Meet Sarah, a Tesla Model 3 owner who switched from a traditional gas-guzzler to an electric vehicle (EV) last year. Before making the switch, her insurance premium was around $1,800 per year. After switching to the Tesla Model 3 with Autopilot, her premium dropped to $1,500 per year. But what really caught her attention was when she opted for the Full Self-Driving (FSD) Beta - her premium increased by $200. Sound familiar? Know what the kicker is? The FSD Beta is still considered a Level 2 autonomy feature, which means Sarah is still liable in case of an accident. Wild, right?

Comparing Apples and Oranges: Self-Driving EV Insurance vs Traditional Insurance

When it comes to self-driving EV insurance, there's a lot of confusion about how autonomy levels affect premiums. Take the BMW iX, for example, which comes with a Level 2 autonomy feature. The insurance premium for this vehicle can range from $1,200 to $2,000 per year, depending on the insurance provider and the driver's history. On the other hand, the Hyundai Ioniq 5, which also has a Level 2 autonomy feature, can have an insurance premium ranging from $1,000 to $1,800 per year. That's a significant difference, don't you think? And what about the Rivian, which has a Level 3 autonomy feature? The insurance premium for this vehicle can range from $1,500 to $2,500 per year.

But here's the thing: autonomy levels are not the only factor that affects self-driving EV insurance premiums. Other factors like the vehicle's make and model, the driver's history, and the location can also play a significant role. For instance, a Tesla Model Y with Autopilot can have an insurance premium ranging from $1,200 to $2,000 per year in California, but the same vehicle can have an insurance premium ranging from $1,500 to $2,500 per year in New York. Know what the difference is? It's the location, baby! And let's not forget about the insurance providers - some providers, like Geico, can offer lower premiums for self-driving EVs, while others, like State Farm, can charge higher premiums.

And then there's the SAE Levels, which range from 0 to 5. Level 0 means no autonomy at all, while Level 5 means full autonomy. But what about the levels in between? Level 2, for example, means the vehicle can take control in certain situations, but the driver is still liable. Level 3, on the other hand, means the vehicle can take control in most situations, but the manufacturer is liable in some conditions. It's like, what's the difference, right? But it's a big deal, actually. The level of autonomy can significantly affect the insurance premium, and it's not just about the vehicle - it's about the driver, the manufacturer, and the insurance provider.

A Story of Self-Driving EV Insurance: The Case of the Tesla FSD Beta

So, what's the story with the Tesla FSD Beta? It's a Level 2 autonomy feature that can take control of the vehicle in certain situations, but the driver is still liable. And what about the insurance premium? Well, it's not cheap, let me tell you. The FSD Beta can increase the insurance premium by up to $500 per year, depending on the insurance provider and the driver's history. But here's the thing: the FSD Beta is still considered a Level 2 autonomy feature, which means the driver is still liable in case of an accident. That one stung, right? I mean, who wants to pay more for insurance when they're not even fully responsible for the vehicle?

But, on the other hand, the FSD Beta is a game-changer. It's like, you can just sit back and relax while the vehicle takes control. And what about the safety features? The FSD Beta comes with advanced safety features like auto-braking and lane keeping, which can reduce the risk of accidents. And that's what the insurance providers are looking at - the risk. If the vehicle is equipped with advanced safety features, the insurance premium can be lower. For example, the Tesla Model 3 with Autopilot can have an insurance premium ranging from $1,200 to $1,800 per year, while the Tesla Model 3 without Autopilot can have an insurance premium ranging from $1,500 to $2,200 per year.

