OK so someone DM'd me this question... what's the deal with self-driving EV insurance? I mean, we've got Level 2, Level 3, Level 4, and Level 5 autonomy — how does that affect your premium? Sound familiar? You're not alone. I've been digging into this for months, and let me tell you, it's a wild ride.

1

2026 is shaping up to be a big year for electric vehicles, with more models than ever hitting the market — like the Hyundai Ioniq 5 and Rivian R1T. But with all these new EVs comes a new level of complexity when it comes to insurance. I'm talking about self-driving EV insurance, specifically how autonomy levels impact your rates. You see, the Society of Automotive Engineers (SAE) has defined 6 levels of autonomy, from Level 0 (no automation) to Level 5 (full automation). And let me tell you, the difference between Level 2 and Level 3 is huge. Level 2, used in systems like Tesla Autopilot and GM Super Cruise, still requires a human driver to be attentive and ready to take control at all times. That means if something goes wrong, the driver is still liable. Know what the kicker is? Level 3, used in systems like Mercedes Drive Pilot, starts to shift some of that liability to the manufacturer — but only in certain conditions.

For example, if you're driving a Mercedes with Drive Pilot engaged and it gets into an accident, the manufacturer might be on the hook for damages — but only if the system was functioning properly and the driver was using it as intended. That one stung, right? I mean, who's responsible when a self-driving car crashes? It's a question that's gonna get a lot more complicated as we move towards higher levels of autonomy.

And don't even get me started on Level 4 and Level 5. I mean, at those levels, the car is essentially driving itself — no human input required. But who's responsible when something goes wrong? The manufacturer? The software developer? The owner of the car? It's a mess, and it's gonna take some serious regulation to sort it out.

