Last Tuesday, a guy named Marcus emailed me asking why his Ioniq 5 quote jumped 40%. He's a freelance writer, uses his car for work, and thought he was getting a decent rate. Sound familiar? Know what the kicker is? His insurer, Geico, didn't account for his business use, which bumped up his premium. That one stung.

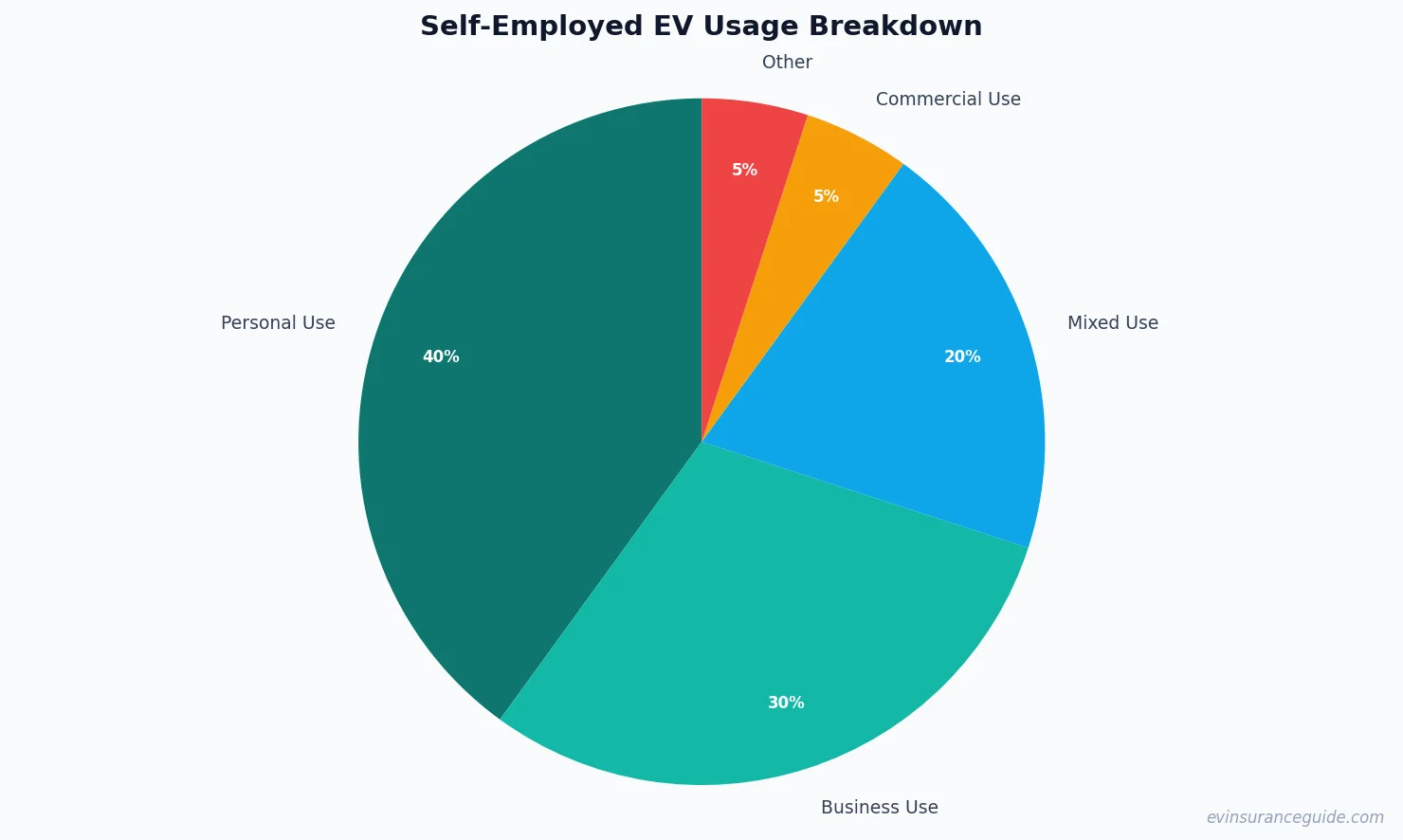

A Story of Mixed Use and Missed Savings

I've seen this story play out time and time again - self-employed individuals and freelancers struggling to find the right EV insurance coverage. They're not sure how to navigate the complex world of personal and business use, and it's costing them. Take Sarah, for example, who drives a Tesla Model 3 for both personal and business use. She's a consultant, and her car is her office on wheels. She's got a good rate with State Farm, but she's not sure if she's getting the best deal. Wild, right? The thing is, insurance companies like Allstate and Progressive are starting to offer more specialized policies for EV owners, but it's still a minefield out there.

