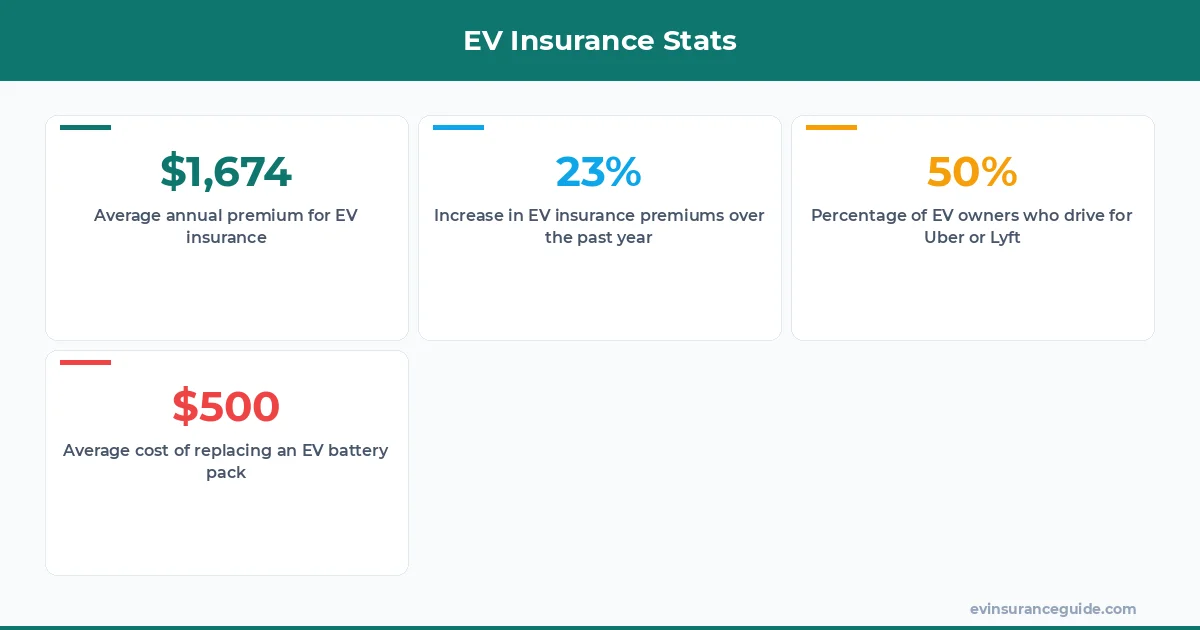

I'm sipping on a coffee at a charging station, watching a Tesla Model 3 charge up, when I overhear a conversation between two EV owners. They're discussing the ridiculous cost of insurance for their electric vehicles, especially since they drive for Uber and Lyft. One of them mentions that their premium increased by $500 after switching to a Rivian R1T. That's a pretty penny, if you ask me. Know what the kicker is? They're not alone. I've seen this happen to countless EV owners, and it's a trend that's only getting worse.

What's Driving Up the Cost of EV Insurance for Rideshare Drivers?

The main reason why EV insurance is so expensive for rideshare drivers is the high cost of replacement parts. For instance, a Tesla Model Y's battery pack can cost upwards of $10,000 to replace. That's a significant expense for insurance companies, which is then passed on to the driver. And let's not forget about the cost of labor - EVs often require specialized technicians, which can drive up repair costs. Sound familiar? It's a vicious cycle, and one that's leaving many EV owners feeling frustrated and financially strained.

