I was sipping on a coffee at a charging station, watching a few Nissan Leafs charge up, when I overheard a conversation between two owners. They were swapping stories about their insurance experiences, and one of them mentioned how they were paying over $400 a month for their Leaf. The other owner chimed in, saying they were paying around $280 for the same model. I couldn't help but wonder, what's the difference? Is it the driver's history, the insurance company, or something else entirely? Sound familiar?

COMPARISON — Electric Vehicles vs Gas Guzzlers: Which Ones Cost Less to Insure?

When it comes to insurance, electric vehicles like the Nissan Leaf, Tesla Model 3, and BMW iX are often compared to their gas-powered counterparts. But which ones actually cost less to insure? Well, according to a study by the National Association of Insurance Commissioners, EVs tend to be cheaper to insure, with an average annual premium of around $1,300, compared to $1,600 for gas-powered vehicles. That's a savings of around $300 per year. But, know what the kicker is? Some insurance companies, like Geico and Progressive, offer even lower rates for EV owners, with discounts ranging from 5% to 10% off their standard rates.

The Nissan Leaf, in particular, is a great example of an EV that can be insured at a lower rate. With its advanced safety features, like automatic emergency braking and lane departure warning, it's considered a lower-risk vehicle. And, with a starting price of around $30,000, it's an affordable option for many buyers. But, what about the insurance costs? Can you really save money on Nissan Leaf insurance? Absolutely, and I'll show you how.

How to Save on Nissan Leaf Insurance: Can You Really Lower Your Premiums?

So, you wanna know how to save on Nissan Leaf insurance? Well, the first step is to shop around. Don't just go with the first insurance company you find; compare rates from multiple providers to find the best deal. For example, a friend of mine, let's call him Alex, was paying around $380 per month for his Leaf. He decided to shop around and found a better rate with USAA, which lowered his premium to around $260 per month. That's a savings of around $120 per month, or $1,440 per year. Wild, right?

