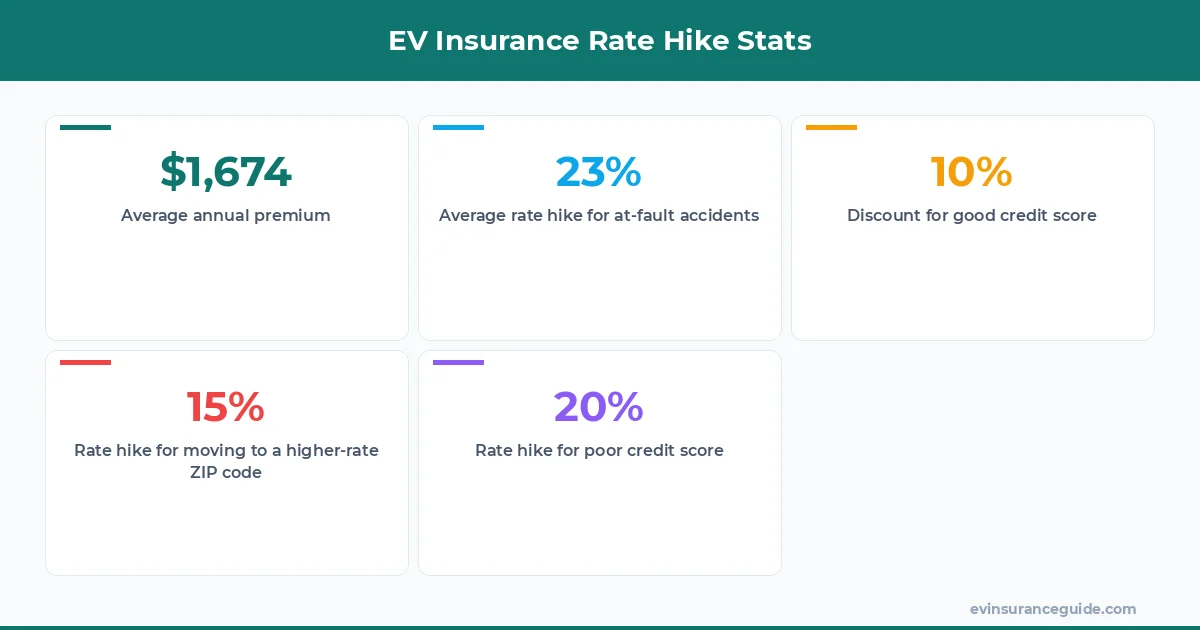

So, let's talk about my friend, Rachel - she's a proud owner of a Tesla Model 3. Last year, she was paying around $1,200 annually for her EV insurance. Fast forward to 2026, and her rates have skyrocketed to over $1,800. Sound familiar? Know what the kicker is? She hasn't changed her driving habits, and her car is still in pristine condition. The big question is - why did her EV insurance go up? Well, actually, it's not just Rachel - the average EV insurance rate has increased by around 8% this year, with some owners seeing hikes as high as 20%. That one stung.

Comparing Apples to Oranges - EV Insurance Rate Hikes

The thing is, when you're shopping for EV insurance, you're not just comparing prices - you're comparing apples to oranges. Different insurers offer varying levels of coverage, deductibles, and discounts. For instance, Geico might offer a lower premium, but their coverage might be limited compared to, say, Progressive. Wild, right? Take the case of the Hyundai Ioniq 5 - its insurance rates have gone up by around 12% this year, primarily due to its high repair costs. The cost of replacing its advanced battery pack can be as high as $10,000. Dead serious - that's a lot of cash.