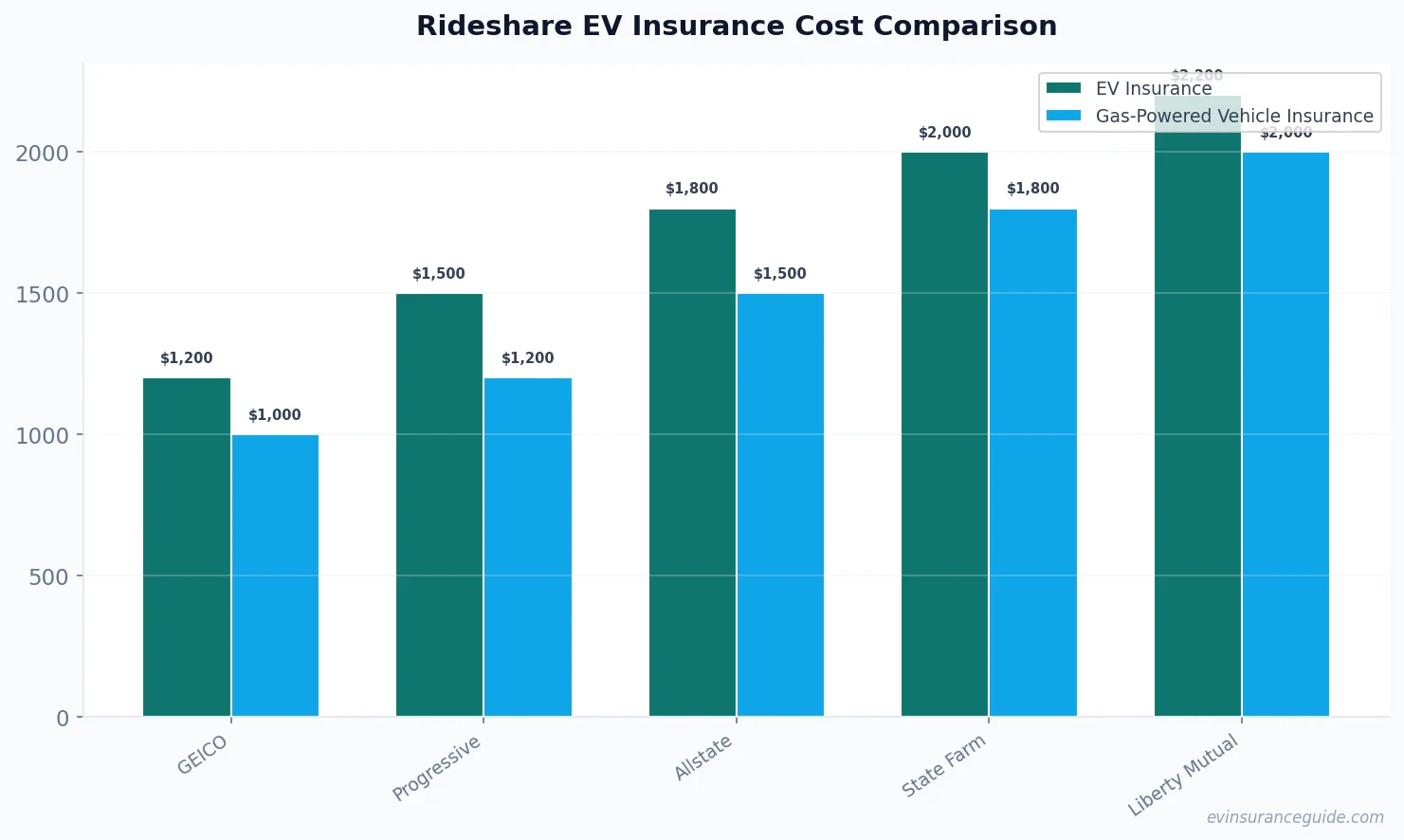

But here's the thing: not all insurance companies are created equal. Some, like GEICO and Progressive, offer more competitive rates for EV owners. For example, GEICO's EV insurance policy can cost as little as $1,200 per year, while Progressive's policy can start at around $1,500. Of course, these prices vary depending on your location, driving history, and other factors. But overall, it's clear that some companies are more willing to work with EV owners than others. Wild, right? You'd think that all insurance companies would be eager to jump on the EV bandwagon, but that's just not the case.

And then there's the issue of rideshare insurance. Companies like Uber and Lyft offer some level of coverage for their drivers, but it's often not enough. That's why many drivers are turning to third-party insurance companies to fill the gap. For instance, Allstate's rideshare insurance policy can cost around $20 per month, while State Farm's policy can cost around $30 per month. These policies can provide additional coverage for things like liability, collision, and comprehensive damage. But be warned: they can also come with some pretty steep premiums. Dead serious, I've seen some policies that cost upwards of $100 per month. That's a lot of money, especially for drivers who are already struggling to make ends meet.