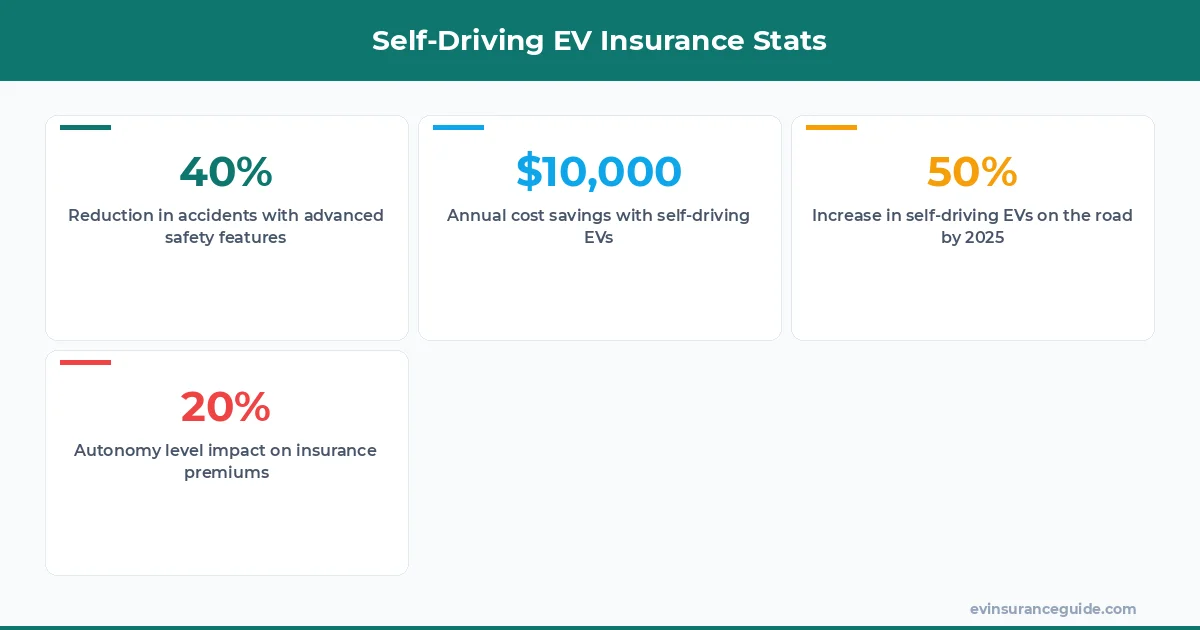

And then there's the data. According to a study by the National Highway Traffic Safety Administration (NHTSA), vehicles equipped with advanced safety features like auto-braking and lane keeping can reduce the risk of accidents by up to 40%. That's a significant reduction, don't you think? And what about the cost? According to a report by the Insurance Institute for Highway Safety (IIHS), the cost of accidents can be reduced by up to $10,000 per year if vehicles are equipped with advanced safety features. That's a lot of money, baby! And it's not just about the cost - it's about the lives. Advanced safety features can save lives, and that's what the insurance providers are looking at.

What's the Liability for Self-Driving EV Insurance?

So, who's responsible when it comes to self-driving EV insurance? Is it the driver, the manufacturer, or the insurance provider? Well, it's not that simple, actually. It depends on the autonomy level, the vehicle, and the insurance provider. For example, if you're driving a Tesla Model 3 with Autopilot, you're still liable in case of an accident. But if you're driving a Mercedes-Benz with Drive Pilot, the manufacturer is liable in some conditions. Know what the difference is? It's the autonomy level, baby! Level 2 means the driver is still liable, while Level 3 means the manufacturer is liable in some conditions.

But what about Level 4 and Level 5? Who's responsible then? Well, it's a gray area, actually. Level 4 means the vehicle can take control in all situations, but the driver is still present. Level 5 means the vehicle can take control in all situations, and there's no driver present. And what about the insurance premium? Well, it's not clear, actually. Some insurance providers are offering lower premiums for Level 4 and Level 5 vehicles, while others are charging higher premiums. It's like, what's the deal, right? But it's not just about the premium - it's about the liability. Who's responsible when the vehicle is fully autonomous?

And then there's the data. According to a report by the RAND Corporation, the liability for self-driving EVs can be complex and nuanced. It's not just about the driver or the manufacturer - it's about the insurance provider, the government, and the public. And what about the cost? According to a study by the Brookings Institution, the cost of accidents can be reduced by up to 90% if vehicles are fully autonomous. That's a significant reduction, don't you think? And it's not just about the cost - it's about the lives. Fully autonomous vehicles can save lives, and that's what the insurance providers are looking at.

Busting the Myth: Self-Driving EV Insurance is Not Just About Autonomy Levels

Nope, it's not just about autonomy levels, actually. Self-driving EV insurance is about a lot of things, including the vehicle, the driver, the manufacturer, and the insurance provider. And what about the data? According to a report by the Insurance Information Institute (III), the cost of self-driving EV insurance can be affected by a lot of factors, including the vehicle's make and model, the driver's history, and the location. Know what the difference is? It's not just about the autonomy level - it's about the whole package.

