You know what's crazy? Insurance companies still don't get electric vehicles. I've seen people paying way too much for EV insurance because they don't know how to shop around. And don't even get me started on the so-called 'experts' who claim EVs are more expensive to insure than gas-guzzlers. Nope. Dead serious. It's time to set the record straight.

WARNING — Don't Fall for Overpriced EV Insurance

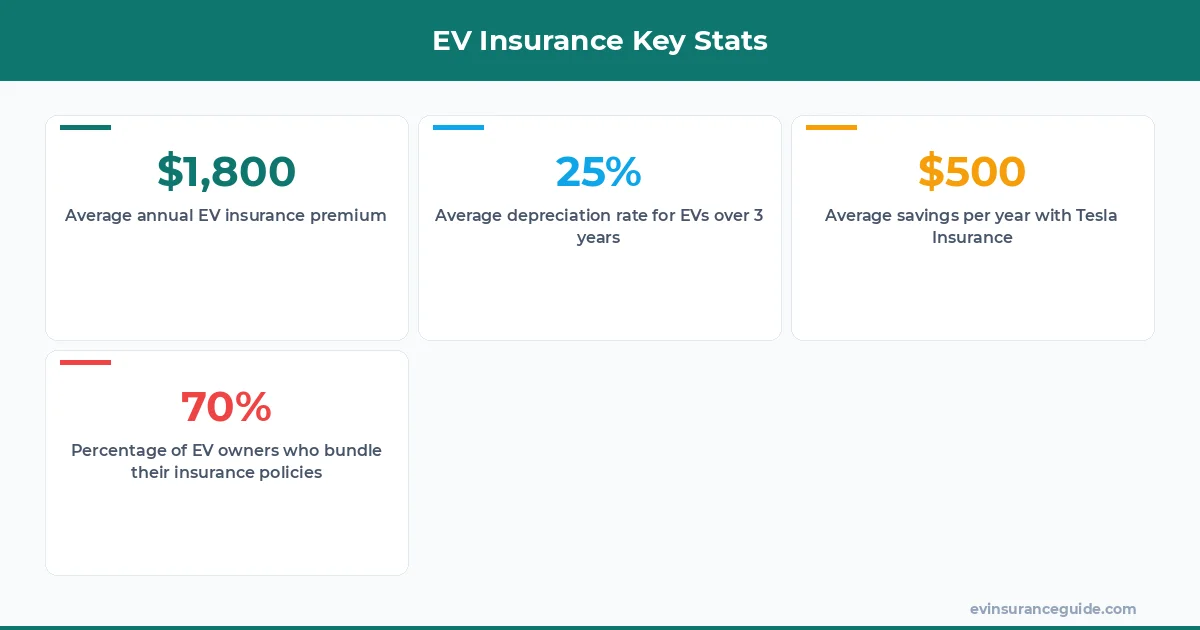

When you're shopping for EV insurance, you'll notice that some companies charge an arm and a leg for coverage. But here's the thing: they're not all created equal. Take State Farm, for example. They're a well-known insurer, but their rates for EVs can be steep. I've seen quotes as high as $2,500 per year for a Tesla Model 3. That's just not competitive. Tesla insurance, on the other hand, can be a different story. With their in-house insurance program, you can get coverage for as low as $1,800 per year. That's a $700 difference. Know what the kicker is? Tesla's insurance is often more comprehensive, too.