EV Insurance: How Does It Compare to Gas-Powered Vehicle Insurance?

EV insurance is often compared to gas-powered vehicle insurance, but the two are not always apples to apples. For one thing, EVs tend to be more expensive to repair than gas-powered vehicles. This is because EVs have complex electrical systems and specialized parts, which can drive up repair costs. On the other hand, gas-powered vehicles have more straightforward mechanical systems, which can make them cheaper to repair. But here's the thing: EVs also tend to be safer than gas-powered vehicles. They have a lower center of gravity, which makes them less prone to rollover accidents. And they often come with advanced safety features, like automatic emergency braking and lane departure warning. So, while EV insurance may be more expensive, it's also often a better value. Know what I mean?

For example, let's say you own a Hyundai Ioniq 5 and drive for Uber. Your insurance premium might be higher than if you owned a gas-powered Honda Civic, but you'll also be getting a safer, more reliable vehicle. And let's not forget about the cost savings on fuel and maintenance - EVs are often cheaper to run than gas-powered vehicles. According to the US Department of Energy, charging an EV can cost as little as $3 to $5 per 100 miles, while driving a gas-powered vehicle can cost around $12 to $15 per 100 miles. That's a significant difference, especially for drivers who put a lot of miles on their vehicles.

But what about the environmental benefits? EVs produce zero tailpipe emissions, which makes them a more sustainable option than gas-powered vehicles. And with the rise of renewable energy sources, it's becoming increasingly possible to charge your EV with clean energy. That's a big deal, especially for drivers who are concerned about their carbon footprint. So, while EV insurance may be more expensive, it's also often a better value. You'll be getting a safer, more reliable vehicle that's also better for the environment.

5 Things You Need to Know About EV Insurance for Rideshare Drivers

First and foremost, you need to understand that EV insurance is not a one-size-fits-all solution. Different insurance companies offer different policies, and some may be more suited to your needs than others. For instance, if you drive a Tesla Model 3 and live in California, you may want to consider a policy that includes coverage for wildfires and earthquakes. On the other hand, if you drive a BMW iX and live in New York, you may want to consider a policy that includes coverage for snow and ice damage. The point is, you need to do your research and find a policy that fits your specific needs.

Second, you need to understand that EV insurance is often more expensive than gas-powered vehicle insurance. This is because EVs tend to be more expensive to repair, and they often require specialized parts and labor. But here's the thing: EVs also tend to be safer and more reliable than gas-powered vehicles. So, while your insurance premium may be higher, you'll also be getting a better value. Sound like a fair trade-off? I think so.

Third, you need to understand that rideshare insurance is a must-have for any driver who works for Uber or Lyft. These companies offer some level of coverage, but it's often not enough. That's why many drivers are turning to third-party insurance companies to fill the gap. For instance, Allstate's rideshare insurance policy can provide additional coverage for things like liability, collision, and comprehensive damage. And with the rise of gig economy jobs, it's becoming increasingly important for drivers to have adequate insurance coverage.

Fourth, you need to understand that EV insurance is not just about the vehicle itself - it's also about the driver. Insurance companies take into account your driving history, your credit score, and other factors when determining your premium. So, if you have a poor driving record or a low credit score, you may want to consider working on those issues before applying for EV insurance. That's just good sense, if you ask me.

Fifth, you need to understand that EV insurance is constantly evolving. New companies are entering the market, and existing companies are updating their policies to reflect the changing needs of EV owners. For instance, some companies are now offering policies that include coverage for charging station accidents or electrical system failures. So, it's essential to stay informed and keep up-to-date on the latest developments in the EV insurance industry.

Pro tip: Always read the fine print before signing up for an EV insurance policy. You want to make sure you understand what's covered and what's not, as well as any exclusions or limitations that may apply.

