So, you've finally got your hands on a brand new Tesla Model 3 - congrats, that's a dream car for many. But, let's talk about the not-so-glamorous part: insurance. I mean, who doesn't love paying hundreds of dollars every year for something they hope they'll never need? And, to make matters worse, there's this hidden factor that can significantly impact your premiums: your credit score. Yep, you read that right - your credit score. It's like, you're already paying a premium for that sleek electric vehicle, and now you've got to worry about your credit history too? Sounds familiar?

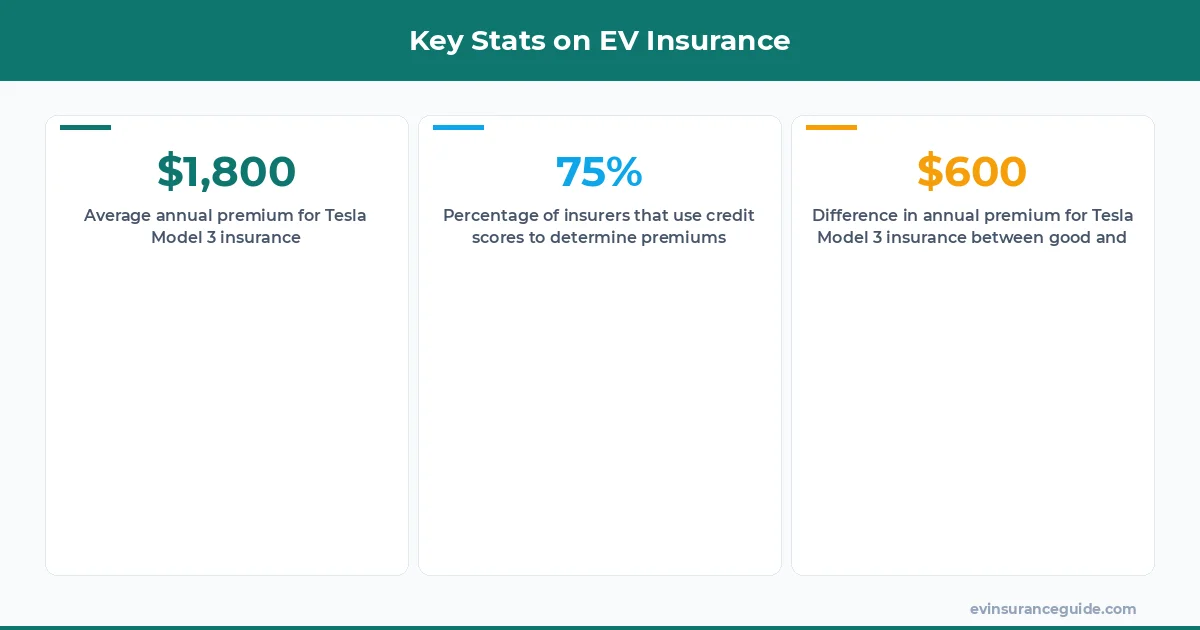

1. 75% of Insurers Use Credit Scores to Determine Premiums

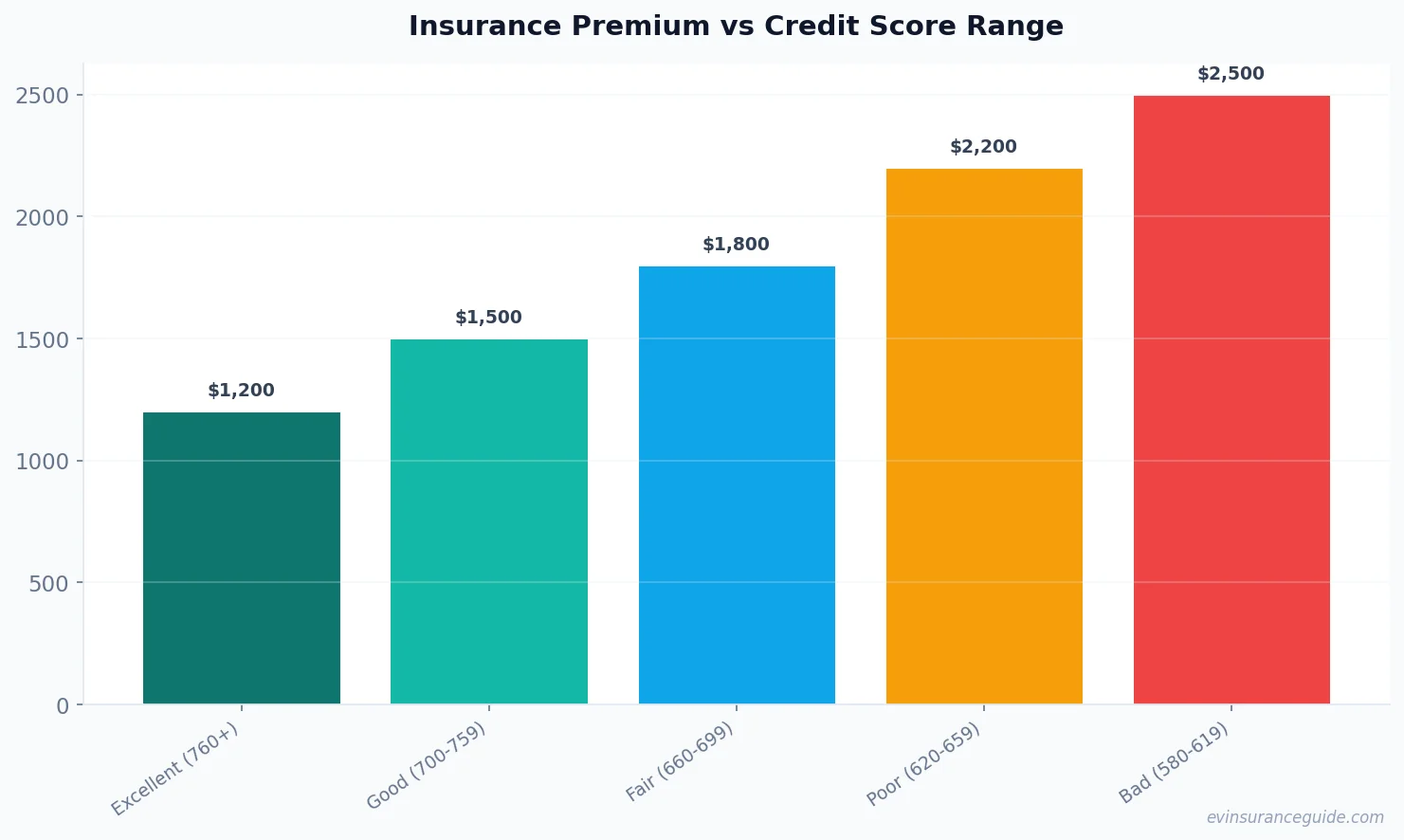

The thing is, most people don't even realize that their credit score is being used to determine their insurance premiums. I mean, it's not like they're gonna put it in bold letters on the policy documents or anything. But, the fact is, around 75% of insurers use credit scores to determine premiums. That's a pretty big deal, if you ask me. And, it's not just about being a responsible borrower - it's about being a responsible driver, too. So, if you've got a poor credit score, you can expect to pay more for your Tesla Model 3 insurance. For instance, a driver with a credit score of 600 might pay around $1,800 per year for their Tesla Model 3 insurance, while someone with a credit score of 800 might pay around $1,200 per year. That's a difference of $600, just because of their credit score. Wild, right?

Now, I know what you're thinking: "But, Alex, why do insurers care about my credit score?" Well, it's simple - they've found that people with good credit scores are less likely to file claims. And, vice versa, people with poor credit scores are more likely to file claims. It's all about risk assessment, my friend. So, if you've got a good credit score, you're seen as a lower risk, and you'll get a better deal on your insurance. But, if you've got a poor credit score, you're seen as a higher risk, and you'll pay more. It's as simple as that.