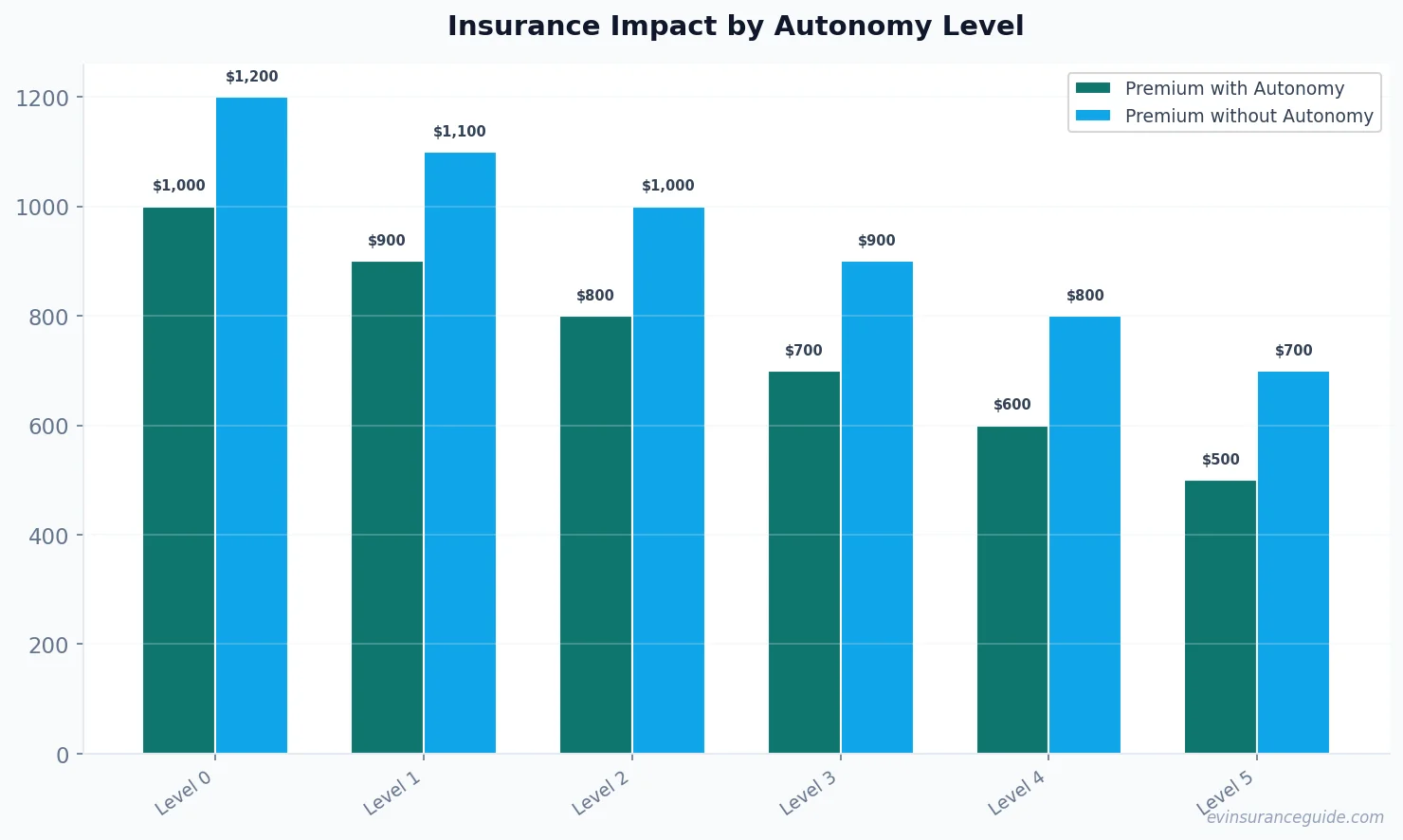

What happens to my self driving EV insurance premium when I use Level 2 autonomy?

So, what does all this mean for your self driving EV insurance premium? Well, it's complicated. If you're using a Level 2 system like Tesla Autopilot, your rates might actually go down — but not by much. I'd estimate a 2-5% discount, depending on your insurer and the specific system you're using. But if you're using a Level 3 system like Mercedes Drive Pilot, that's where things get interesting. Because the manufacturer is taking on some of the liability, your rates might actually go down more — maybe 10-15% — because the insurer is shouldering less risk.

But here's the thing: these discounts are gonna vary wildly depending on the insurer, the specific vehicle, and the level of autonomy. And let's not forget about all the other factors that go into determining your premium — like your driving history, location, and deductible. It's a complex equation, and it's gonna take some time to sort out.

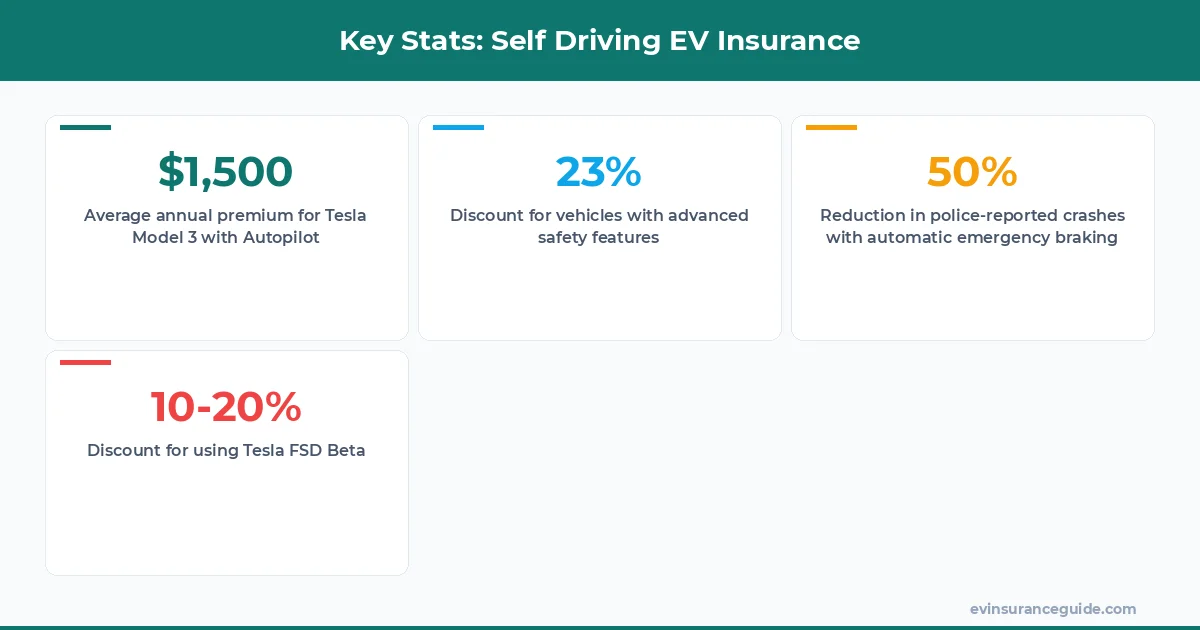

For instance, if you're driving a Tesla Model 3 with Autopilot engaged, your premium might be around $1,500 per year. But if you're driving a Mercedes with Drive Pilot, that premium might drop to $1,200 per year — assuming all other factors are equal. That's a $300 difference, just because of the autonomy level. Wild, right?

Pro tip: if you're shopping for self driving EV insurance, make sure to ask about autonomy-related discounts. Some insurers, like State Farm, are already offering discounts for vehicles with advanced safety features like auto-braking and lane keeping.

