Last Tuesday, a guy named Marcus emailed me asking why his Ioniq 5 quote jumped 40%. We went back and forth, and it turned out his insurer had started using driving data from his car's onboard computer. That one stung - he was a good driver, but the data told a different story. Sound familiar?

WARNING — The Data Trap

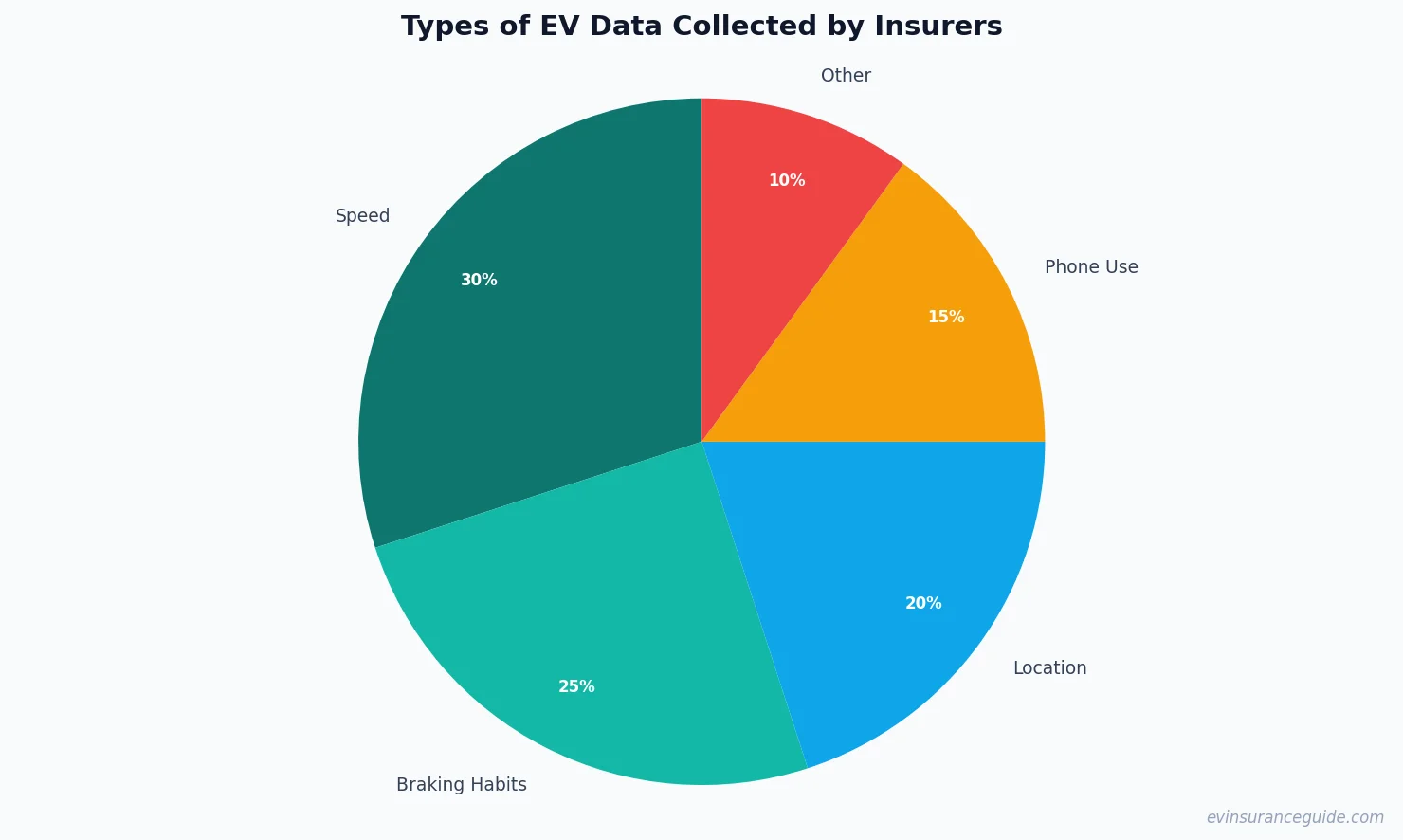

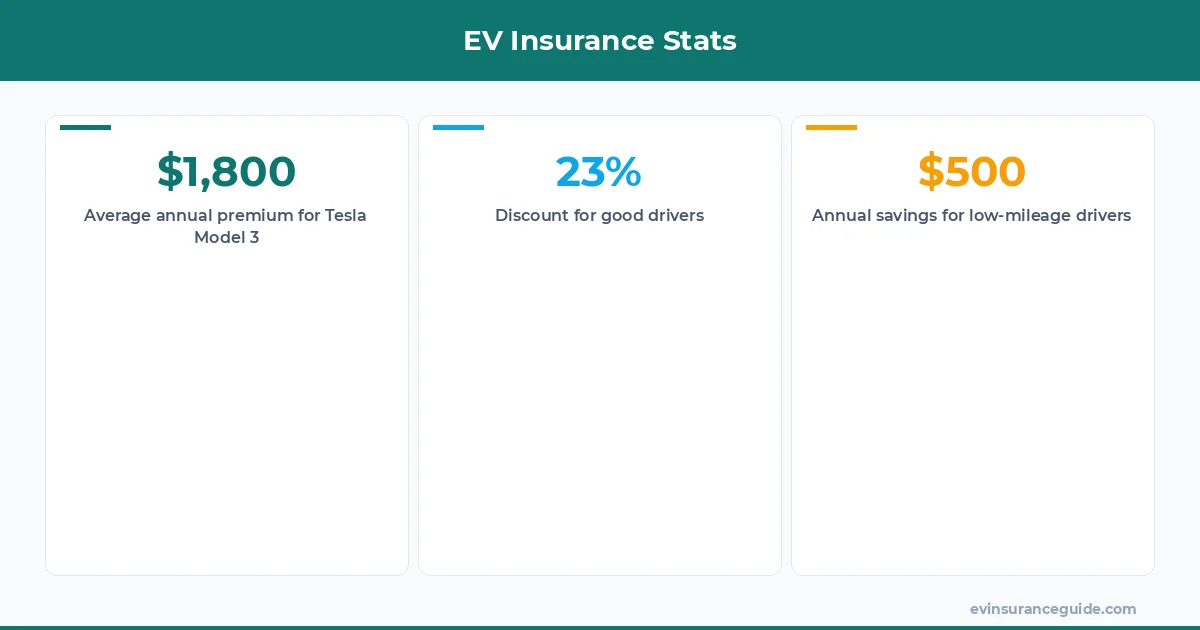

You see, most EV owners don't realize their cars are sending a ton of data to insurers. We're talking everything from speed and braking habits to location and even phone use. It's like having a built-in spy, and it can seriously affect your Tesla Model 3 insurance cost. For instance, if you're a Tesla Model 3 owner and you drive aggressively, your insurance rates could skyrocket - we're talking $1,800 to $2,500 per year, easy. But, if you drive a BMW iX and you're super cautious, you might get a discount - around 10% to 15% off your annual premium.

Take Rivian owners, for example. Their cars come with all sorts of fancy tech, including a built-in data collection system. And, let's be real, that data can be a double-edged sword. On the one hand, it can help you prove you're a good driver and get lower rates. On the other hand, it can also show insurers all the times you sped or brake-checked, and that'll cost you. Know what the kicker is? Some insurers are using this data to raise rates for even the smallest infractions - like going 5 mph over the limit. Wild, right?

