Buying insurance for your Tesla Model 3 or Model Y is kinda like buying a new pair of shoes - you want the best fit, but you also don't wanna break the bank. And when it comes to total loss, that's when the real fun begins... or not. I mean, who wants to deal with adjusters and claims, right? But, what if I told you that the total loss payout for your EV might be lower than you'd expect? Sound familiar?

What's the Total Loss Payout for My Tesla?

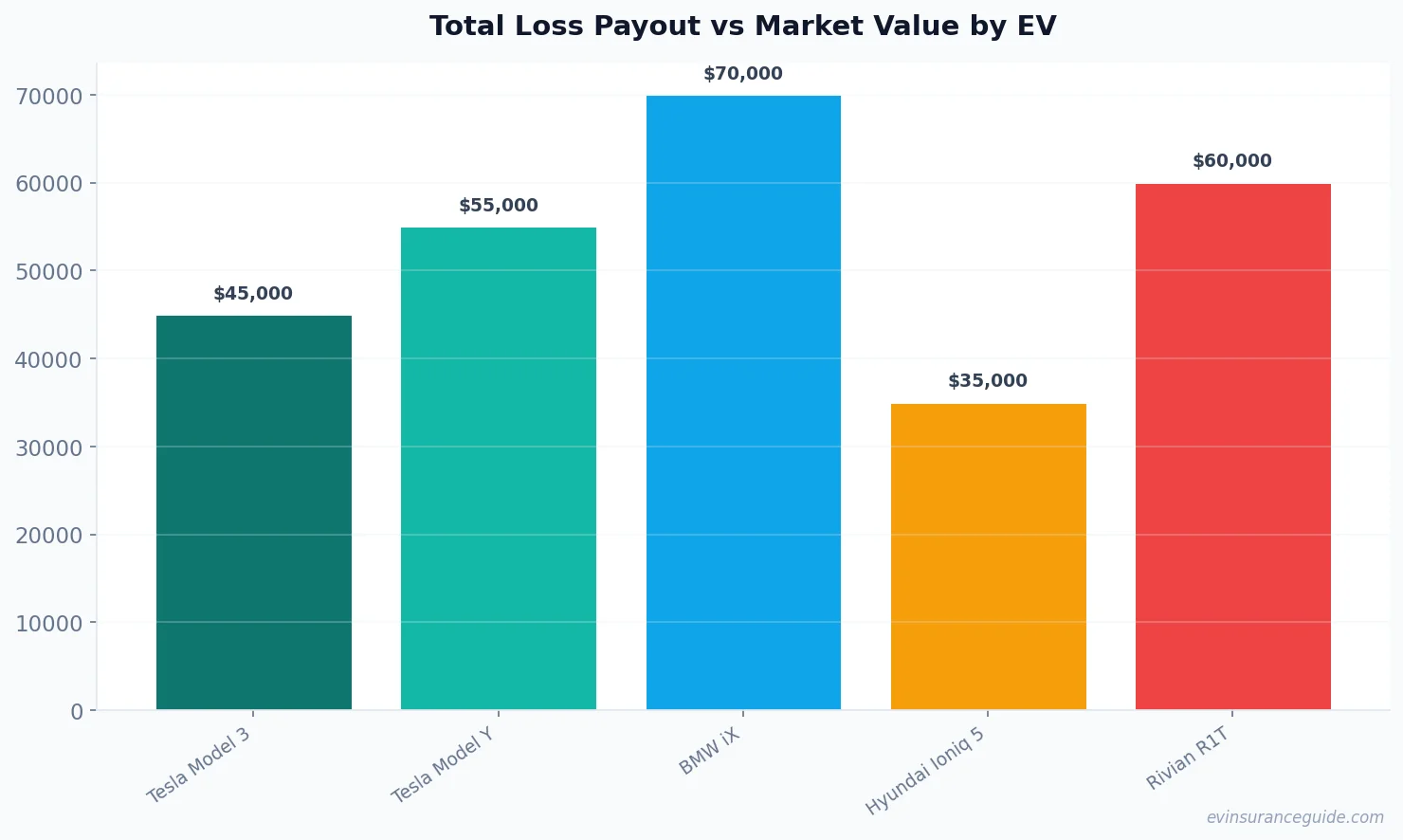

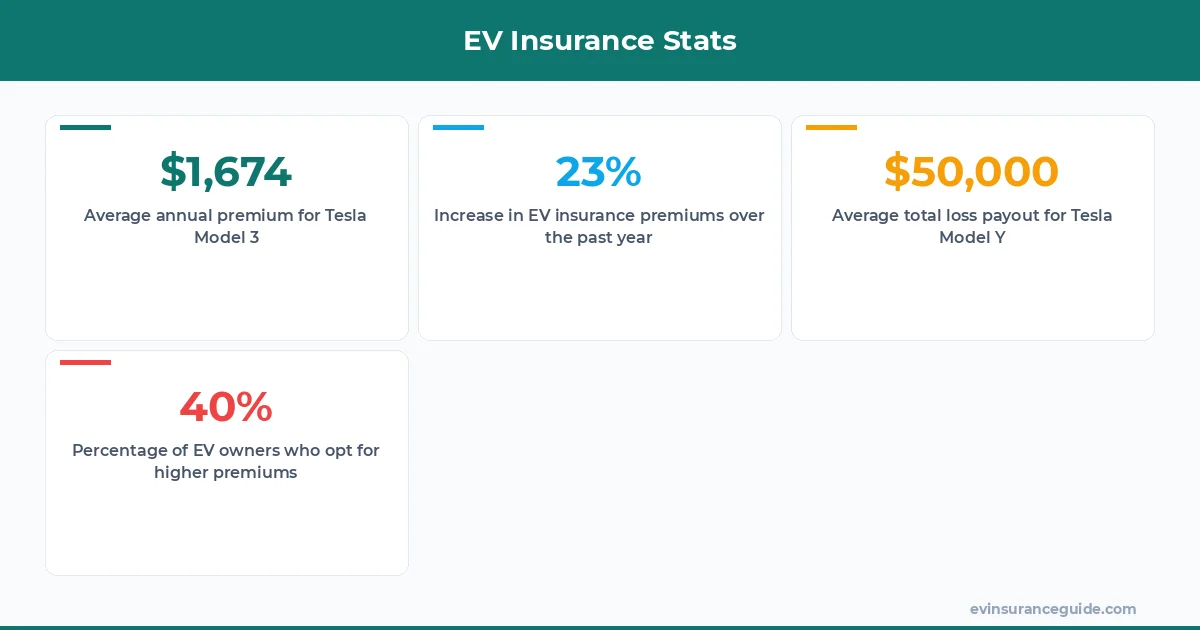

Well, actually, it depends on several factors, like the age of your vehicle, its condition, and - you guessed it - the insurance company. For instance, if you've got a brand new Tesla Model Y, and it's totaled in an accident, you might expect to get around $50,000 to $60,000, depending on the trim level and options. But, if you've got a 3-year-old Model 3, that payout could be more like $35,000 to $45,000. Know what the kicker is? Your Tesla insurance cost can affect the total loss payout, too. Yep, you read that right - the more you pay for insurance, the more you might get in a total loss payout. Wild, right?

Now, I know some of you might be thinking, "But Alex, what about the BMW iX or the Hyundai Ioniq 5? How do their total loss payouts compare?" Well, let me tell you - those EVs have their own set of rules. For example, the BMW iX, being a luxury EV, might have a higher total loss payout, around $70,000 to $80,000, due to its higher purchase price. On the other hand, the Hyundai Ioniq 5, being a more affordable option, might have a lower payout, around $30,000 to $40,000.

