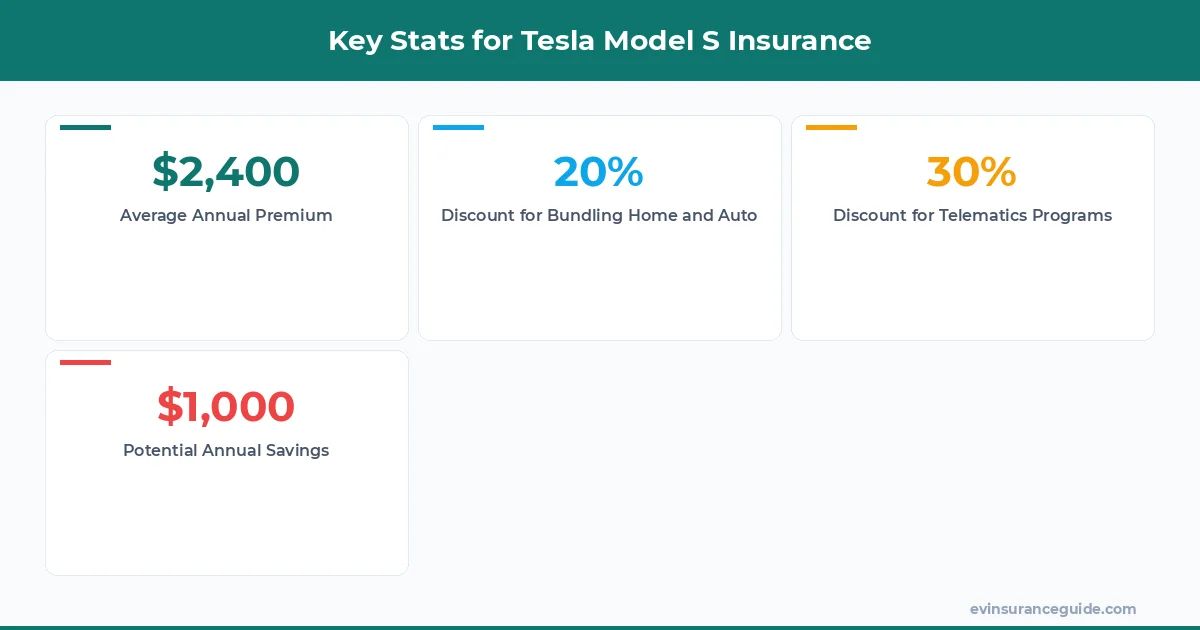

Did you know that the average annual premium for a Tesla Model S is around $2,400? That's a pretty penny, especially considering the already steep price tag of the vehicle itself. But what if I told you that with the right strategies, you could save upwards of $1,000 per year on your Tesla Model S insurance? Sound familiar? You're probably thinking, "Yeah, I've heard that before, but how do I actually do it?"

How to Save on Tesla Model S Insurance?