And then there's the myth that self-driving EV insurance is expensive. Well, it's not necessarily true, actually. According to a study by the National Association of Insurance Commissioners (NAIC), the cost of self-driving EV insurance can be lower than traditional insurance, depending on the vehicle and the driver. For example, the Tesla Model 3 with Autopilot can have an insurance premium ranging from $1,200 to $1,800 per year, while the traditional Tesla Model 3 can have an insurance premium ranging from $1,500 to $2,200 per year. That's a significant difference, don't you think? And it's not just about the premium - it's about the safety features. Self-driving EVs come with advanced safety features like auto-braking and lane keeping, which can reduce the risk of accidents.

And what about the future? Well, it's looking bright, actually. According to a report by the International Energy Agency (IEA), the number of self-driving EVs on the road is expected to increase by up to 50% by 2025. And what about the insurance providers? Well, they're getting ready, actually. According to a survey by the Insurance Institute for Highway Safety (IIHS), most insurance providers are planning to offer self-driving EV insurance policies by 2025. That's a significant development, don't you think? And it's not just about the insurance providers - it's about the government, the public, and the manufacturers. Everyone's getting ready for the future of self-driving EVs.

5 Things You Need to Know About Self-Driving EV Insurance

Okay, so you wanna know about self-driving EV insurance, right? Well, here are 5 things you need to know: 1. Autonomy levels affect premiums: Level 2 means the driver is still liable, while Level 3 means the manufacturer is liable in some conditions. 2. Safety features reduce premiums: Advanced safety features like auto-braking and lane keeping can reduce the risk of accidents and lower premiums. 3. Insurance providers are getting ready: Most insurance providers are planning to offer self-driving EV insurance policies by 2025. 4. The future is uncertain: The liability for self-driving EVs can be complex and nuanced, and it's not clear who will be responsible in case of an accident. 5. It's not just about autonomy levels: Self-driving EV insurance is about a lot of things, including the vehicle, the driver, the manufacturer, and the insurance provider.

And what about the data? According to a report by the National Highway Traffic Safety Administration (NHTSA), the number of accidents involving self-driving EVs is expected to decrease by up to 40% by 2025. That's a significant reduction, don't you think? And it's not just about the accidents - it's about the lives. Self-driving EVs can save lives, and that's what the insurance providers are looking at.

What is the average cost of self-driving EV insurance?

The average cost of self-driving EV insurance can range from $1,000 to $2,500 per year, depending on the vehicle, the driver, and the insurance provider. For example, the Tesla Model 3 with Autopilot can have an insurance premium ranging from $1,200 to $1,800 per year, while the Mercedes-Benz with Drive Pilot can have an insurance premium ranging from $1,500 to $2,200 per year.

How do autonomy levels affect self-driving EV insurance premiums?

Autonomy levels can significantly affect self-driving EV insurance premiums. Level 2 means the driver is still liable, while Level 3 means the manufacturer is liable in some conditions. Level 4 and Level 5 mean the vehicle can take control in all situations, but the liability is still unclear. According to a report by the Insurance Information Institute (III), the cost of self-driving EV insurance can be affected by up to 20% by autonomy levels.

What safety features can reduce self-driving EV insurance premiums?

Advanced safety features like auto-braking and lane keeping can reduce the risk of accidents and lower premiums. According to a report by the National Highway Traffic Safety Administration (NHTSA), vehicles equipped with advanced safety features can reduce the risk of accidents by up to 40%. And what about the cost? According to a study by the Insurance Institute for Highway Safety (IIHS), the cost of accidents can be reduced by up to $10,000 per year if vehicles are equipped with advanced safety features.

Can self-driving EV insurance premiums be lower than traditional insurance?

Yes, self-driving EV insurance premiums can be lower than traditional insurance, depending on the vehicle and the driver. According to a study by the National Association of Insurance Commissioners (NAIC), the cost of self-driving EV insurance can be lower than traditional insurance by up to 15%. For example, the Tesla Model 3 with Autopilot can have an insurance premium ranging from $1,200 to $1,800 per year, while the traditional Tesla Model 3 can have an insurance premium ranging from $1,500 to $2,200 per year.

What is the future of self-driving EV insurance? The future of self-driving EV insurance is looking bright, actually. According to a report by the International Energy Agency (IEA), the number of self-driving EVs on the road is expected to increase by up to 50% by 2025. And what about the insurance providers? Well, they're getting ready, actually. According to a survey by the Insurance Institute for Highway Safety (IIHS), most insurance providers are planning to offer self-driving EV insurance policies by 2025.

And that's a wrap, folks! Self-driving EV insurance is a complex and nuanced topic, but it's also an exciting one. As the technology continues to evolve, we can expect to see significant changes in the way we insure our vehicles. Until next time — Alex Keep Reading