The Story of How I Learned the Hard Way

I've got a buddy, let's call him Dave, who owns a Rivian R1T. He was involved in a pretty bad accident, and his truck was totaled. Long story short, the insurance company offered him around $40,000, which was way lower than what he expected. That one stung. But, here's the thing - Dave had opted for a lower premium, which meant he had a higher deductible. So, in the end, he was out of pocket for around $10,000. Ouch. The moral of the story? Don't skimp on the insurance premium, folks. You get what you pay for.

As it turns out, Dave's experience wasn't an isolated incident. I've heard similar stories from other EV owners, including some Tesla Model 3 and Model Y owners. It seems that the total loss payout can vary significantly depending on the insurance company and the specific policy. So, it's crucial to do your research and choose an insurance provider that offers a fair total loss payout.

Busting the Myth: Total Loss Payouts are Always Fair

Myth: Total loss payouts are always fair and based on the market value of your vehicle. Reality: Not always. I've seen cases where the insurance company has lowballed the payout, citing "depreciation" or "condition" as the reason. But, what about the Tesla insurance cost? Doesn't that factor in? Dead serious, folks - if you don't negotiate, you might end up with a payout that's way lower than what you deserve.

Pro tip: Always keep detailed records of your vehicle's maintenance, including receipts and photos. This can help you build a case for a higher total loss payout if needed.

Now, I'm not saying all insurance companies are out to get you. But, it's crucial to be aware of the potential pitfalls. For instance, some insurance providers might use a "total loss formula" that takes into account the vehicle's age, mileage, and condition. While this might sound fair, it can sometimes result in a lower payout than expected.

Warning: Don't Fall for the Low-Premium Trap

You might be tempted to opt for a lower premium, thinking you'll save some cash. But, beware - that lower premium might come with a higher deductible, which could leave you out of pocket in the event of a total loss. And, let's not forget about the Tesla insurance cost. If you're not careful, you might end up with a policy that's overpriced trash. This policy is overpriced trash, if you ask me.

For example, let's say you've got a Tesla Model 3, and you opt for a lower premium with a higher deductible. If your car is totaled, you might be looking at a payout of around $40,000. But, if you'd opted for a higher premium with a lower deductible, that payout could be more like $50,000. See the difference? It's all about weighing the costs, folks.

5 Things You Need to Know About Total Loss Payouts

Here are the top 5 things you need to know about total loss payouts for your EV:

- 1. The total loss payout can vary depending on the insurance company and policy.

- 2. Your Tesla insurance cost can affect the total loss payout.

- 3. Keeping detailed records of your vehicle's maintenance can help you build a case for a higher payout.

- 4. Be aware of the potential pitfalls, such as lowball offers from insurance companies.

- 5. Don't fall for the low-premium trap - it might come with a higher deductible.

FAQs

What's the average total loss payout for a Tesla Model 3?

The average total loss payout for a Tesla Model 3 can range from $35,000 to $50,000, depending on the age, condition, and trim level of the vehicle.

How does the Tesla insurance cost affect the total loss payout?

The Tesla insurance cost can affect the total loss payout, as a higher premium might result in a higher payout.

Can I negotiate the total loss payout with my insurance company?

Yes, you can negotiate the total loss payout with your insurance company. It's essential to keep detailed records of your vehicle's maintenance and to be prepared to make a case for a higher payout.

What's the best way to avoid a low total loss payout?

The best way to avoid a low total loss payout is to choose an insurance provider that offers a fair total loss payout, and to opt for a policy with a lower deductible.

What's the difference between the total loss payout and the market value of my vehicle?

The total loss payout might be lower than the market value of your vehicle, depending on the insurance company and policy. It's crucial to understand the terms of your policy and to negotiate if necessary.

How can I get a higher total loss payout for my EV?

To get a higher total loss payout for your EV, keep detailed records of your vehicle's maintenance, and be prepared to make a case for a higher payout. You can also consider opting for a policy with a lower deductible and a higher premium.

That's all from me — go save some money. — Alex