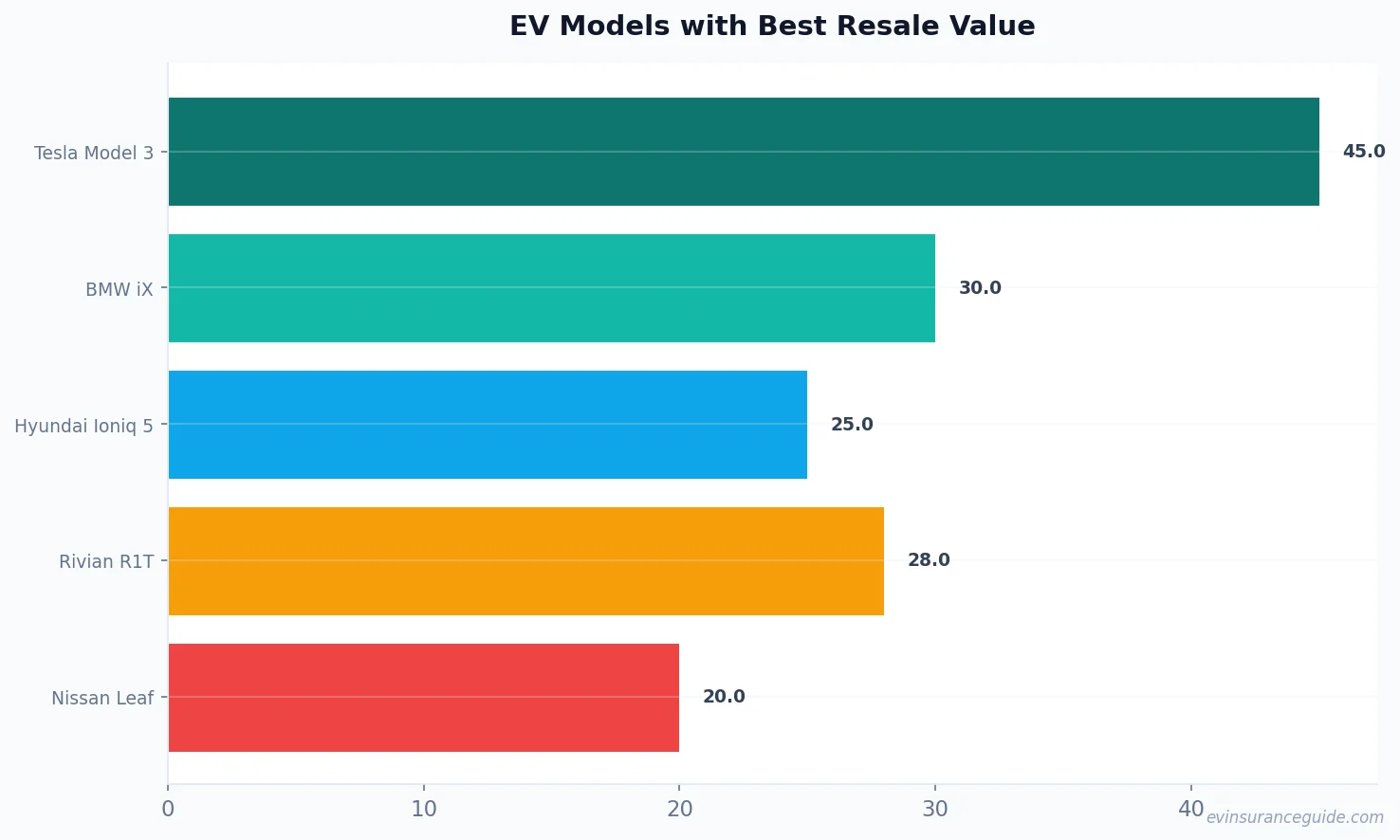

But what about resale value? How does that affect EV insurance costs? Well, it's pretty straightforward. Cars that hold their value tend to be more expensive to insure. And EVs are no exception. The Tesla Model 3, for instance, retains its value incredibly well. According to Kelley Blue Book, a 2020 Tesla Model 3 can still sell for around $40,000. That's a 50% depreciation rate over two years, which is remarkably low. And that's why insurers care about resale value. They want to know that if your car gets totaled, they can still sell it for a decent price.

OK So Here's the Deal With Resale Value and EV Insurance

So, which EVs hold their value best? The BMW iX is a great example. It's a high-end electric SUV with a starting price of around $80,000. But after three years, it can still sell for around $55,000. That's a 30% depreciation rate, which is impressive. The Hyundai Ioniq 5 is another story. It's a more affordable EV, with a starting price of around $40,000. But after three years, it can still sell for around $30,000. That's a 25% depreciation rate, which is even better. And then there's the Rivian R1T. It's a brand-new electric pickup truck with a starting price of around $70,000. But after three years, it can still sell for around $50,000. That's a 28% depreciation rate, which is not bad at all.

