My friend, Rachel, was paying a whopping $2,500 a year for insurance on her Tesla Model 3... until she switched to a new provider and cut her premiums in half. That's a $1,250 difference - dead serious. She was thrilled, and I was kinda jealous, to be honest. So, what changed? For starters, she dropped collision coverage, which was costing her around $800 per year, and opted for a higher deductible. She also switched to a provider that offered a discount for good driving habits, which saved her an additional $200 per year. Sound familiar? You're probably wondering how you can achieve similar savings.

What Happened to Rachel - A Cautionary Tale

Rachel's story is a great example of how understanding the different types of EV insurance coverage can help you save on premiums. She had been paying for comprehensive coverage, which was costing her around $500 per year, but she realized she didn't need it since her car was already a few years old. By dropping this coverage, she was able to save even more on her premiums. Know what the kicker is? She didn't even notice a difference in her coverage - that's how much she was overpaying. Wild, right? This got me thinking - why is EV insurance so expensive, anyway? Is it the cost of the cars themselves, or is there something more at play?

The cost of EVs is definitely a factor - they're still relatively new and expensive to produce, which drives up the cost of insurance. But there are other factors at play, too. For example, the cost of repairs for EVs can be higher than for gas-powered cars, since they require specialized equipment and training. This can drive up the cost of collision coverage, which can range from $500 to $1,500 per year, depending on the provider and the driver's history. And then there's the issue of battery replacement - if an EV's battery is damaged, it can cost upwards of $10,000 to replace, which can be a significant expense for insurance companies.

Here's the Honest Truth - Why Is EV Insurance So Expensive?

I'm gonna give it to you straight - why is EV insurance so expensive? It's because insurance companies are still figuring out how to price these cars. They're using outdated models and overestimating the risk, which means you're paying more than you need to. Take the Hyundai Ioniq 5, for example - it's a great car, but insurance companies are still charging premiums that are 10-20% higher than they should be. That's because they're basing their rates on the car's MSRP, which can be $40,000 or more, rather than its actual value on the road. This is overpriced trash, if you ask me. You can get a much better deal by shopping around and comparing rates from different providers. For example, Geico is offering premiums as low as $1,200 per year for the Ioniq 5, while State Farm is charging over $2,000 per year.

Pro tip: always compare rates from at least three different providers before making a decision. And don't be afraid to negotiate - if you've been a loyal customer, you may be able to get a better rate by threatening to switch.

The BMW iX is another example - it's a luxury car, but insurance companies are charging premiums that are more in line with a Tesla Model S. That's just not right. You should be able to get a better deal on a car that's not as expensive to repair. And what about the Rivian? It's a new car, but insurance companies are already charging premiums that are through the roof. Why is EV insurance so expensive, indeed?