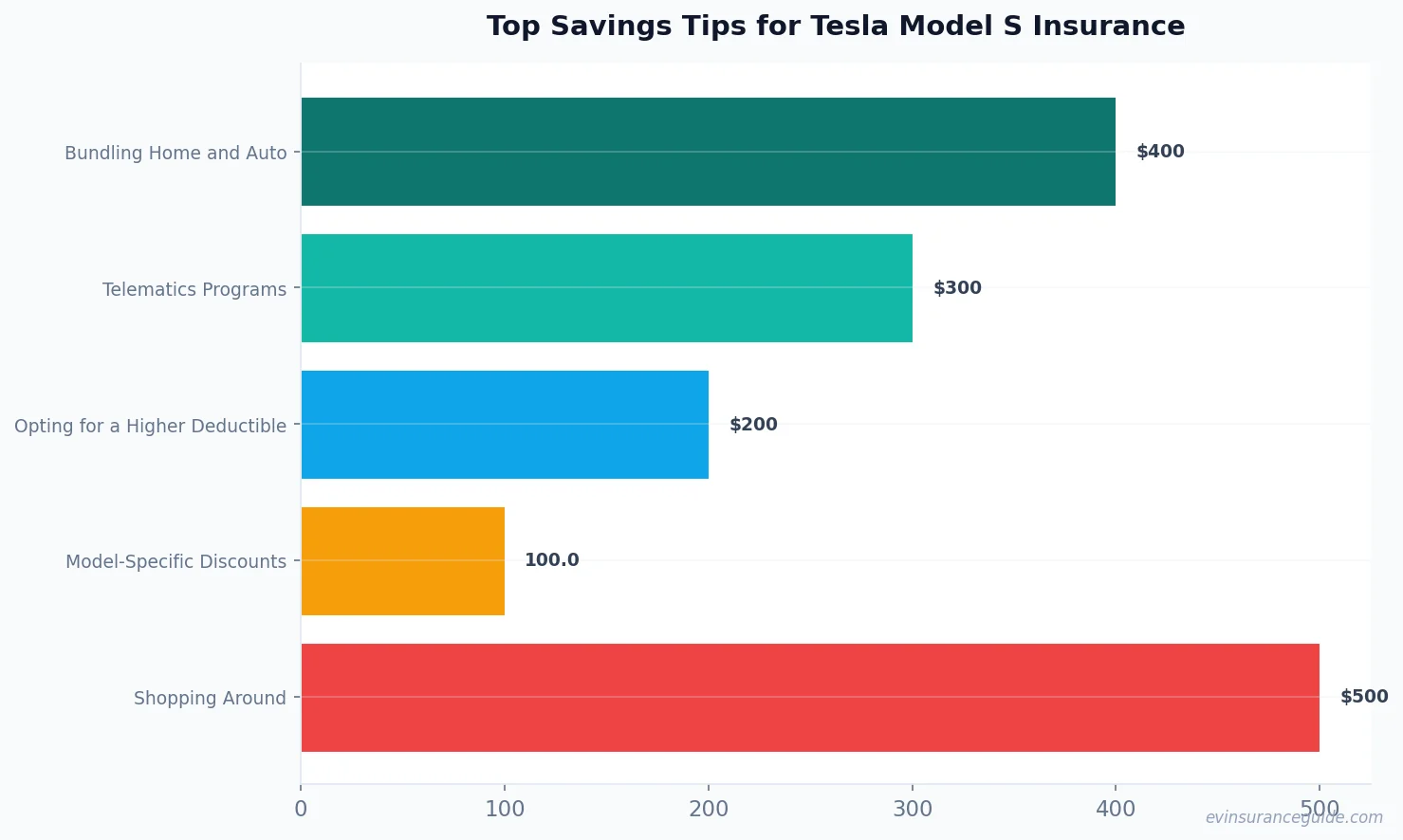

Well, actually, it's not as complicated as you might think. One of the easiest ways to save on Tesla Model S insurance is by bundling your home and auto policies. For example, if you're currently paying $380 per month for your Tesla Model S insurance, you could potentially save around $400-600 per year by bundling your policies with a company like State Farm or Allstate. That's a significant chunk of change, if you ask me. Know what the kicker is? You can often get even better rates if you have a good driving record and a high credit score. So, if you're a responsible driver with a solid credit history, you could be looking at some serious savings.

But, let's get real for a second. Bundling isn't the only way to save on Tesla Model S insurance. You could also consider opting for a higher deductible, which would lower your monthly premiums. For instance, if you currently have a $500 deductible, you could potentially save around $200-300 per year by increasing it to $1,000. Of course, this means you'll have to pay more out of pocket in the event of an accident, but if you're a safe driver, it could be a smart move. Dead serious, it's all about weighing the risks and benefits.

And, if you're feeling extra adventurous, you could even look into telematics programs, which track your driving habits and reward you with lower rates if you're a safe driver. For example, Progressive's Snapshot program uses a small device to monitor your driving and can potentially save you up to 30% on your premiums. That's a pretty sweet deal, if you ask me. Wild, right? The future of insurance is all about data-driven decision making, and if you're willing to share your driving data, you could be looking at some serious savings.

OK So Here's the Deal With Telematics Programs

OK, so you're probably wondering how these telematics programs work, and which ones are the best for Tesla Model S owners. Well, let me tell you, it's not as complicated as it sounds. Most telematics programs use a small device that plugs into your car's OBD-II port and tracks your driving habits, such as speed, acceleration, and braking. The data is then sent to the insurance company, which uses it to determine your rates. For example, if you're a safe driver who always wears your seatbelt and never speeds, you'll likely qualify for lower rates. On the other hand, if you're a bit of a lead foot, you might not see as much savings. Hmm, let me rethink that... actually, it's not just about being a safe driver, it's also about being a consistent driver. So, if you're someone who always drives at the same time of day, on the same roads, you'll likely see more savings than someone who drives all over the place.

But, what about the different types of telematics programs out there? Well, some companies, like Liberty Mutual, offer a mobile app that you can download and use to track your driving. Others, like Allstate, use a small device that plugs into your car's OBD-II port. And then there are companies, like Root Insurance, that use a combination of both. So, which one is best for you? Well, that depends on your personal preferences and driving habits. If you're someone who likes to have control over your data, you might prefer a mobile app. On the other hand, if you're someone who doesn't want to have to think about it, you might prefer a plug-in device.

Busting the Myth That Tesla Model S Insurance is Always Expensive

So, you've probably heard that Tesla Model S insurance is always expensive, but is that really true? Nope. While it's true that Tesla Model S insurance can be pricey, there are plenty of ways to save money. For example, if you're a member of the military, you might qualify for a discount with companies like USAA. Or, if you're a student with good grades, you might qualify for a discount with companies like Geico. And, if you're a safe driver with a clean record, you might qualify for a discount with companies like Progressive. That one stung, didn't it? I mean, who doesn't love saving money?

