I was sipping coffee at a charging station when I overheard a conversation between two EV owners, Rachel and Mike, discussing their insurance experiences. Rachel mentioned that her Tesla Model 3 was totaled in an accident, and she was shocked to find out that her insurance payout was lower than she expected. Mike shared a similar story about his BMW iX, and they both wondered why EV insurance is so expensive. Sound familiar? That got me thinking - what's the deal with total loss and EV insurance?

OK So Here's the Deal With Total Loss

When an EV is totaled, the insurance company will typically pay out the actual cash value (ACV) of the vehicle, which is the market value of the EV at the time of the accident. But here's the thing - the ACV can be lower than the purchase price of the EV, especially if it's a newer model. For example, a brand new Tesla Model Y can cost around $50,000, but its ACV might be around $40,000 after just a few months of ownership. Know what the kicker is? The insurance company won't pay out the full purchase price, even if you've only had the EV for a short time. That one stung for Rachel, who had only owned her Tesla for six months before it was totaled.

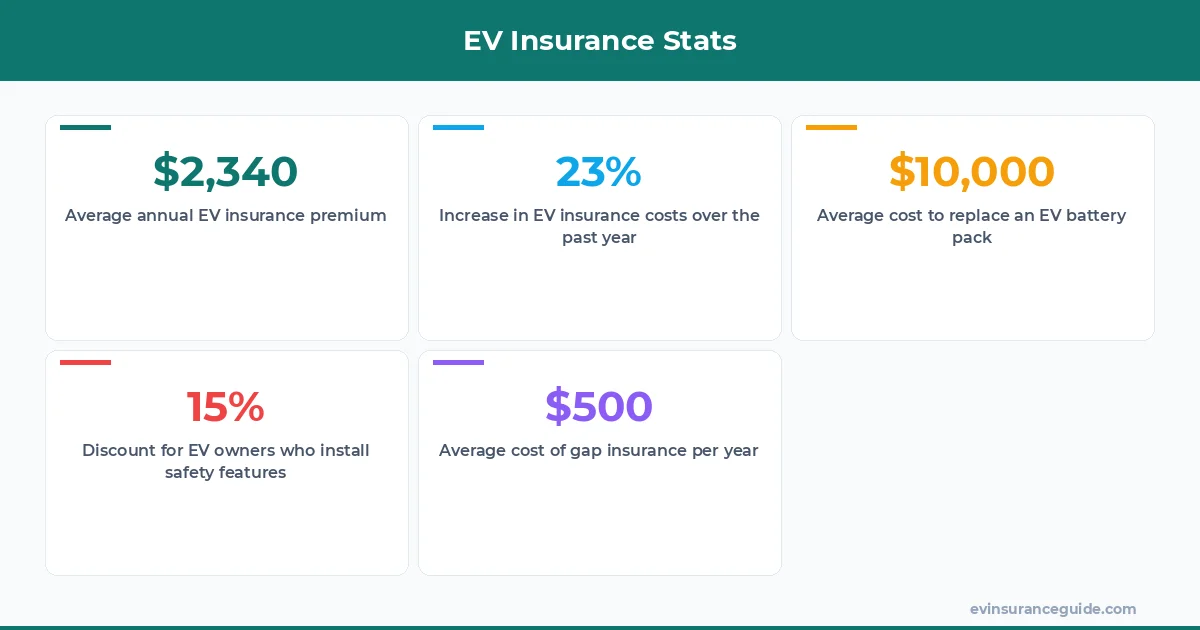

The cost of EV insurance can vary widely depending on several factors, including the make and model of the EV, the driver's location, and their driving history. On average, EV insurance can cost between $1,500 to $3,000 per year, with some companies like Geico and Progressive offering more competitive rates. But why is EV insurance so expensive? One reason is that EVs are often more expensive to repair or replace than gas-powered vehicles. For instance, the battery pack in a Hyundai Ioniq 5 can cost upwards of $10,000 to replace, which can drive up insurance costs.