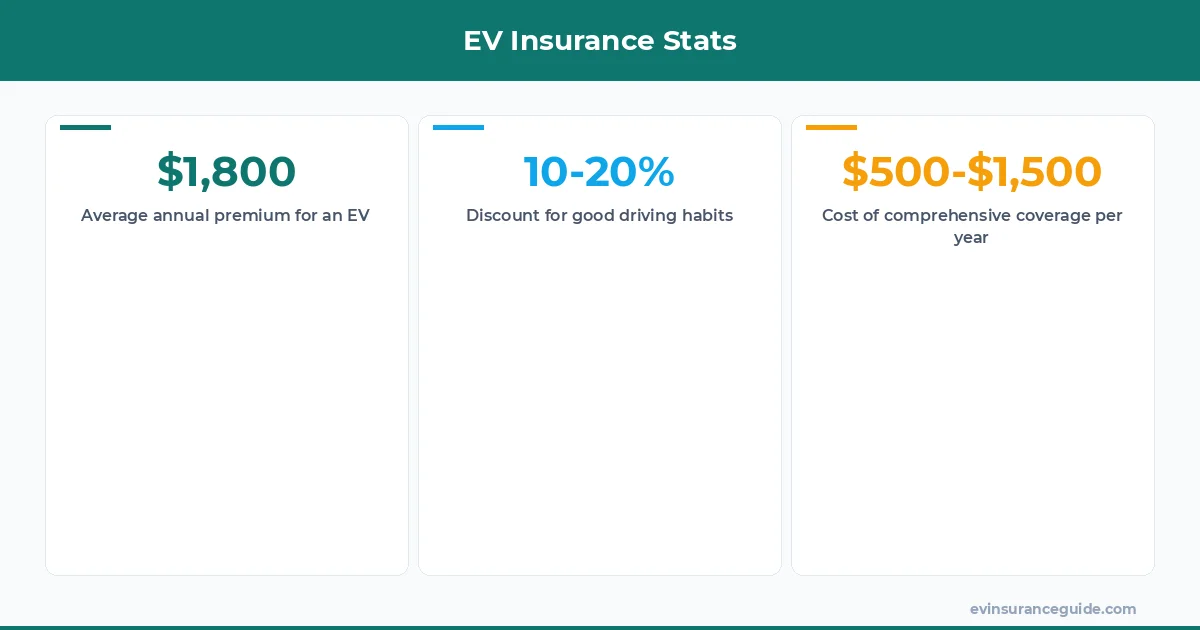

But, OK, let's look at the numbers. According to a recent study, the average annual premium for an EV is around $1,800. That's compared to around $1,300 for a gas-powered car. So, what's driving up the cost of EV insurance? Is it the cost of the cars themselves, or is it something else entirely? Well, actually, it's a combination of both. The cost of EVs is still relatively high, which drives up the cost of insurance. But there are other factors at play, too, like the cost of repairs and the risk of battery replacement.

Busting the Myth - EV Insurance Is Not That Expensive

Myth bust: EV insurance is not that expensive. Sure, it's more expensive than insurance for gas-powered cars, but it's not outrageous. You can get a good deal if you shop around and compare rates. And, let's be real, the cost of insurance is just one factor to consider when buying an EV. You've also got to think about the cost of the car itself, the cost of charging, and the cost of maintenance. Why is EV insurance so expensive, anyway? Is it because insurance companies are still figuring out how to price these cars, or is it because EV owners are more likely to be involved in accidents?

Take the Tesla Model Y, for example. It's a great car, and insurance companies are starting to offer more competitive rates. You can get a premium as low as $1,500 per year, which is not bad considering the car's MSRP is over $50,000. And, if you're a good driver, you can get an even better deal. For example, USAA is offering premiums as low as $1,200 per year for the Model Y, which is a great deal considering the car's value.