Honest Opinion: Credit Score-Based Insurance is Unfair

Honest opinion: the whole credit score-based insurance thing is kinda unfair. I mean, what if you've got a poor credit score, but you're an amazing driver? Shouldn't that count for something? It's like, you're being punished for something that's not even related to your driving skills. And, what about people who are just starting out, and they don't have a credit history yet? Shouldn't they get a fair shot, too? It's just not right, if you ask me. The system's gotta change, or at least, insurers should start taking other factors into account, like driving history, or something.

But, for now, we're stuck with the system we've got. So, what can you do to improve your credit score, and get a better deal on your Tesla Model 3 insurance? Well, first of all, you've got to check your credit report, and make sure there are no errors on it. You can do this for free, once a year, through websites like AnnualCreditReport.com. Then, you've got to start building a positive credit history, by paying your bills on time, and keeping your credit utilization ratio low. It's not rocket science, but it does take some effort.

A Story of How Credit Score Impacted Insurance Costs

So, let me tell you a story about my friend, Rachel. She's a huge EV fan, and she recently bought a brand new Hyundai Ioniq 5. She was so excited to get behind the wheel, but then she got her insurance quote, and she was shocked. It was way higher than she expected, and she couldn't understand why. So, she started digging, and she realized that her credit score was the culprit. She had a few late payments on her credit card, and it had tanked her credit score. She was devastated, but she didn't give up. She started working on her credit score, and after a few months, she was able to get a much better deal on her insurance. She saved around $500 per year, just by improving her credit score. That one stung, but it was a valuable lesson.