Now, I know some of you are thinking, 'But Alex, I'm a great driver! I don't speed, I don't brake-check, and I always wear my seatbelt.' And that's awesome - you should be rewarded for being a good driver. The problem is, the data collection system doesn't always tell the whole story. Maybe you were driving on a windy road and had to brake hard to avoid a deer. Maybe you were in a situation where you had to speed up to avoid an accident. The data doesn't care - it just shows that you were speeding or braking hard, and that's all the insurer needs to raise your rates.

STORY_TEASE — The Case of the Skyrocketing Quote

I've got a friend, let's call her Emily, who owns a Hyundai Ioniq 5. She's a great driver, always follows the rules, and never speeds. But, one day, she got a quote from her insurer that was 50% higher than the previous year. She was shocked - what had changed? It turned out that the insurer had started using data from her car's onboard computer, and it showed that she was braking hard more often than average. The thing is, Emily lives in a city with really bad roads, and she was just trying to avoid potholes. But, the data didn't show that - it just showed that she was braking hard, and that was enough to raise her rates.

This is just one example of how data collection can affect your Tesla Model 3 insurance cost. And, let's be real, it's not just about the data itself - it's about how insurers use it. Some insurers are using data to reward good drivers, while others are using it to punish them. It's like a big game of cat and mouse, and you need to be aware of the rules to come out on top. For instance, if you're a Tesla Model Y owner and you drive less than 7,000 miles per year, you might be eligible for a low-mileage discount - around $200 to $300 per year.