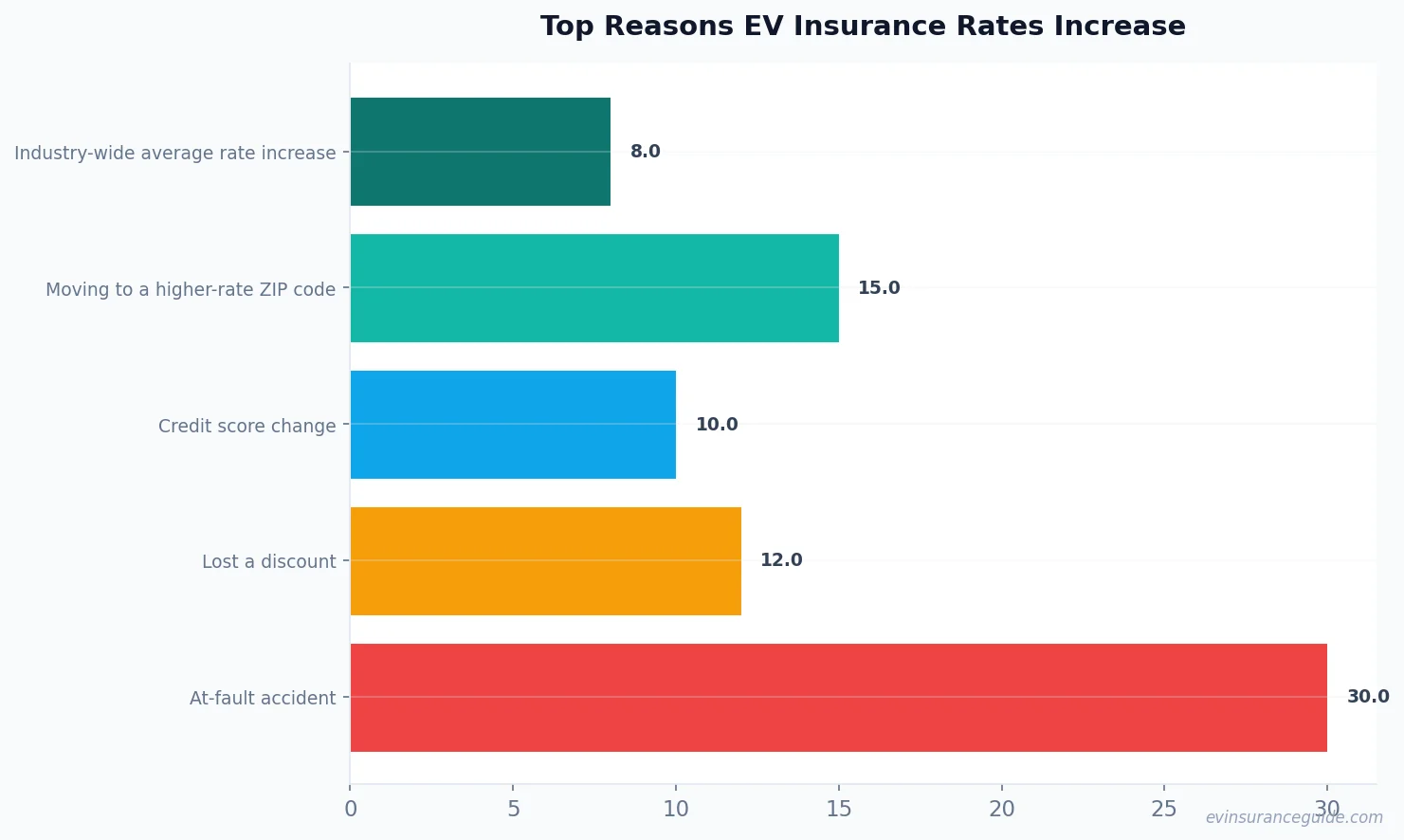

The industry-wide average rate increase of 8% might seem like a lot, but it's essential to understand that different factors contribute to this hike. For example, if you've moved to a higher-rate ZIP code, your premiums could increase by as much as 15%. Yep, you read that right - 15%. But, on the other hand, if you've improved your credit score, you might be eligible for a discount of up to 10%. It's all about understanding the intricacies of EV insurance and how to work the system to your advantage. Know what I mean?

Warning Signs - Hidden Costs and Rate Hikes

You know the old saying - 'what you don't know can't hurt you.' But when it comes to EV insurance, that's just not true. There are hidden costs and rate hikes lurking around every corner, waiting to pounce on unsuspecting owners. Take the case of the BMW iX - its insurance rates have gone up by around 10% this year, primarily due to its high-tech features and advanced safety systems. The thing is, these features might make the car more expensive to repair, but they also make it safer to drive. It's a Catch-22, really. On one hand, you want the latest and greatest tech, but on the other hand, you don't want to break the bank. Sound familiar?

For instance, let's say you own a Rivian R1T, and you've installed a state-of-the-art infotainment system. If you get into an accident, the cost of repairing or replacing that system could be as high as $5,000. That's a lot of money, and it's essential to factor it into your insurance calculations. But, on the other hand, if you've opted for a more basic trim level, your insurance rates might be lower. It's all about finding that delicate balance between features, safety, and affordability. Can't stress this enough - do your research, and don't be afraid to negotiate.

OK So Here's the Deal With Credit Scores and EV Insurance

Credit scores - the bane of many an EV owner's existence. But, actually, they play a significant role in determining your insurance rates. If you've got a good credit score - say, above 750 - you might be eligible for a discount of up to 10%. But, if your credit score is poor - below 600, for instance - you could be looking at a rate hike of as much as 20%. That's a big difference, and it's essential to understand how credit scores impact your EV insurance rates. Take the case of my friend, Alex - he's got a credit score of around 820, and he's paying a premium of around $1,500 per year for his Tesla Model Y. But, if his credit score were to drop to, say, 680, his rates could increase by as much as $300. That's a lot of money, and it's essential to keep your credit score in check.

