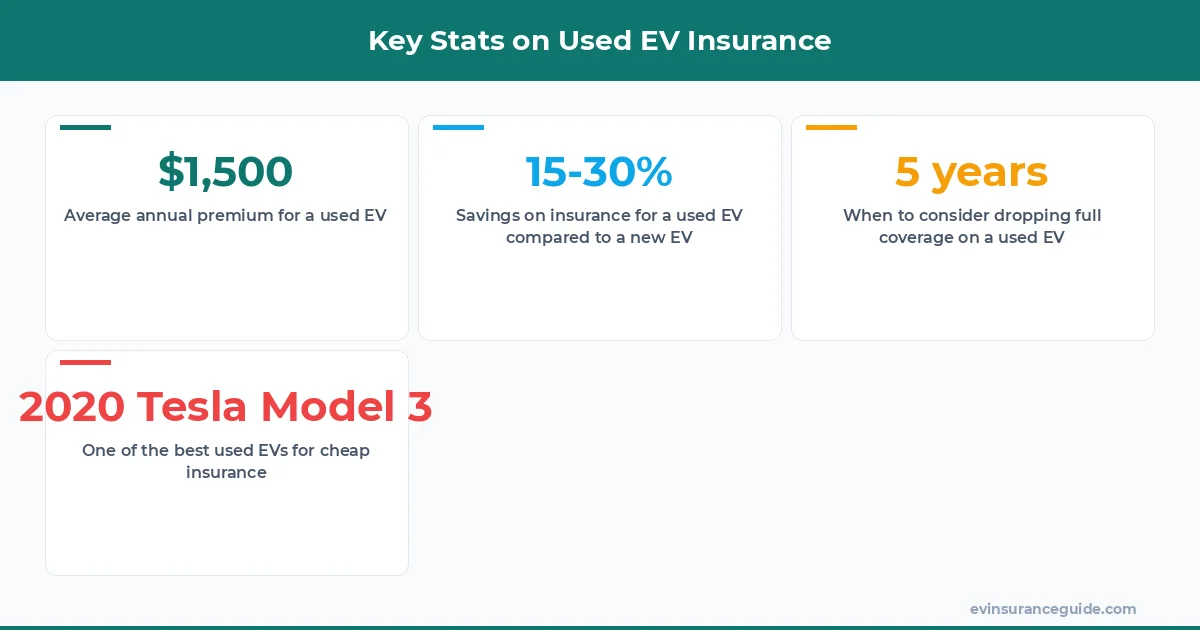

Insurance for a used EV can be a real bargain - think 15-30% cheaper than insuring a brand new model. That's a significant chunk of change, especially when you're already saving money by buying a pre-owned vehicle. For instance, a 1-year-old Tesla Model 3 might set you back around $340 per month, while a 3-year-old model could be as low as $280 per month. But what about a 5-year-old EV? You're looking at a monthly premium of around $220. Sound familiar?

Comparing Apples to Oranges: New vs Used EV Insurance

When it comes to insurance, used EVs are often the way to go if you want to save some cash. But don't just take my word for it - the numbers speak for themselves. A 2022 Tesla Model Y, for example, might have an average annual premium of around $1,800. Compare that to a 2019 model, which could be as low as $1,300 per year. That's a difference of $500, folks. Know what the kicker is? You can use that extra money to upgrade your vehicle's tech or even invest in some fancy new wheels. Wild, right?

So, what's the best way to find cheap insurance for your used EV? Well, actually, it's not that complicated. You just need to do your research and shop around. Don't be afraid to compare quotes from different insurance companies, like Geico or Progressive. And don't even get me started on the importance of reading reviews - you want to make sure you're working with a reputable company that's gonna have your back in case something goes wrong.

Pro tip: Always check the insurance company's financial ratings before making a decision. You don't want to be stuck with a company that's gonna leave you high and dry when you need them most.

But, I mean, how much is insurance for a used EV, really? It depends on a lot of factors, including the vehicle's make and model, its age, and even your location. For example, a 2020 BMW iX might have an average annual premium of around $1,600 in California, but that same vehicle could cost over $2,000 per year to insure in New York. And what about a Hyundai Ioniq 5? You're looking at an average annual premium of around $1,400. Not bad, right?

Warning: Don't Get Caught in the Trap of Overpriced Insurance

Okay, so you've found a great deal on a used EV - congratulations, you're one step ahead of the game. But don't get too excited just yet, because you still need to factor in the cost of insurance. And let me tell you, it's not always a straightforward process. Some insurance companies might try to sell you on all sorts of extra coverage options, like roadside assistance or rental car insurance. And while those things might be nice to have, they're not always necessary. So, be careful not to get caught in the trap of overpriced insurance. You don't want to end up paying more than you need to, especially when you're already saving money by buying a used vehicle.

For instance, a company like Allstate might offer you a bunch of different coverage options, but they might not always be the cheapest. You need to do your research and compare quotes from different companies to find the best deal. And don't be afraid to negotiate - if you're a good driver with a clean record, you might be able to get a better rate. Just remember, it's all about finding that sweet spot between affordability and coverage. You don't want to sacrifice one for the other, or you'll be sorry. Dead serious.

So, what's the best way to avoid overpriced insurance? Well, it's pretty simple, really. Just make sure you're working with a reputable company, and always read the fine print before signing anything. You don't want to get stuck with a policy that's gonna cost you an arm and a leg. And hey, if you're not sure about something, just ask. That's what the insurance company is there for, right?