But here's the thing: you don't have to break the bank to get good coverage. I'd recommend shopping around, comparing quotes from different insurers, and looking for policies that specifically cater to EV owners. And don't be afraid to negotiate - you can often get a better rate by bundling your policies or asking about discounts. For instance, USAA offers a discount for military members and veterans, while Liberty Mutual offers a discount for certain professions.

Tesla Insurance Cost vs. BMW iX: Which is More Expensive to Insure?

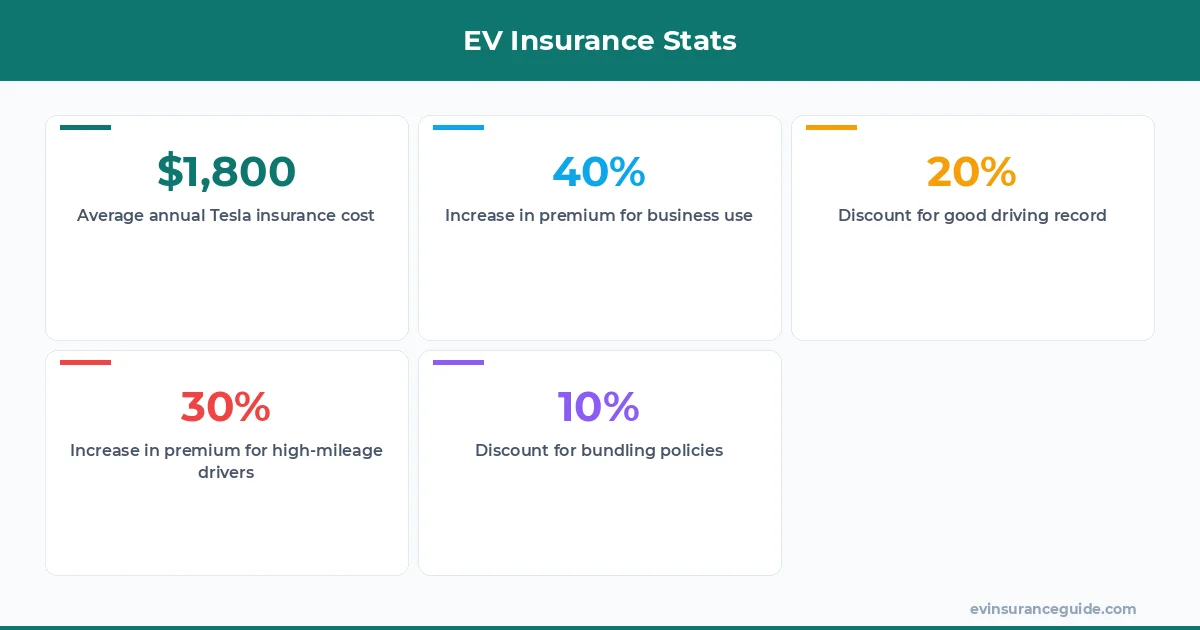

So, how does the Tesla insurance cost compare to other EVs on the market? Well, actually, it's not always the most expensive option. The BMW iX, for example, can be pricier to insure, especially if you're looking at the higher-end models. But, on average, you're looking at around $1,800 per year for a Tesla Model Y, while the BMW iX can cost upwards of $2,200 per year. Know what the difference is? It's not just the car itself, but the insurance company's perception of risk. Tesla's got a reputation for being a bit more...let's say, 'adventurous' when it comes to Autopilot and other features. That's reflected in the premium.

Now, I know what you're thinking: what about the Hyundai Ioniq 5? Isn't that a more affordable option? And yeah, it is - the Ioniq 5 is a great choice for those on a budget. But, when it comes to insurance, it's not always the cheapest option. I've seen quotes ranging from $1,400 to $1,900 per year, depending on the trim level and other factors. So, it's not a clear-cut winner in terms of cost. But, hey, at least you've got options, right?

And let's not forget about the Rivian - a newer player in the EV market, but one that's making waves. The Rivian R1T is a beast of a truck, and it's got a price tag to match. But, when it comes to insurance, it's not as bad as you'd think. I've seen quotes around $2,000 per year, which is comparable to some of the other high-end EVs on the market.

