Buying insurance for your brand new Tesla Model 3 can be a real kick in the wallet - it's like paying for a whole other car... every year. Sound familiar? The reason why is EV insurance so expensive is a question on every EV owner's mind. I've seen quotes ranging from $1,800 to $3,500 per year for a Tesla Model Y, depending on the insurance provider and location. That's a significant chunk of change, especially considering the car itself might cost around $50,000.

What's Driving Up EV Insurance Costs?

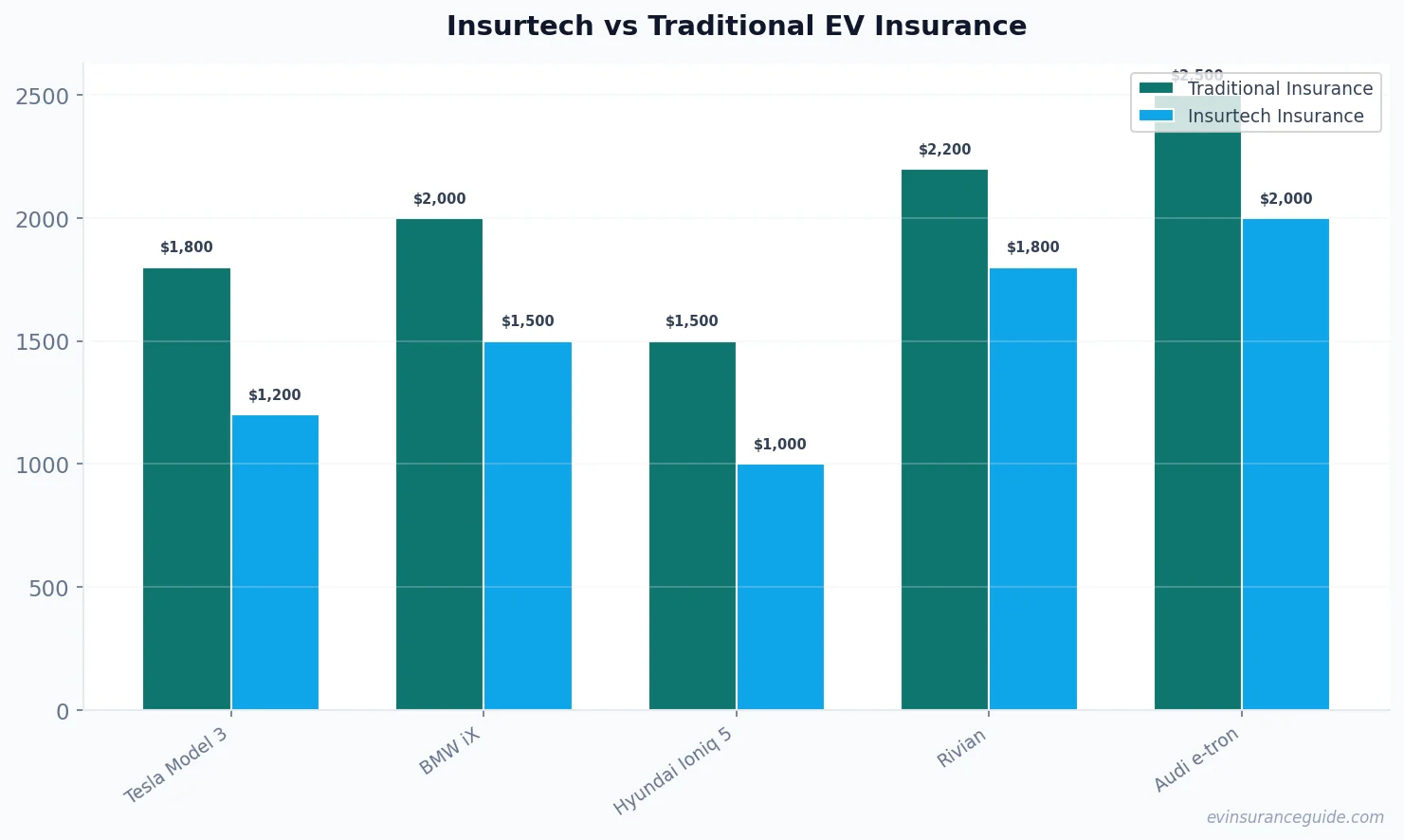

The main culprit behind the high cost of EV insurance is the lack of data on these vehicles. Insurers are still trying to figure out how much it costs to repair or replace an EV, and until they have more data, they're erring on the side of caution - which means higher premiums for you. Know what the kicker is? Some traditional insurers are charging even more for EVs than they are for gas-guzzling SUVs. For example, a friend of mine who owns a BMW iX was quoted $2,500 per year by a traditional insurer, while his neighbor's gas-powered BMW X5 was quoted at $1,800 per year. That one stung.

But here's the thing: insurtech companies like Lemonade and Root are shaking things up. They're using AI and machine learning to better assess risk and offer more competitive premiums. I've seen quotes from Lemonade for as low as $1,200 per year for a Hyundai Ioniq 5, which is significantly lower than what traditional insurers are offering. And the best part? These insurtech companies are often more transparent about their pricing and more flexible with their policies.

A Story of Two Insurers: Traditional vs Insurtech

I spoke to a Rivian owner who had a wild experience with a traditional insurer. They were quoted $3,000 per year, but when they tried to file a claim, the insurer lowballed them and tried to repair the car with cheap, non-OEM parts. The owner ended up switching to an insurtech company called Root, which offered them a lower premium and better coverage. Now, they're paying $1,800 per year and getting better service to boot. Wild, right? The difference in pricing and service between traditional and insurtech insurers is staggering.

