Last Tuesday, a guy named Marcus emailed me asking why his Ioniq 5 quote jumped 40%. He'd just upgraded from a base model to the N Line, and suddenly his insurance premium skyrocketed. Sound familiar? Know what the kicker is? The insurer didn't even mention the 0-60 time as a factor, just a generic 'performance enhancement' surcharge. Wild, right?

OK So Here's the Deal With Performance EV Insurance

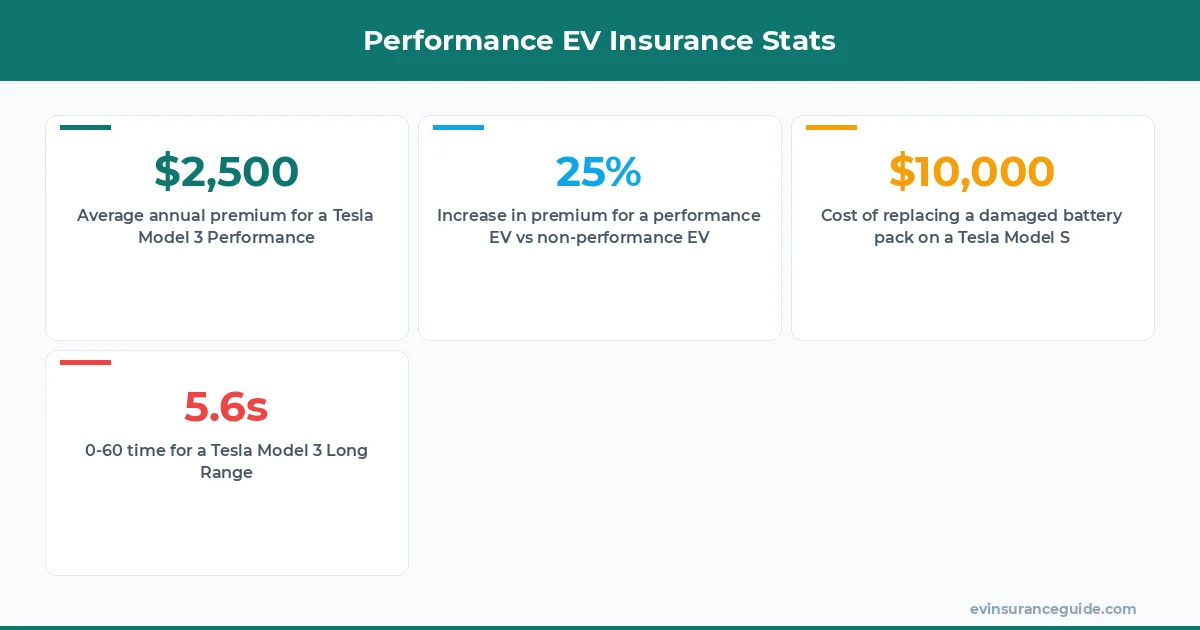

Performance EVs like the Tesla Model 3, BMW iX, and Rivian are a whole different ball game when it comes to insurance. You're looking at premiums that can range from $1,500 to $3,000 per year, depending on your location, driving record, and... you guessed it, the car's performance specs. That one stung for Marcus, who was expecting a much lower quote. Dead serious, some insurers will charge you an extra $500 just for having a dual-motor setup.

The thing is, these cars are not your average daily drivers. They're built for speed, with 0-60 times that can leave even the most seasoned drivers grinning from ear to ear. The Tesla Model 3 Performance, for instance, can go from 0-60 in just 3.2 seconds. That's crazy fast, and insurers know it. They're gonna charge you for that kind of power, no question.

But here's the thing: not all insurers are created equal. Some, like State Farm, have specific policies for performance EVs, while others will just lump you into a generic 'high-performance vehicle' category and charge you an arm and a leg. You gotta shop around, and that's where I come in – to help you navigate the world of performance EV insurance and find the best deals out there.

A Story of Two EV Owners: Tesla Insurance vs State Farm

Meet Rachel, who owns a Tesla Model Y Long Range. She's a safe driver, with a spotless record, and she's always been happy with her insurance premiums. That is, until she decided to upgrade to the Performance trim. Suddenly, her premium jumped by 25%, and she was faced with a difficult decision: stick with her current insurer or shop around for a better deal.