Now, I know what you're thinking: "Alex, this is all well and good, but what about people who don't have a credit history?" Well, that's a great question. The thing is, insurers are starting to use alternative credit scoring models, that take into account other factors, like rent payments, or utility bills. It's not perfect, but it's a start. And, some insurers are even offering discounts for people who don't have a credit history, but have a good driving record. So, there are options out there, you just have to shop around.

Comparison: Tesla Model 3 Insurance vs BMW iX Insurance

So, let's compare the insurance costs of two popular EVs: the Tesla Model 3, and the BMW iX. Now, I know what you're thinking: "Alex, these are two very different cars, with different price tags, and different features." And, you're right. But, let's just look at the insurance costs, and see what we can find. According to our research, the average annual insurance premium for a Tesla Model 3 is around $1,800. For a BMW iX, it's around $2,500. That's a difference of $700, just because of the car model. Now, I know that's not the only factor that determines insurance costs, but it's definitely one of them.

But, here's the thing: insurance costs can vary widely, depending on a lot of factors, including your location, your driving history, and your credit score. So, it's not just about the car model, it's about you, as a driver. And, that's what insurers are trying to assess, when they're determining your premiums. They want to know, what's the likelihood that you'll file a claim, and how much will it cost them, if you do. It's all about risk assessment, my friend.

Can You Get a Good Deal on Tesla Model 3 Insurance with Bad Credit?

So, can you get a good deal on Tesla Model 3 insurance, if you have bad credit? Well, it's not impossible, but it's definitely harder. You'll have to shop around, and compare quotes from different insurers, to find the best deal. And, you might have to consider a higher deductible, or a less comprehensive policy, to get a lower premium. But, it's not all doom and gloom. Some insurers specialize in high-risk drivers, and they might offer better deals, even with bad credit. So, don't give up, just keep looking.

Pro tip: When shopping for insurance, make sure to ask about discounts for good driving habits, or for being a member of certain organizations. You might be surprised at what you can get.

And, don't forget to check your credit report, and work on improving your credit score. It's not just about getting a better deal on your insurance, it's about being financially responsible, and having a better financial future. So, take control of your finances, and start building a positive credit history. Your wallet will thank you, and so will your insurer.

FAQs

#### What is the average credit score required for Tesla Model 3 insurance?

The average credit score required for Tesla Model 3 insurance is around 700. However, this can vary widely, depending on the insurer, and other factors.

#### How much does Tesla Model 3 insurance cost?

The cost of Tesla Model 3 insurance can vary widely, depending on a lot of factors, including your location, your driving history, and your credit score. On average, it can cost around $1,800 per year.

#### Can I get a discount on Tesla Model 3 insurance if I have a good driving record?

Yes, you can get a discount on Tesla Model 3 insurance, if you have a good driving record. Some insurers offer discounts for good driving habits, such as accident-free driving, or low mileage.

#### What is the impact of credit score on Tesla Model 3 insurance premiums?

The impact of credit score on Tesla Model 3 insurance premiums is significant. According to our research, a driver with a credit score of 600 might pay around $1,800 per year for their Tesla Model 3 insurance, while someone with a credit score of 800 might pay around $1,200 per year. That's a difference of $600, just because of their credit score.

#### How can I improve my credit score to get a better deal on Tesla Model 3 insurance?

You can improve your credit score by paying your bills on time, keeping your credit utilization ratio low, and monitoring your credit report for errors. You can also consider working with a credit counselor, or using a credit monitoring service, to help you improve your credit score.

#### What are some tips for getting a good deal on Tesla Model 3 insurance with bad credit?

Some tips for getting a good deal on Tesla Model 3 insurance with bad credit include shopping around, comparing quotes from different insurers, and considering a higher deductible, or a less comprehensive policy. You can also try working with a broker, or an insurance agent, who specializes in high-risk drivers.

#### Can I get Tesla Model 3 insurance with no credit history?

Yes, you can get Tesla Model 3 insurance with no credit history. However, you might have to pay a higher premium, or consider a different type of insurance policy. Some insurers offer alternative credit scoring models, that take into account other factors, such as rent payments, or utility bills.

So, there you have it - the lowdown on how your credit score impacts your Tesla Model 3 insurance cost. It's not the most glamorous topic, but it's an important one. And, now that you know the facts, you can start working on improving your credit score, and getting a better deal on your insurance.

Go get yourself a better quote. You deserve it. — Alex