7 Things to Know Before Buying EV Insurance as a Self-Employed Individual

OK, so you're a self-employed individual or freelancer, and you're looking to buy EV insurance. Here are a few things to keep in mind:

- 1. Your business use will affect your premium - it's not just about the car itself, but how you use it.

- 2. Shop around - don't just stick with one insurer, compare quotes and look for the best deal.

- 3. Consider a commercial policy - if you're using your car primarily for business, it might be cheaper to go with a commercial policy.

- 4. Look for discounts - many insurers offer discounts for things like good driving records, low mileage, or certain professions.

- 5. Don't skimp on coverage - you get what you pay for, so make sure you've got adequate coverage in case something goes wrong.

- 6. Read the fine print - know what you're getting into before you sign on the dotted line.

- 7. And finally, don't be afraid to ask questions - your insurer should be able to answer any questions you have about your policy.

Pro tip: always read the fine print, and don't be afraid to ask questions. Your insurer should be able to explain everything in plain English, so don't be shy.

But, and this is a big but, you've got to be honest about your business use. If you're not, you could be in for a world of trouble. I've seen cases where self-employed individuals have underestimated their business use, only to have their claim denied when they need it most. That's why it's so important to be accurate when reporting your business use - it's not worth the risk of having your claim denied.

Honestly, Some EV Insurance Policies are Overpriced Trash

I'm gonna say it: some EV insurance policies are just plain bad. They're overpriced, underwhelming, and don't offer the kind of coverage you need. Take, for example, the policy offered by Esurance - it's around $2,500 per year for a Tesla Model 3, which is just ridiculous. You can do better than that. Look for policies that offer flexible coverage options, discounts for good driving habits, and a reputation for paying out claims quickly. Anything less, and you're just throwing your money away.

And don't even get me started on the companies that try to upsell you on unnecessary features. I mean, do you really need roadside assistance if you've got a Tesla with Autopilot? Probably not. So, be smart, and don't fall for the sales pitch.

OK So Here's the Deal With Tesla Insurance Cost and Business Use

So, you're a self-employed individual or freelancer, and you're looking to navigate the complex world of EV insurance. Here's the deal: you've got to be smart about it. You've got to shop around, compare quotes, and look for policies that cater to your specific needs. And don't be afraid to negotiate - you can often get a better rate by bundling your policies or asking about discounts. For instance, if you've got a good driving record, you might be eligible for a discount. Or, if you've got a low mileage, you might be able to get a lower rate.

And let's talk about the cost - the average Tesla insurance cost is around $1,800 per year, but it can vary depending on the model, trim level, and other factors. The Tesla Model Y, for example, is one of the most popular models, and it's got a relatively low insurance cost. But, the Tesla Model S is a different story - it's a more expensive car, and it's got a higher insurance cost to match.

But, at the end of the day, it's all about finding the right balance between cost and coverage. You don't want to overpay for insurance, but you also don't want to skimp on coverage. So, take your time, do your research, and find the policy that's right for you.

FAQs

#### What is the average Tesla insurance cost?

The average Tesla insurance cost is around $1,800 per year, but it can vary depending on the model, trim level, and other factors.

#### How does business use affect my EV insurance premium?

Your business use will affect your premium - it's not just about the car itself, but how you use it. You'll need to report your business use accurately to ensure you're getting the right coverage.

#### Can I get a discount on my EV insurance?

Yes, many insurers offer discounts for things like good driving records, low mileage, or certain professions. You can also bundle your policies or ask about discounts to get a better rate.

#### What is the best EV insurance company for self-employed individuals?

There's no one-size-fits-all answer to this question - it depends on your specific needs and circumstances. However, companies like State Farm, Allstate, and Progressive offer a range of policies that cater to self-employed individuals and freelancers.

#### How do I report my business use to my insurer?

You'll need to report your business use accurately to your insurer - this may involve keeping a log of your mileage, tracking your business use, or providing documentation to support your claim.

#### Can I use my personal EV insurance policy for business use?

It depends on your policy - some personal policies may cover business use, but it's not always the case. You may need to purchase a commercial policy or add a rider to your personal policy to cover your business use.

#### What happens if I don't report my business use accurately?

If you don't report your business use accurately, you could be in for a world of trouble. Your claim could be denied, or you could face higher premiums or even policy cancellation.

Keep those batteries topped up and those premiums low. — Alex