OK So Here's the Deal With EV Insurance Coverage

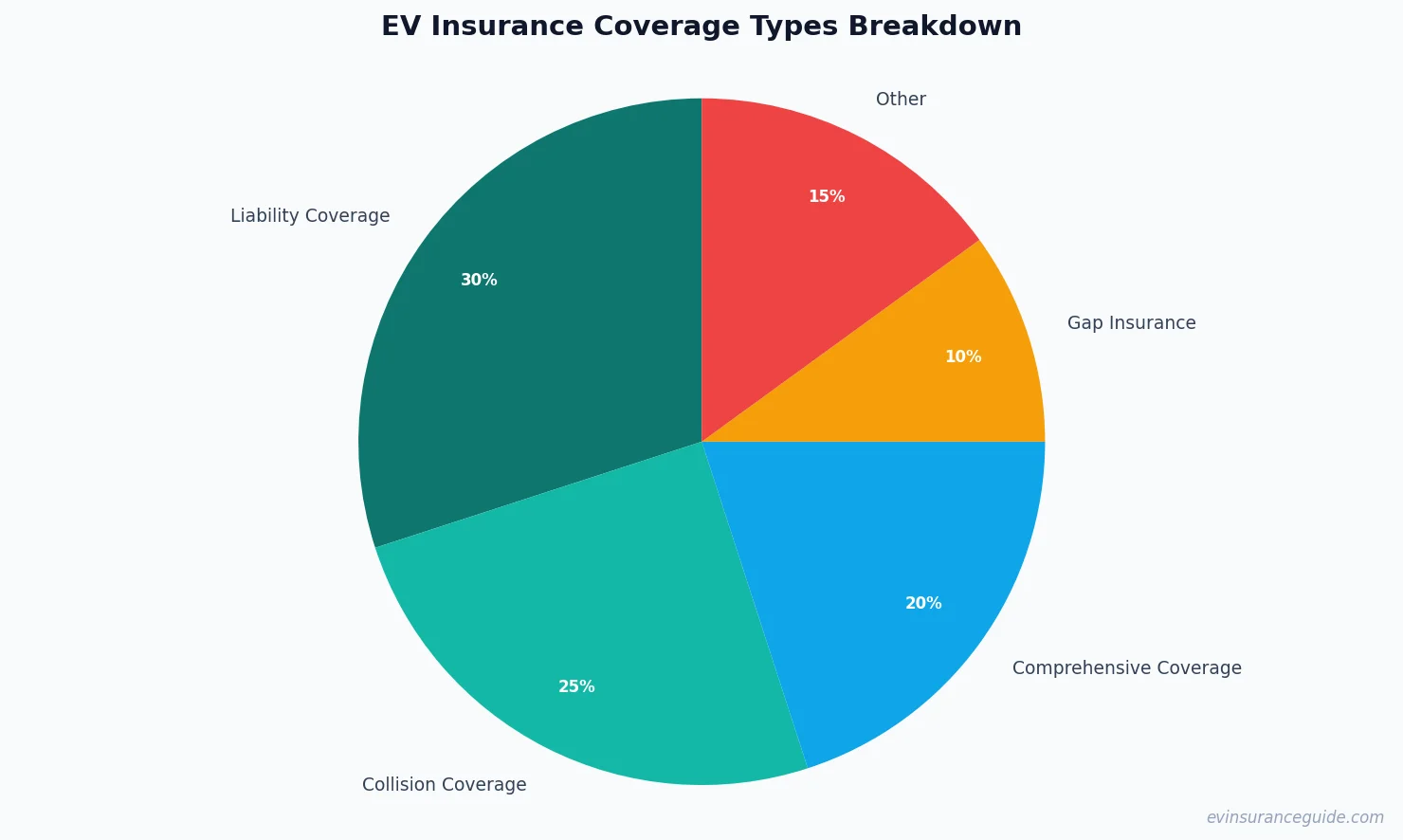

OK, so here's the deal with EV insurance coverage. You've got your liability coverage, which is required by law. This covers damages to other people or property in the event of an accident. Then you've got your collision coverage, which covers damages to your own car. And, finally, you've got your comprehensive coverage, which covers damages that aren't related to an accident, like theft or vandalism. But, why is EV insurance so expensive, anyway? Is it because insurance companies are still trying to figure out how to price these cars, or is it because EV owners are more likely to be involved in accidents?

The cost of comprehensive coverage can range from $200 to $500 per year, depending on the provider and the driver's history. And, if you've got a high-end EV, you may want to consider additional coverage, like gap insurance. This covers the difference between the actual cash value of your car and the amount you still owe on your loan. For example, if your car is worth $30,000, but you still owe $40,000 on your loan, gap insurance would cover the $10,000 difference.

What's the Best Type of EV Insurance Coverage for You?

What's the best type of EV insurance coverage for you? That depends on a few factors, like the value of your car, your driving history, and your budget. If you've got a high-end EV, you may want to consider comprehensive coverage, which can range from $500 to $1,000 per year, depending on the provider and the driver's history. But, if you've got a more budget-friendly EV, like the Nissan Leaf, you may be able to get away with just liability coverage, which can cost as little as $500 per year.

For example, let's say you've got a Tesla Model 3, which is worth around $40,000. You may want to consider comprehensive coverage, which would cover damages to your car in the event of an accident or other incident. But, if you've got a Hyundai Ioniq 5, which is worth around $30,000, you may be able to get away with just liability coverage.

FAQs

#### What is the average annual premium for an EV?

The average annual premium for an EV is around $1,800, although this can vary depending on the provider, the driver's history, and the value of the car.

#### What is the most expensive type of EV insurance coverage?

The most expensive type of EV insurance coverage is comprehensive coverage, which can range from $500 to $1,500 per year, depending on the provider and the driver's history.

#### What is gap insurance, and do I need it?

Gap insurance covers the difference between the actual cash value of your car and the amount you still owe on your loan. If you've got a high-end EV, you may want to consider gap insurance, which can range from $50 to $100 per year, depending on the provider and the driver's history.

#### Can I get a discount on my EV insurance premium?

Yes, you can get a discount on your EV insurance premium by shopping around and comparing rates from different providers. You may also be able to get a discount by bundling your EV insurance with other types of insurance, like home or life insurance.

#### What is the best way to save on EV insurance?

The best way to save on EV insurance is to shop around and compare rates from different providers. You may also be able to save by dropping comprehensive coverage, which can be expensive, or by opting for a higher deductible.

#### What is the difference between liability coverage and comprehensive coverage?

Liability coverage covers damages to other people or property in the event of an accident, while comprehensive coverage covers damages to your own car that aren't related to an accident, like theft or vandalism.

So, there you have it - a breakdown of the different types of EV insurance coverage, and some tips for saving on your premium. Why is EV insurance so expensive, anyway? It's because insurance companies are still figuring out how to price these cars, and they're using outdated models that overestimate the risk. But, by shopping around and comparing rates, you can get a better deal and save on your premium. Happy driving, and don't overpay! — Alex