As someone who's been in the industry for a while, I can tell you that traditional insurers are starting to take notice of the insurtech disruption. They're trying to modernize their own systems and offer more competitive premiums, but it's an uphill battle. The truth is, insurtech companies are more agile and better equipped to handle the unique needs of EV owners. They're offering features like usage-based insurance, which can save you money if you don't drive much, and they're often more willing to work with you to customize your policy.

EV Insurance Costs: A Tale of Two Worlds

Buying an EV can be a costly endeavor, but the insurance costs can be just as bad. Why is EV insurance so expensive, anyway? The answer lies in the fact that EVs are still a relatively new phenomenon, and insurers are struggling to keep up. They're using outdated models to assess risk, which means they're often overcharging EV owners. But insurtech companies are changing the game by using more advanced data analytics and AI-powered risk assessment tools. For example, a study by the National Association of Insurance Commissioners found that insurtech companies are using data from sources like vehicle sensors and driving apps to offer more personalized premiums.

Pro tip: If you're shopping for EV insurance, make sure to ask about usage-based options. These can save you big time if you don't drive much. I've seen quotes from companies like Metromile that offer pay-per-mile insurance starting at just $29 per month.

But what about the cost of repairing or replacing an EV? That's where things get really interesting. Because EVs have fewer moving parts than gas-powered cars, they're often cheaper to maintain and repair. However, the high cost of replacement batteries can be a major factor in insurance costs. Insurtech companies are taking a more nuanced approach to assessing this risk, which is why they're often able to offer lower premiums.

Honestly, Traditional Insurers Are Overpriced

I'm gonna say it: traditional insurers are ripping off EV owners. They're charging way too much for coverage, and they're not offering the kind of personalized service that insurtech companies are. Why is EV insurance so expensive, again? It's because traditional insurers are stuck in the past and refusing to adapt to the changing needs of EV owners. They're using outdated models and overcharging for coverage, which means you're paying way too much for your premium. I've seen quotes from traditional insurers that are as high as $4,000 per year for a Tesla Model S, which is just outrageous.