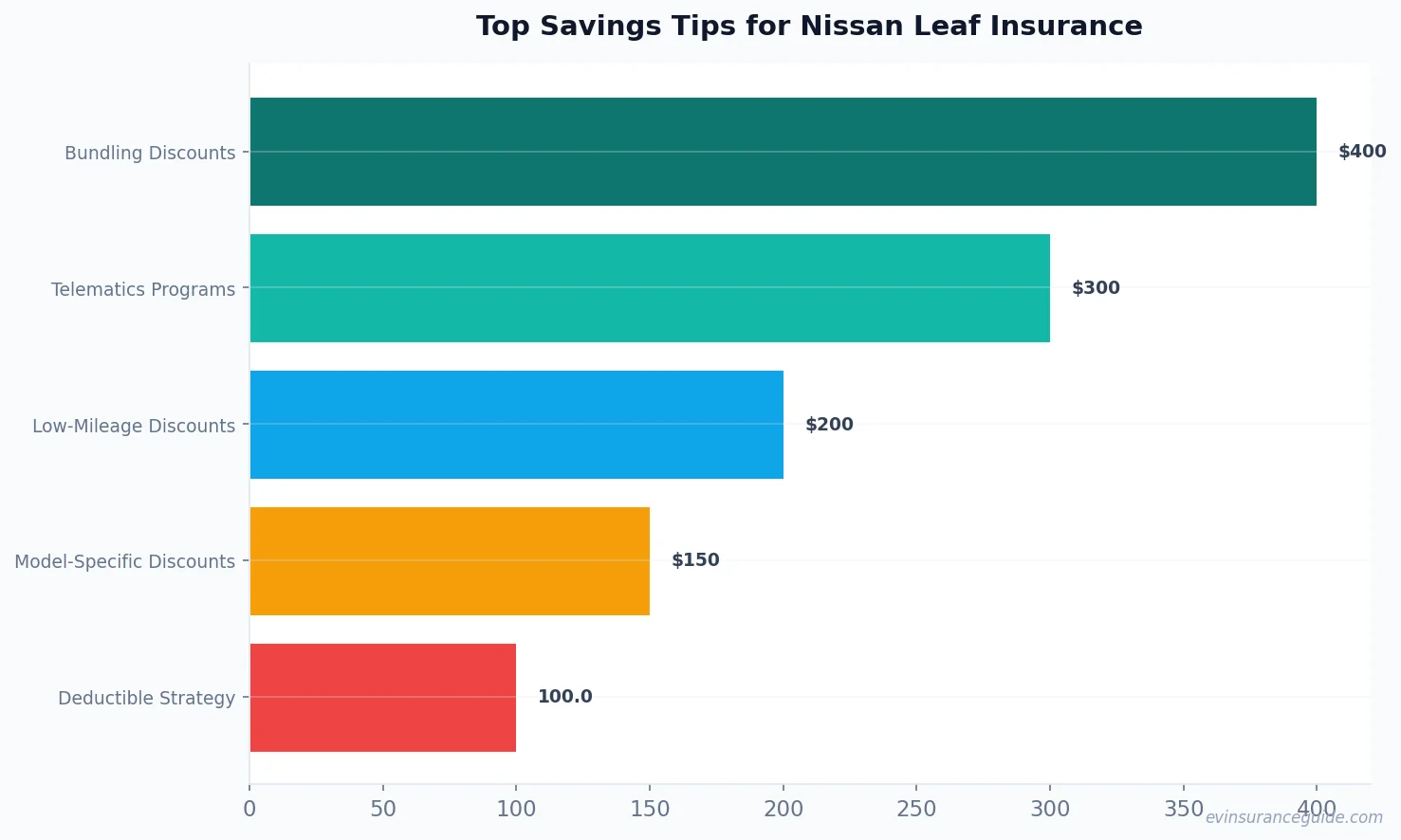

But, that's not all. Another way to save on Nissan Leaf insurance is to take advantage of bundling discounts. If you have multiple vehicles or a home, you can bundle your policies with one insurance company and get a discount. For example, State Farm offers a discount of up to 20% off your auto insurance premiums when you bundle with a home policy. And, with a Nissan Leaf, you can also get a discount for being a low-mileage driver. Some insurance companies, like Allstate, offer a discount of up to 10% off your premiums if you drive less than 7,500 miles per year.

OK So Here's the Deal With Telematics Programs...

OK, so here's the deal with telematics programs: they can be a great way to save money on your Nissan Leaf insurance. These programs use a device or app to track your driving habits and provide feedback on how to improve your driving. Some insurance companies, like Progressive, offer a discount of up to 20% off your premiums if you participate in their telematics program. And, with a Nissan Leaf, you can also take advantage of its advanced safety features, like adaptive cruise control and lane centering, to get a discount.

But, which telematics program is the best? Well, that depends on your driving habits and the insurance company you choose. Some popular telematics programs include Progressive's Snapshot, State Farm's Drive Safe & Save, and Geico's DriveEasy. Each program has its own set of features and discounts, so it's worth shopping around to find the one that works best for you.

WARNING — Don't Get Caught in the High-Deductible Trap...

Don't get caught in the high-deductible trap, where you think you're saving money on your premiums, but end up paying more out of pocket when you file a claim. It's a common mistake, and one that can cost you big time. For example, let's say you have a $2,000 deductible on your Nissan Leaf insurance policy. If you get into an accident and the repair costs are $3,000, you'll have to pay the first $2,000 out of pocket, and then the insurance company will cover the remaining $1,000. But, if you have a lower deductible, say $500, you'll only have to pay $500 out of pocket, and the insurance company will cover the remaining $2,500.

So, what's the optimal deductible strategy? Well, it depends on your financial situation and driving habits. If you're a low-mileage driver and have a good driving record, you may be able to get away with a higher deductible. But, if you're a high-mileage driver or have a history of accidents, it's best to stick with a lower deductible.

STORY TEASE — The Time I Saved $800 on My EV Insurance...

I've got a story to tell, and it's one that'll make you laugh. So, I was shopping around for insurance for my friend's Hyundai Ioniq 5, and I stumbled upon a company that offered a discount for EV owners. I thought, why not, and decided to give it a try. Long story short, I ended up saving around $800 per year on the insurance premiums. It was a no-brainer, and I was glad I made the switch. But, the real kicker was when I realized that I could've saved even more if I had shopped around earlier. Don't make the same mistake, folks. Shop around, and you'll be surprised at how much you can save.

FAQs

#### What is the average cost of Nissan Leaf insurance?

The average cost of Nissan Leaf insurance varies depending on several factors, including your location, driving history, and insurance company. However, according to a study by NerdWallet, the average annual premium for a Nissan Leaf is around $1,300.

#### How can I get a discount on my Nissan Leaf insurance?

There are several ways to get a discount on your Nissan Leaf insurance, including bundling your policies, taking advantage of telematics programs, and being a low-mileage driver. Some insurance companies, like Geico and Progressive, also offer discounts for EV owners.

#### What is the best insurance company for Nissan Leaf owners?

The best insurance company for Nissan Leaf owners depends on several factors, including your location, driving history, and budget. However, some popular insurance companies for EV owners include Geico, Progressive, and USAA.

#### Can I get a discount for being a low-mileage driver?

Yes, many insurance companies offer discounts for low-mileage drivers. For example, State Farm offers a discount of up to 10% off your premiums if you drive less than 7,500 miles per year.

#### How can I save money on my Nissan Leaf insurance premiums?

There are several ways to save money on your Nissan Leaf insurance premiums, including shopping around, bundling your policies, and taking advantage of telematics programs. You can also consider raising your deductible, but be careful not to get caught in the high-deductible trap.

#### What are some model-specific discounts for the Nissan Leaf?

Some insurance companies offer model-specific discounts for the Nissan Leaf, including discounts for its advanced safety features and low emissions. For example, Geico offers a discount of up to 10% off your premiums for EV owners.

#### Are there any federal or state incentives for EV owners?

Yes, there are several federal and state incentives for EV owners, including tax credits and rebates. For example, the federal government offers a tax credit of up to $7,500 for EV owners, and some states offer rebates of up to $5,000.

As a seasoned EV owner, I can tell you that shopping around for insurance is key. Don't just go with the first company you find; compare rates and find the best deal. And, don't be afraid to negotiate – it's worth it in the long run.

So, there you have it – 10 tips to help you save money on your Nissan Leaf insurance. From shopping around to taking advantage of telematics programs, there are plenty of ways to lower your premiums and get the best coverage for your EV. And, remember, it's all about finding the right balance between cost and coverage. You don't want to sacrifice one for the other, or you'll end up paying more in the long run. Happy driving, and don't overpay! — Alex