Cars with advanced safety features vs classic gas guzzlers

Now, let's compare cars with advanced safety features — like the BMW iX, with its suite of ADAS features — to classic gas guzzlers. I mean, it's no contest, right? The iX is a $100,000 vehicle with some of the most advanced safety features on the market, while a classic gas guzzler might be a $5,000 beater with no safety features to speak of. But here's the thing: even with all those advanced safety features, the iX is still gonna be more expensive to insure — at least, for now.

That's because insurers are still trying to figure out how to price the risk of these new vehicles. I mean, they're essentially flying blind, because there just isn't enough data yet. But as more and more people start driving EVs with advanced safety features, that's gonna change. Insurers are gonna start to see the benefits of these features — like reduced claims frequency and severity — and they're gonna start to price that into the premium.

For example, a study by the Insurance Institute for Highway Safety found that vehicles with automatic emergency braking had 50% fewer police-reported crashes than those without. That's a huge reduction in risk, and it's gonna translate into lower premiums over time.

Warning: don't assume self driving EV insurance is always cheaper

OK, so you might be thinking — self driving EV insurance is gonna be cheaper, right? I mean, these cars are basically driving themselves, so there's less risk of an accident. But hold on just a minute. That's not necessarily true. I mean, sure, autonomy can reduce the risk of an accident, but it's not a guarantee. And if something does go wrong, the liability issues can get really complicated, really fast.

For instance, let's say you're driving a Tesla with Autopilot engaged and it gets into an accident. You might assume that Tesla is on the hook for damages, but that's not necessarily true. I mean, if you were using the system as intended and it malfunctioned, then yeah, Tesla might be liable. But if you were using it in a way that's not recommended — like, say, you had your hands off the wheel for an extended period — then you might still be on the hook for damages.

It's a mess, and it's gonna take some serious regulation to sort it out. But in the meantime, don't assume that self driving EV insurance is always cheaper. I mean, it might be — but it depends on a lot of factors, like the level of autonomy, the specific vehicle, and the insurer.

Honest opinion: Tesla FSD Beta is a game-changer for self driving EV insurance

I'm gonna give you my honest opinion here: Tesla FSD Beta is a game-changer for self driving EV insurance. I mean, this is a system that's essentially capable of full autonomy — Level 5, in other words. And it's being rolled out to thousands of vehicles right now. But here's the thing: it's still in beta, and it's not perfect. I mean, there have been reports of glitches and malfunctions, and some people are even questioning whether it's safe to use on public roads.

But despite all that, I think FSD Beta is a step in the right direction. I mean, it's pushing the boundaries of what's possible with autonomy, and it's gonna force insurers to rethink their approach to self driving EV insurance. And let's be real — if you're using FSD Beta, you're probably gonna see a discount on your premium. I'd estimate 10-20%, depending on the insurer and the specific vehicle.

But here's the thing: using FSD Beta might also increase your premium in some cases. I mean, if you're using it in a way that's not recommended — like, say, you're taking your hands off the wheel for an extended period — then you might be seen as a higher risk by the insurer. And that could translate into higher premiums over time.

What is the current state of self driving EV insurance in 2026?

The current state of self driving EV insurance in 2026 is complex and evolving. I mean, we've got multiple autonomy levels, each with its own set of risks and benefits. And insurers are still trying to figure out how to price that risk. But one thing is for sure: self driving EV insurance is gonna be a major growth area in the next few years.

How do I get a discount on my self driving EV insurance premium?

To get a discount on your self driving EV insurance premium, you'll wanna ask about autonomy-related discounts. Some insurers, like State Farm, are already offering discounts for vehicles with advanced safety features like auto-braking and lane keeping. And if you're using a Level 3 system like Mercedes Drive Pilot, you might see an even bigger discount — maybe 10-15%.

What are the most important factors in determining my self driving EV insurance premium?

The most important factors in determining your self driving EV insurance premium are gonna be the level of autonomy, the specific vehicle, and your driving history. I mean, if you're a safe driver with a clean record, you're gonna see lower premiums — regardless of the autonomy level. But if you're a high-risk driver, you might see higher premiums, even with advanced safety features.

Can I use Tesla FSD Beta and still get a discount on my self driving EV insurance premium?

Yes, you can use Tesla FSD Beta and still get a discount on your self driving EV insurance premium. I'd estimate 10-20%, depending on the insurer and the specific vehicle. But keep in mind that using FSD Beta might also increase your premium in some cases — like, if you're using it in a way that's not recommended.

How will self driving EV insurance change in the next 5 years?

In the next 5 years, self driving EV insurance is gonna change dramatically. I mean, we're gonna see more and more vehicles with advanced safety features hitting the market, and that's gonna force insurers to rethink their approach. We're gonna see more discounts for autonomy-related features, and we're gonna see more insurers offering specialized self driving EV insurance products. And who knows — we might even see a whole new market for self driving EV insurance emerge.

That's all from me — go save some money. — Alex