But, I mean, it's not always easy to find the right insurance company. There are so many out there, and they all seem to be offering the same thing. So, how do you choose? Well, that's a great question. Know what I always say? Do your research, and don't be afraid to ask around. You can even check out online reviews to see what other people are saying about a particular company.

My Honest Opinion: When to Drop Full Coverage on a Used EV

Okay, let's get real for a second. If you're driving a used EV that's more than 5 years old, it's probably time to drop full coverage. I mean, think about it - if your vehicle is worth less than $10,000, it's probably not worth paying for comprehensive and collision coverage. You're basically just throwing money out the window, and that's not what you want to do. So, when should you drop full coverage? Well, it's simple: when the cost of the coverage is more than the value of the vehicle itself. That's just common sense, right?

For example, let's say you've got a 2018 Rivian that's worth around $8,000. If you're paying more than $800 per year for full coverage, it's probably time to drop it. You can just stick with liability insurance, and you'll be good to go. And hey, if you're not sure about the value of your vehicle, you can always check out a website like Kelley Blue Book to get an estimate. Just remember, it's all about being practical and making smart financial decisions. You don't want to be stuck paying for something you don't need, especially when you're on a budget.

But, I mean, what about certified pre-owned vehicles? Don't they deserve full coverage, no matter what? Well, actually, it's not that simple. While certified pre-owned vehicles might be worth more than your average used EV, they're still not always worth the cost of full coverage. You need to do the math and figure out what makes sense for your particular situation. And hey, if you're still not sure, you can always talk to an insurance agent. They'll be able to give you some advice and help you make a decision.

Myth-Busting: Certified Pre-Owned vs Private Sale Insurance Differences

Okay, so you've decided to buy a used EV - congratulations, you're making a great decision. But now you need to think about insurance, and that's where things can get a little tricky. You might be wondering whether it's better to buy a certified pre-owned vehicle or a private sale. And hey, that's a great question. But here's the thing: when it comes to insurance, it doesn't always matter whether you buy a certified pre-owned or a private sale. The cost of insurance is gonna depend on a lot of factors, including the vehicle's make and model, its age, and even your location.

For example, a certified pre-owned 2020 Tesla Model 3 might have an average annual premium of around $1,500, while a private sale 2020 Tesla Model 3 might have an average annual premium of around $1,400. That's not a huge difference, right? But, I mean, what about the benefits of buying a certified pre-owned vehicle? Don't they deserve better insurance rates? Well, actually, it's not that simple. While certified pre-owned vehicles might come with some extra perks, like warranties and inspections, they're not always worth the extra cost. You need to do the math and figure out what makes sense for your particular situation.

5 Key Things to Know About Used EV Insurance

Okay, so you've learned a lot about used EV insurance - congratulations, you're on the right track. But here are 5 key things to keep in mind:

- 1. The cost of insurance is gonna depend on a lot of factors, including the vehicle's make and model, its age, and even your location.

- 2. You should always shop around and compare quotes from different insurance companies to find the best deal.

- 3. Don't be afraid to negotiate - if you're a good driver with a clean record, you might be able to get a better rate.

- 4. Certified pre-owned vehicles might come with some extra perks, but they're not always worth the extra cost.

- 5. You should always read the fine print before signing anything, and make sure you understand what you're getting into.

And, I mean, what about the future of used EV insurance? Is it gonna get cheaper or more expensive? Well, that's a great question. Know what I think? I think it's gonna get cheaper, especially as more and more people start buying used EVs. The market is gonna become more competitive, and insurance companies are gonna have to lower their rates to stay ahead of the game. That's just my two cents, though.

FAQs

#### What is the average cost of insurance for a used EV?

The average cost of insurance for a used EV can vary depending on a lot of factors, including the vehicle's make and model, its age, and even your location. But, on average, you're looking at around $1,500 per year for a 2020 Tesla Model 3.

#### How much is insurance for a used EV, really?

Well, it depends on what you mean by "really". If you're talking about the actual cost of insurance, it can vary depending on a lot of factors. But, on average, you're looking at around $1,500 per year for a 2020 Tesla Model 3. If you're talking about the value of insurance, though, that's a different story. Insurance is worth it if you want to protect yourself and your vehicle in case something goes wrong.

#### What are the best used EVs for cheap insurance?

Some of the best used EVs for cheap insurance include the Tesla Model 3, the Hyundai Ioniq 5, and the BMW iX. These vehicles are all relatively affordable to insure, especially when you compare them to other EVs on the market.

#### When should I drop full coverage on my used EV?

You should drop full coverage on your used EV when the cost of the coverage is more than the value of the vehicle itself. That's just common sense, right? You don't want to be paying more for insurance than your vehicle is worth.

#### Can I negotiate my insurance rate?

Yes, you can negotiate your insurance rate. If you're a good driver with a clean record, you might be able to get a better rate. Just make sure you're working with a reputable company, and always read the fine print before signing anything.

#### What are the benefits of buying a certified pre-owned EV?

The benefits of buying a certified pre-owned EV include warranties, inspections, and other perks. But, I mean, are they worth the extra cost? That's a great question. Know what I think? I think they're not always worth it, especially if you're on a budget.

That's all from me — go save some money. — Alex