Why Is EV Insurance So Expensive for Rideshare Drivers, Anyway?

Let's be honest - EV insurance is expensive, and it's not just because of the cost of replacement parts. There are a lot of factors at play here, from the complexity of EV systems to the rising cost of labor. But what really gets my goat is that some insurance companies are taking advantage of EV owners. They're charging exorbitant premiums without providing adequate coverage or support. That's just not right, if you ask me. EV owners deserve better, and it's time for insurance companies to step up their game.

For example, I've seen some insurance companies charging EV owners upwards of $2,000 per year for a policy that doesn't even include comprehensive coverage. That's outrageous, especially when you consider that gas-powered vehicle insurance can cost as little as $800 per year. It's like they're punishing EV owners for choosing a more sustainable option. But here's the thing: it's not all bad news. There are some insurance companies out there that are genuinely trying to help EV owners. They're offering competitive rates, comprehensive coverage, and excellent customer service. So, if you're an EV owner, don't give up hope. There are options out there, and it's worth doing your research to find the best one for your needs.

Myth-Busting: EV Insurance Edition

One of the biggest myths about EV insurance is that it's always more expensive than gas-powered vehicle insurance. But that's just not true. While EV insurance can be more expensive, it's not always the case. In fact, some insurance companies are now offering competitive rates for EV owners, especially those who drive for Uber or Lyft. For instance, Progressive's EV insurance policy can cost as little as $1,200 per year, while GEICO's policy can start at around $1,500. That's not much more than gas-powered vehicle insurance, if you ask me.

Another myth is that EV insurance is only for wealthy people who can afford expensive vehicles. But that's not true either. EVs are becoming increasingly affordable, and many models are now priced competitively with gas-powered vehicles. For example, the Hyundai Ioniq 5 starts at around $30,000, while the Tesla Model 3 starts at around $35,000. That's not much more than a gas-powered Honda Civic or Toyota Corolla, if you ask me. And with the cost savings on fuel and maintenance, EVs can actually be a more affordable option in the long run.

FAQs

#### What is the average cost of EV insurance for rideshare drivers?

The average cost of EV insurance for rideshare drivers can vary depending on several factors, including the type of vehicle, the driver's location, and their driving history. However, according to some estimates, the average cost of EV insurance for rideshare drivers can range from $1,500 to $3,000 per year.

#### How does EV insurance differ from gas-powered vehicle insurance?

EV insurance differs from gas-powered vehicle insurance in several ways. For one thing, EVs tend to be more expensive to repair, which can drive up insurance costs. On the other hand, EVs are often safer and more reliable than gas-powered vehicles, which can reduce insurance costs.

#### What are some tips for reducing the cost of EV insurance?

Some tips for reducing the cost of EV insurance include shopping around for different policies, improving your driving record, and maintaining a good credit score. You can also consider installing safety features like anti-theft devices or dash cams, which can help reduce your premium.

#### Can I get a discount on my EV insurance if I drive for Uber or Lyft?

Yes, some insurance companies offer discounts for drivers who work for Uber or Lyft. For example, Allstate's rideshare insurance policy can provide a discount of up to 10% for drivers who work for these companies.

#### What are some of the best insurance companies for EV owners?

Some of the best insurance companies for EV owners include GEICO, Progressive, and Allstate. These companies offer competitive rates, comprehensive coverage, and excellent customer service.

#### How do I know if I need EV insurance?

If you own an EV and drive for Uber or Lyft, you likely need EV insurance. However, it's always a good idea to check with your insurance company to see what type of coverage you need and how much it will cost.

#### What are some common exclusions or limitations in EV insurance policies?

Some common exclusions or limitations in EV insurance policies include coverage for charging station accidents, electrical system failures, or damage to specialized parts. It's essential to read the fine print and understand what's covered and what's not before signing up for a policy.

Well, actually, I think that's all the questions for now. But let me sum up - EV insurance is a complex and often confusing topic, but it's essential for any EV owner who drives for Uber or Lyft. By doing your research and shopping around for different policies, you can find the best coverage for your needs and budget.

Stay charged and stay covered! — Alex