But, what about model-specific discounts? Well, some companies, like Tesla Insurance, offer discounts specifically for Tesla owners. For example, if you're a Tesla Model S owner, you might qualify for a discount of up to 10% on your premiums. And, if you're a Tesla Model 3 or Model Y owner, you might qualify for an even bigger discount. So, which models qualify for the biggest discounts? Well, that depends on the company and the specific model. But, as a general rule, the more expensive the model, the bigger the discount.

Comparing Tesla Model S Insurance Rates to Other EVs

So, how do Tesla Model S insurance rates compare to other EVs on the market? Well, let's take a look at some numbers. For example, the average annual premium for a BMW iX is around $2,100, while the average annual premium for a Hyundai Ioniq 5 is around $1,800. And, if you're looking at the Rivian R1T, you're looking at an average annual premium of around $2,500. But, what about the Tesla Model 3? Well, the average annual premium for a Tesla Model 3 is around $1,900, while the average annual premium for a Tesla Model Y is around $2,000. So, which EV has the lowest insurance rates? Well, that would be the Hyundai Ioniq 5, followed closely by the Tesla Model 3.

But, what about the factors that affect insurance rates? Well, some of the biggest factors include the make and model of the vehicle, the driver's age and experience, and the location where the vehicle is driven. For example, if you live in a big city, you're likely to pay more for insurance than if you live in a small town. And, if you're a young driver, you're likely to pay more for insurance than if you're an older driver. So, how can you save money on insurance? Well, one way is to shop around and compare rates from different companies. Another way is to consider opting for a higher deductible, which would lower your monthly premiums.

Being Honest About the Best Way to Save on Tesla Model S Insurance

So, what's the best way to save on Tesla Model S insurance? Well, honestly, it's all about finding the right combination of discounts and rates that work for you. For example, if you're a safe driver with a clean record, you might qualify for a discount with companies like Progressive. And, if you're a member of the military, you might qualify for a discount with companies like USAA. But, what about bundling your home and auto policies? Well, that's a great way to save money, especially if you have a good driving record and a high credit score. So, which company offers the best bundling discounts? Well, that depends on your specific situation, but some companies, like State Farm, offer discounts of up to 20% for bundling your home and auto policies.

But, what about the pros and cons of each company? Well, some companies, like Geico, offer great rates but not as many discounts. Others, like Allstate, offer a wide range of discounts but not the best rates. So, which company is best for you? Well, that depends on your specific situation and what you're looking for in an insurance company. But, one thing is for sure: shopping around and comparing rates is the best way to save money on Tesla Model S insurance.

FAQs

#### What is the average annual premium for a Tesla Model S?

The average annual premium for a Tesla Model S is around $2,400. But, this can vary depending on a number of factors, including the driver's age and experience, the location where the vehicle is driven, and the make and model of the vehicle.

#### How can I save money on Tesla Model S insurance?

There are a number of ways to save money on Tesla Model S insurance, including bundling your home and auto policies, opting for a higher deductible, and shopping around to compare rates from different companies.

#### What is the best way to compare insurance rates?

The best way to compare insurance rates is to shop around and get quotes from multiple companies. You can do this online or by working with an insurance agent. It's also a good idea to read reviews and check the financial stability of the companies you're considering.

#### Can I get a discount for being a safe driver?

Yes, many insurance companies offer discounts for safe drivers. For example, Progressive's Snapshot program uses a small device to monitor your driving and can potentially save you up to 30% on your premiums.

#### How much can I save by bundling my home and auto policies?

The amount you can save by bundling your home and auto policies varies depending on the company and your specific situation. But, some companies, like State Farm, offer discounts of up to 20% for bundling your home and auto policies.

#### What is the difference between a $500 deductible and a $1,000 deductible?

The main difference between a $500 deductible and a $1,000 deductible is the amount you'll have to pay out of pocket in the event of an accident. With a $500 deductible, you'll pay $500, while with a $1,000 deductible, you'll pay $1,000. But, a higher deductible can also mean lower monthly premiums.

#### Can I get a discount for being a member of the military?

Yes, some insurance companies, like USAA, offer discounts for members of the military. These discounts can vary depending on the company and your specific situation.

Pro tip: Always shop around and compare rates from multiple companies to find the best deal on Tesla Model S insurance.

So, let's say you're a Tesla Model S owner who's currently paying $380 per month for insurance. By bundling your home and auto policies, opting for a higher deductible, and shopping around to compare rates, you could potentially save around $120 per month, or $1,440 per year. That's a significant chunk of change, if you ask me. But, it's not just about the money - it's also about finding the right insurance company and policy for your specific needs. So, do your research, shop around, and don't be afraid to negotiate. That's my two cents. Take it or leave it — but I hope it helps. — Alex