Rachel's story is not unique, sadly. Many EV owners have reported similar experiences, with some even seeing their premiums double or triple after upgrading to a performance model. The reason? Insurers see these cars as high-risk, high-reward investments. They know that drivers who opt for performance EVs are more likely to push their cars to the limit, which increases the risk of accidents and claims.

But what about State Farm, you ask? Well, they're actually one of the more EV-friendly insurers out there. They offer specific policies for Tesla owners, including the Model 3 and Model Y, and their rates are often competitive with other major insurers. However, their quotes can vary widely depending on your location and driving record, so it's always a good idea to shop around and compare rates.

Warning: Don't Fall for the 'Performance Surcharge' Trap

There's a sneaky little thing that some insurers like to call a 'performance surcharge'. It's a fancy way of saying 'we're gonna charge you more because your car is fast', and it can add hundreds of dollars to your premium. The thing is, these surcharges are not always transparent, and some insurers won't even tell you what you're paying for.

That's why it's so important to read the fine print and ask questions. Don't be afraid to push back against these surcharges, especially if you're not sure what you're getting for your money. And remember, not all insurers are created equal – some will charge you more for the same coverage, simply because they can.

One pro tip is to look for insurers that offer 'usage-based' insurance, which can help you save money if you're a safe driver. These policies use data from your car to track your driving habits, and if you're driving safely, you can earn discounts on your premium. It's a win-win, and it's definitely worth exploring if you're in the market for a new policy.

If you're in the market for a performance EV, don't assume that your current insurer will give you the best rate. Shop around, and don't be afraid to negotiate – it could save you thousands of dollars in the long run.

What Affects Your Performance EV Insurance Premium the Most?

Know what the biggest factor is in determining your performance EV insurance premium? It's not the car's horsepower, surprisingly, but its 0-60 time. Yep, you read that right – how fast your car can go from 0-60 is a major determinant of your insurance premium. The reason is simple: faster cars are more likely to be involved in accidents, which increases the risk for insurers.

But what about other factors, like the car's value or your driving record? Don't get me wrong, those things matter too, but they're not as important as the 0-60 time. For instance, a Tesla Model 3 with a 0-60 time of 5.6 seconds will generally be cheaper to insure than a Model 3 with a 0-60 time of 3.2 seconds, even if the latter is a base model.

And let's not forget about the cost of repairs – performance EVs are often more expensive to fix than their non-performance counterparts, which can drive up your premium. For example, replacing a damaged battery pack on a Tesla Model S can cost upwards of $10,000, which is a significant expense for insurers.

5 Key Factors in Performance EV Insurance

There are several key factors that affect your performance EV insurance premium, including the car's 0-60 time, horsepower, and value. Here are the top 5 factors to consider:

- 1. 0-60 time: As mentioned earlier, this is a major determinant of your premium. Faster cars are more expensive to insure.

- 2. Horsepower: While not as important as the 0-60 time, the car's horsepower still plays a role in determining your premium. More powerful cars are generally more expensive to insure.

- 3. Car value: The value of your car is also a factor, as more expensive cars are more costly to repair or replace.

- 4. Driving record: Your driving record is a key factor in determining your premium, as a clean record can help lower your rates.

- 5. Location: Where you live can also affect your premium, as some areas are considered higher-risk than others.

FAQs

#### What is the average annual premium for a performance EV?

The average annual premium for a performance EV can range from $1,500 to $3,000, depending on the car's specs and your driving record.

#### Can I save money by opting for a non-performance EV?

Yes, you can save money by opting for a non-performance EV. These cars are generally cheaper to insure, as they're less powerful and less likely to be involved in accidents.

#### Do all insurers offer performance EV insurance?

No, not all insurers offer performance EV insurance. Some may not have specific policies for these cars, or they may charge higher premiums due to the increased risk.

#### How can I lower my performance EV insurance premium?

You can lower your premium by shopping around, maintaining a clean driving record, and opting for a usage-based insurance policy.

#### What is the most expensive performance EV to insure?

The most expensive performance EV to insure is often the Tesla Model S Plaid, which can have an annual premium of upwards of $5,000.

#### Can I negotiate my performance EV insurance premium?

Yes, you can negotiate your premium by shopping around and comparing rates from different insurers.

Happy driving, and don't overpay! — Alex