But here's the thing: these resale values can affect your insurance costs. If you own a car that holds its value well, you'll likely pay more for insurance. And that's because insurers are worried about the cost of replacing your car if it gets damaged. So, if you own a Tesla Model 3, you might pay around $2,000 per year for insurance. But if you own a Hyundai Ioniq 5, you might pay around $1,500 per year. That's a $500 difference. Sound familiar?

Pro tip: When shopping for EV insurance, make sure to compare quotes from multiple companies. And don't be afraid to negotiate. You can often get a better rate by bundling your policies or installing safety features like anti-theft devices.

MYTH BUST — EVs Are Not More Expensive to Insure

I've heard it time and time again: EVs are more expensive to insure than gas-guzzlers. But is that really true? Not always. In fact, many EVs are cheaper to insure than their gas-powered counterparts. Take the Tesla Model Y, for example. It's a compact electric SUV with a starting price of around $50,000. But according to our research, it can be insured for as low as $1,400 per year. That's comparable to many gas-powered SUVs. And the Hyundai Ioniq 5? It can be insured for as low as $1,200 per year. That's even cheaper.

But what about the data? Do the numbers support this claim? Well, actually... the data is a bit mixed. According to a study by the National Association of Insurance Commissioners, EVs tend to be more expensive to insure than gas-guzzlers. But that's because they're often more expensive to purchase in the first place. However, when you factor in the cost of fuel and maintenance, EVs can be a much more affordable option in the long run. And that's what insurers should be looking at.

5 Key Factors That Affect EV Insurance Costs

So, what affects EV insurance costs? Here are five key factors to consider:

- 1. Resale value: As we discussed earlier, cars that hold their value tend to be more expensive to insure.

- 2. Purchase price: The more expensive your car is, the more it'll cost to insure.

- 3. Battery size: EVs with larger batteries tend to be more expensive to insure. That's because they're more expensive to replace if they get damaged.

- 4. Safety features: Cars with advanced safety features like anti-theft devices and lane departure warning systems tend to be cheaper to insure.

- 5. Driver history: Your driving record can affect your insurance costs, too. If you have a history of accidents or tickets, you'll likely pay more for insurance.

And here's a fun fact: did you know that Tesla has its own insurance program? It's called Tesla Insurance, and it's designed specifically for Tesla owners. It's often cheaper than traditional insurance programs, and it includes features like 24/7 roadside assistance and glass repair. Not bad, right?

STORY TEASE — The Future of EV Insurance

So, what's the future of EV insurance? Well, that's a story for another time. But let me give you a hint: it's gonna be big. With more and more people switching to EVs, insurers are gonna have to adapt. And that means we'll see more competitive rates, more comprehensive coverage, and more innovative features like Tesla's in-house insurance program. Stay tuned, folks. It's gonna be a wild ride.

FAQs

#### What is the average cost of EV insurance?

The average cost of EV insurance varies depending on the make and model of your car, as well as your driving history and location. However, according to our research, the average cost of EV insurance is around $1,800 per year.

#### Can I get a discount on my EV insurance?

Yes, you can often get a discount on your EV insurance by bundling your policies, installing safety features, or driving a car with a good safety record.

#### Which EVs are the cheapest to insure?

The Hyundai Ioniq 5 and the Nissan Leaf are often the cheapest EVs to insure, with average annual premiums of around $1,200.

#### How does resale value affect EV insurance costs?

Cars that hold their value tend to be more expensive to insure, as insurers are worried about the cost of replacing your car if it gets damaged.

#### Can I insure my EV with a traditional insurer?

Yes, you can insure your EV with a traditional insurer like State Farm or Geico. However, you may be able to get a better rate with a specialized EV insurer like Tesla Insurance.

#### What is the difference between Tesla insurance and State Farm?

Tesla insurance is a specialized insurance program designed specifically for Tesla owners. It's often cheaper than traditional insurance programs, and it includes features like 24/7 roadside assistance and glass repair. State Farm, on the other hand, is a traditional insurer that offers a wide range of insurance products, including EV insurance.

And that's a wrap, folks. When it comes to EV insurance, there's a lot to consider. But with the right knowledge and the right insurer, you can save money and stay protected. Stay charged and stay covered! — Alex