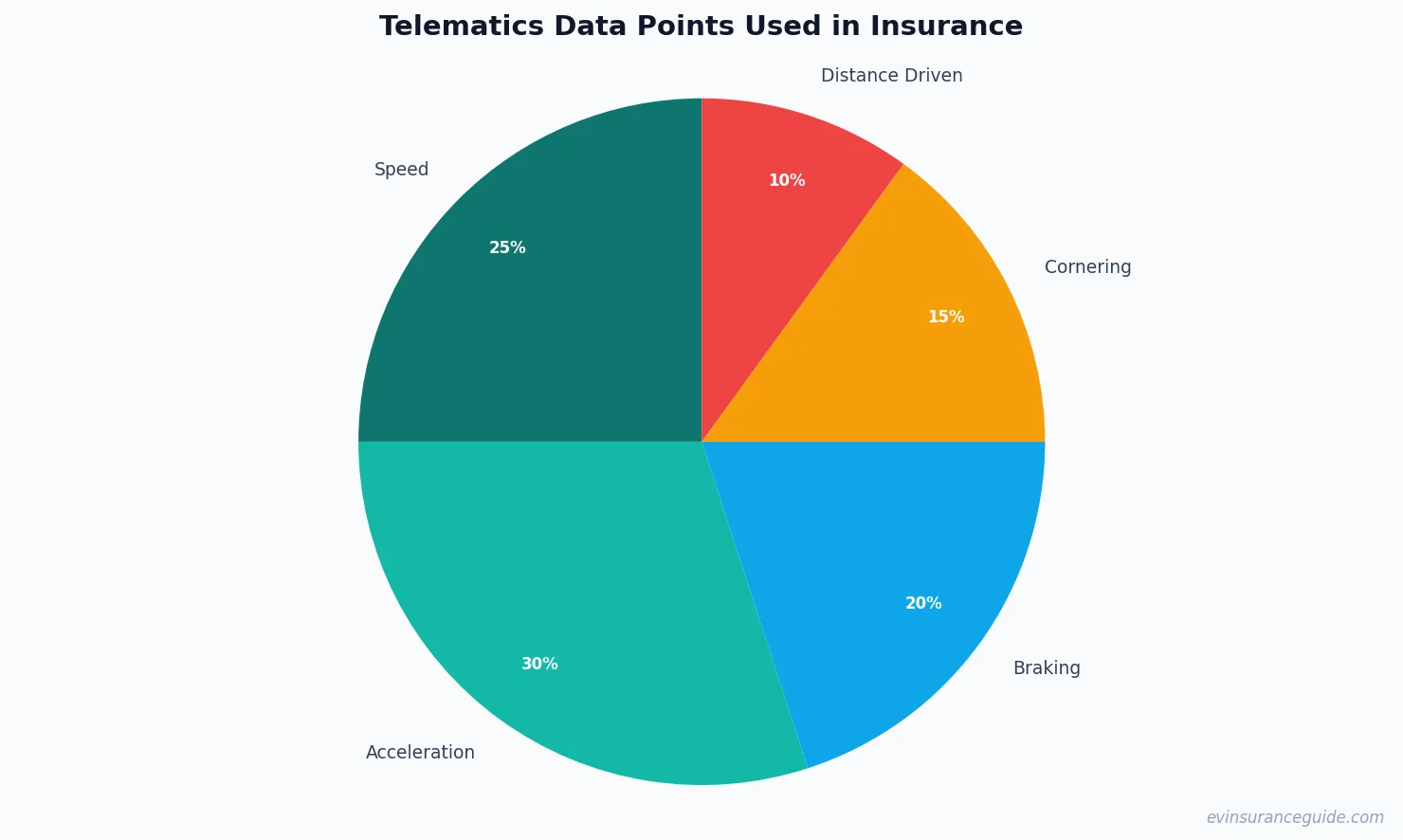

So, how does telematics data actually work? Well, it's pretty simple. Your car is equipped with a small device that tracks your driving habits, including your speed, acceleration, braking, and cornering. This data is then transmitted to the insurance company, which uses it to determine your premium. And the best part? You can usually access this data yourself, so you can see exactly how you're driving and where you can improve.

For example, let's say you're a Hyundai Ioniq 5 owner, and you're looking to save money on your insurance. You opt-in to the telematics program, and after a few months, you receive a report that shows you're a safe driver. You're eligible for a discount, and your premium goes down. But here's the thing: you can also use this data to improve your driving habits. Maybe you're acceleration is a bit too aggressive, or maybe you're braking too hard. With telematics data, you can identify these areas and work on improving them.