So, what can you do to avoid getting caught in the data trap? First, you need to understand what data your car is collecting and how it's being used. You can do this by checking your car's manual or contacting your insurer directly. You should also be aware of your driving habits and try to improve them - even small changes can make a big difference in your insurance rates. And, if you do get a quote that seems too high, don't be afraid to shop around - there are plenty of insurers out there who are willing to work with you to get you a better rate.

5 Things to Know About EV Data Collection

There are a few things you should know about EV data collection and how it affects your Tesla Model 3 insurance cost. First, not all insurers use data collection - some still rely on traditional methods like questionnaires and driving records. Second, the type of data collected can vary - some insurers collect data on speed and braking habits, while others collect data on location and phone use. Third, you have the right to opt out of data collection - but, be aware that this might affect your rates. Fourth, some states have laws regulating data collection - so, it's worth checking your local laws to see what's allowed. And, fifth, data collection is just one factor that affects your insurance rates - there are plenty of other things you can do to lower your rates, like improving your credit score or taking a defensive driving course.

For example, if you're a Tesla Model 3 owner and you have a good credit score - above 750 - you might be eligible for a discount - around 10% to 15% off your annual premium. And, if you take a defensive driving course, you might be able to lower your rates even further - around 5% to 10% off your annual premium. It's all about being aware of the factors that affect your rates and taking steps to improve them.

COMPARISON — Tesla Model 3 Insurance Cost vs. Other EVs

When it comes to Tesla Model 3 insurance cost, it's worth comparing it to other EVs on the market. For instance, the BMW iX is a great car, but it's also one of the most expensive to insure - around $2,500 to $3,500 per year. The Hyundai Ioniq 5, on the other hand, is relatively affordable - around $1,800 to $2,500 per year. And, the Rivian is somewhere in between - around $2,000 to $3,000 per year. So, what's the difference? It all comes down to data collection and how insurers use it.

If you're a Tesla Model 3 owner, you might be wondering how your insurance rates compare to other EV owners. The truth is, it's all about the data - and how insurers use it. Some insurers are using data to reward good drivers, while others are using it to punish them. It's like a big game of cat and mouse, and you need to be aware of the rules to come out on top. For example, if you're a Tesla Model Y owner and you drive less than 10,000 miles per year, you might be eligible for a low-mileage discount - around $300 to $500 per year.

HONEST_OPINION — The Truth About EV Data Collection

Let's be real - EV data collection is a double-edged sword. On the one hand, it can help you prove you're a good driver and get lower rates. On the other hand, it can also show insurers all the times you sped or brake-checked, and that'll cost you. As someone who's been in the industry for a while, I gotta say - it's a bit of a nightmare. Insurers are using data collection to raise rates and make more money, and it's not always fair. But, there are some insurers out there who are using data collection to reward good drivers - and that's the way it should be.

Pro tip: always review your driving data before submitting it to your insurer. You might be surprised at what it shows - and you can use that information to negotiate a better rate.

And, let's not forget about the cost - EV data collection can be expensive. Some insurers are charging extra for data collection services, and that can add up quickly. For example, if you're a Tesla Model 3 owner and you opt for data collection, you might be charged an extra $100 to $200 per year. But, if you're a good driver, it might be worth it - you could save around $500 to $1,000 per year on your insurance rates.

FAQs

#### What is EV data collection?

EV data collection is the process of collecting data from your electric vehicle's onboard computer. This data can include everything from speed and braking habits to location and phone use.

#### How does EV data collection affect my insurance rates?

EV data collection can affect your insurance rates in a number of ways. If you're a good driver, data collection can help you prove it and get lower rates. But, if you're a bad driver, data collection can show insurers all the times you sped or brake-checked, and that'll cost you.

#### Can I opt out of EV data collection?

Yes, you can opt out of EV data collection. But, be aware that this might affect your rates. Some insurers offer discounts for data collection, so if you opt out, you might not be eligible for those discounts.

#### How much does EV data collection cost?

The cost of EV data collection can vary. Some insurers charge extra for data collection services, while others include it in the cost of your insurance premium. On average, you can expect to pay around $100 to $200 per year for data collection services.

#### What are the benefits of EV data collection?

The benefits of EV data collection include lower insurance rates for good drivers, improved road safety, and more accurate insurance quotes. Data collection can also help you identify areas where you need to improve your driving habits.

#### Is EV data collection secure?

Yes, EV data collection is secure. Insurers use advanced security measures to protect your data, including encryption and secure servers. But, it's always a good idea to review your driving data before submitting it to your insurer to make sure it's accurate.

And, finally,

Happy driving, and don't overpay! — Alex