But, here's the thing - credit scores aren't the only factor that affects your EV insurance rates. Your driving history, the type of car you own, and even your location all play a role. For instance, if you live in a state with high crime rates, your insurance rates might be higher. Or, if you've got a history of accidents or tickets, your rates could be higher as well. It's all about understanding the complexities of EV insurance and how to work the system to your advantage. Blockquote: > Pro tip: Check your credit report regularly to ensure there are no errors that could be affecting your credit score. A good credit score can save you hundreds of dollars on your EV insurance premiums.

The Story of the At-Fault Accident and Its Impact on EV Insurance

So, let's talk about at-fault accidents - the ultimate EV insurance rate hike trigger. If you're involved in an at-fault accident, your rates could increase by as much as 30%. Yep, you read that right - 30%. But, here's the thing - it's not just the accident itself that affects your rates. The severity of the accident, the cost of repairs, and even the type of car you own all play a role. Take the case of the Hyundai Kona Electric - its insurance rates have gone up by around 15% this year, primarily due to its high repair costs. The thing is, if you're involved in an at-fault accident, it's essential to understand how it will impact your EV insurance rates. But, on the other hand, if you've got a good driving record and a clean history, you might be eligible for a discount. It's all about finding that delicate balance between risk and reward.

For instance, let's say you own a Tesla Model 3, and you're involved in a minor fender bender. The cost of repairs might be around $1,000, and your rates might increase by around 10%. But, if you're involved in a more severe accident - say, one that causes $5,000 worth of damage - your rates could increase by as much as 25%. That's a big difference, and it's essential to understand how at-fault accidents impact your EV insurance rates. But, here's the thing - it's not all doom and gloom. If you've got a good driving record and a clean history, you might be eligible for a discount. It's all about finding that delicate balance between risk and reward.

FAQs

#### What is the average cost of EV insurance in 2026?

The average cost of EV insurance in 2026 is around $1,674 per year, with some owners paying as much as $2,500. It's essential to shop around and compare prices to find the best deal.

#### How does my credit score affect my EV insurance rates?

Your credit score plays a significant role in determining your EV insurance rates. If you've got a good credit score - say, above 750 - you might be eligible for a discount of up to 10%. But, if your credit score is poor - below 600, for instance - you could be looking at a rate hike of as much as 20%.

#### What is the impact of an at-fault accident on my EV insurance rates?

If you're involved in an at-fault accident, your rates could increase by as much as 30%. It's essential to understand how at-fault accidents impact your EV insurance rates and to take steps to minimize the damage. This might include taking a defensive driving course or installing safety features in your vehicle.

#### How can I reduce my EV insurance rates?

There are several ways to reduce your EV insurance rates, including improving your credit score, shopping around for quotes, and taking advantage of discounts. You might also consider installing safety features in your vehicle or taking a defensive driving course.

#### What is the difference between comprehensive and collision coverage?

Comprehensive coverage protects you against damage that's not related to an accident - say, theft or vandalism. Collision coverage, on the other hand, protects you against damage that's related to an accident. It's essential to understand the difference between these two types of coverage and to choose the right policy for your needs.

#### Can I customize my EV insurance policy to suit my needs?

Yes, you can customize your EV insurance policy to suit your needs. This might include adding or removing coverage options, adjusting your deductible, or taking advantage of discounts. It's essential to work with an insurer that offers flexible policies and to take the time to understand your options.

#### Why did my EV insurance go up in 2026?

There are several reasons why your EV insurance rates might have increased in 2026, including an industry-wide average rate increase of 8%, moving to a higher-rate ZIP code, or losing a discount. It's essential to understand the reasons behind the rate hike and to take steps to minimize the damage. This might include shopping around for quotes, improving your credit score, or taking advantage of discounts.

Honest Opinion - The Truth About EV Insurance Rate Hikes

So, here's the thing - EV insurance rate hikes are a fact of life. But, it's not all doom and gloom. If you understand the reasons behind the rate hike and take steps to minimize the damage, you can keep your premiums in check. It's all about being informed, shopping around, and taking advantage of discounts. Don't be afraid to negotiate, and don't be afraid to walk away if the deal isn't right. Remember, it's your money, and you should be in control. Know what I mean? Why did my EV insurance go up in 2026? It's a question that's on everyone's mind, and the answer is complex. But, with the right information and the right mindset, you can navigate the world of EV insurance and keep your premiums in check.

Cheers from the EV insurance trenches. — Alex