And the benefits don't stop there. Telematics data can also help you in the event of an accident. For instance, if you're involved in a crash, the data can be used to determine fault and process your claim more quickly. This can be a huge relief, especially if you're dealing with a complex claim. Sound familiar? It should — because it's exactly what happens when you're dealing with a traditional insurance claim, but without the hassle and paperwork.

HONEST_OPINION: Don't Overpay for EV Insurance

Look, I'm gonna be blunt: most EV owners are overpaying for their insurance. It's a fact. And it's not just because of the high cost of replacement parts or the limited number of insurance companies that offer EV-specific policies. It's because they're not taking advantage of telematics data. This is a game-changer, folks. With telematics data, you can save up to 30% on your premium, depending on your driving habits and the insurance company you choose.

But here's the thing: you gotta do your research. You can't just assume that every insurance company is offering telematics-based discounts. You gotta shop around, compare rates, and find the best deal for your specific situation. And don't be afraid to negotiate — because, let's be real, insurance companies are all about making a profit. So, if you can prove that you're a safe driver, they should be willing to give you a better rate.

For instance, let's say you're a Rivian owner, and you're looking for a new insurance policy. You do your research, and you find a company that offers telematics-based discounts. You opt-in to the program, and after a few months, you receive a report that shows you're a safe driver. You're eligible for a discount, and your premium goes down. But here's the thing: you can also use this data to improve your driving habits, and potentially save even more money in the long run.

If you're looking to save money on your EV insurance, don't be afraid to ask about telematics-based discounts. It's a simple way to save up to 30% on your premium, and it's only going to become more popular in the future.

5 Ways to Save Money on EV Insurance

So, how can you save money on your EV insurance? Here are five ways to get started:

- 1. Shop around and compare rates from different insurance companies.

- 2. Opt-in to telematics programs, which can offer personalized rates based on your driving habits.

- 3. Bundle your EV insurance with other policies, like home or renters insurance.

- 4. Improve your driving habits, such as accelerating and braking more smoothly.

- 5. Consider purchasing a car with advanced safety features, like lane departure warning or blind spot detection.

For example, let's say you're a 40-year-old driver with a clean record, and you own a Tesla Model Y. Your annual premium could range from $2,000 to $4,000, depending on the insurance company and the level of coverage you choose. But with telematics data, you could potentially save up to $1,000 per year. That's a significant chunk of change — and it's all because you're willing to share your driving data with the insurance company.

Can You Really Save Money on EV Insurance?

So, can you really save money on your EV insurance? The answer is yes — but it depends on your specific situation. If you're a safe driver with a clean record, you may be eligible for discounts. But if you're a high-risk driver, you may not qualify for the same level of savings. Know what the kicker is? It's all about being proactive and taking control of your insurance costs.

For instance, let's say you're a 30-year-old driver with a few speeding tickets on your record. Your annual premium could range from $2,500 to $5,000, depending on the insurance company and the level of coverage you choose. But with telematics data, you could potentially save up to $1,200 per year. That's a significant chunk of change — and it's all because you're willing to share your driving data with the insurance company.

FAQs

#### How do I opt-in to telematics programs?

To opt-in to telematics programs, you'll typically need to contact your insurance company and ask about their specific program. They'll usually send you a device to install in your car, which will track your driving habits and report back to the insurance company.

#### What kind of data is collected by telematics devices?

Telematics devices collect a range of data, including your speed, acceleration, braking, and cornering. This data is then used to determine your premium and offer personalized rates.

#### Can I use telematics data to improve my driving habits?

Yes, you can use telematics data to improve your driving habits. By tracking your driving data, you can identify areas where you need to improve, such as accelerating and braking more smoothly.

#### How much can I save with telematics-based discounts?

The amount you can save with telematics-based discounts varies depending on your insurance company and your driving habits. But on average, you can save up to 30% on your premium.

#### Are telematics programs available for all EV models?

No, telematics programs are not available for all EV models. However, many major insurance companies offer telematics-based discounts for popular EV models like the Tesla Model 3 and BMW iX.

#### Do I need to install a device in my car to participate in telematics programs?

Not always. Some insurance companies offer telematics programs that use the built-in technology in your car, such as the Tesla Model 3's Autopilot system. But in most cases, you'll need to install a device to participate in the program.

So, there you have it — the inside scoop on how to save money on your EV insurance with telematics data. It's not rocket science, folks. It's just about being proactive and taking control of your insurance costs. And if you're willing to share your driving data with the insurance company, you can potentially save up to 30% on your premium. That's a no-brainer, if you ask me. Happy driving, and don't overpay! — Alex