5 Key Statistics That Will Change Your Mind About EV Insurance

Here are five key statistics that show why insurtech companies are the way to go for EV owners:

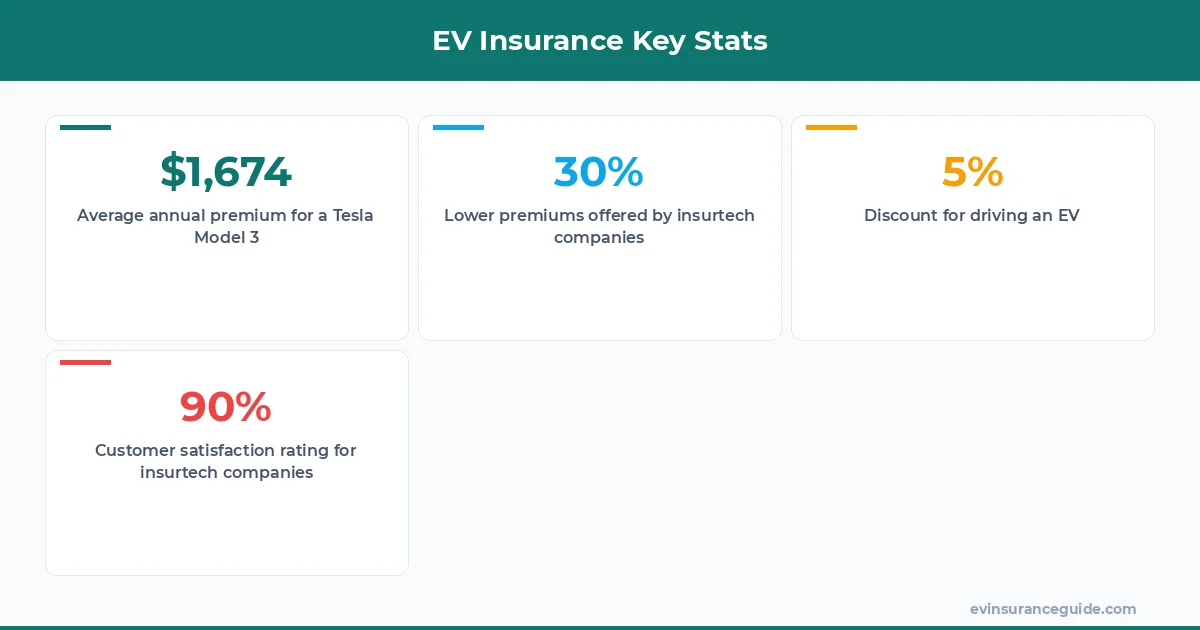

- 1. Lower premiums: Insurtech companies are offering premiums that are up to 30% lower than traditional insurers.

- 2. Better coverage: Insurtech companies are offering more comprehensive coverage options, including features like roadside assistance and rental car coverage.

- 3. More transparency: Insurtech companies are being more transparent about their pricing and policy terms, which means you know exactly what you're getting.

- 4. Faster claims processing: Insurtech companies are using AI-powered claims processing, which means you get your money faster.

- 5. Higher customer satisfaction: Insurtech companies are consistently rated higher in customer satisfaction surveys, which means you're more likely to be happy with your insurer.

FAQs

#### What is the average cost of EV insurance?

The average cost of EV insurance can range from $1,500 to $3,500 per year, depending on the insurer and your location. However, insurtech companies are offering premiums that are significantly lower, with some starting at just $1,000 per year.

#### Do all insurers offer EV-specific policies?

No, not all insurers offer EV-specific policies. However, most major insurers are starting to offer specialized EV policies, which can provide better coverage and lower premiums.

#### Can I get a discount for driving an EV?

Yes, some insurers are offering discounts for driving an EV. These discounts can range from 5% to 10% off your premium, depending on the insurer and your location.

#### How do I choose the best EV insurer for me?

Choosing the best EV insurer for you depends on your specific needs and circumstances. Consider factors like premium cost, coverage options, and customer service when making your decision.

#### What is the difference between insurtech and traditional insurance?

Insurtech companies are using advanced data analytics and AI-powered risk assessment tools to offer more personalized and competitive premiums. Traditional insurers, on the other hand, are often stuck in the past and refusing to adapt to the changing needs of EV owners.

#### Are insurtech companies reliable?

Yes, insurtech companies are reliable and often have higher customer satisfaction ratings than traditional insurers. They're also often more transparent about their pricing and policy terms, which means you know exactly what you're getting.

And that's a wrap, folks. Go get yourself a better quote. You deserve it. — Alex