A Story of Total Loss - What Happened to Rachel's Tesla

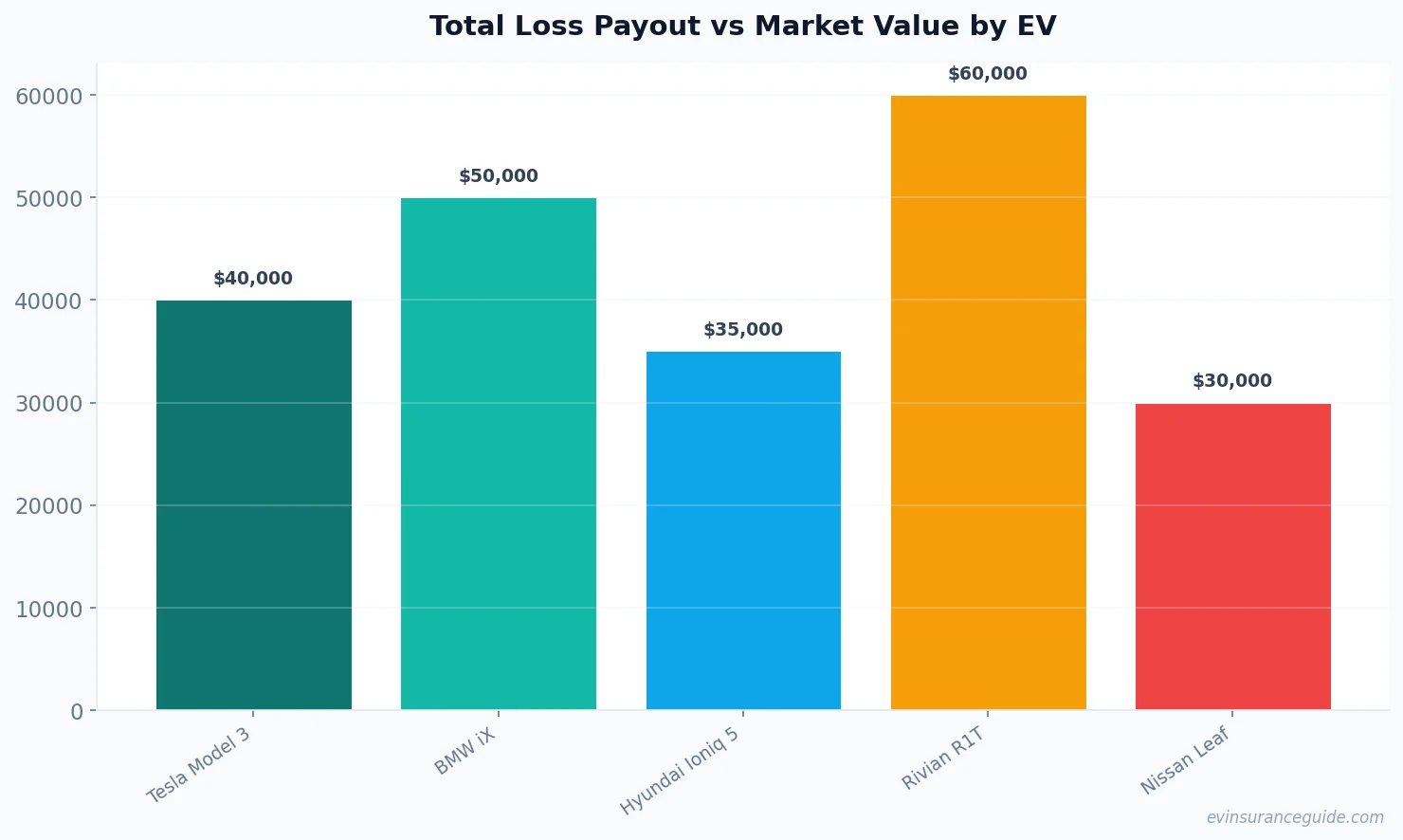

Rachel's story is a great example of how total loss can work for EVs. She had purchased her Tesla Model 3 just a few months before the accident, and she had opted for a comprehensive insurance policy that covered damage to her vehicle. When the accident happened, Rachel was relieved to find out that her insurance company would cover the cost of repairs. But when the repair estimate came in, Rachel was shocked to find out that her Tesla was totaled. The insurance company offered her a payout of $38,000, which was lower than she expected. Rachel was disappointed, but she eventually accepted the offer and used the payout to purchase a new EV.

The whole experience left Rachel wondering why EV insurance is so expensive. She had done her research and compared rates from different insurance companies, but she still felt like she was overpaying for her coverage. And she's not alone - many EV owners are paying high premiums for their insurance, often without fully understanding what they're getting. Wild, right? It's like, you're already paying a premium for the EV itself, and then you've got to pay even more for insurance. But is it worth it? That's a topic for another time.

What's the Real Cost of Total Loss - Can You Afford It?

The cost of total loss can be significant, especially if you're not prepared for it. Let's say you own a Rivian R1T, which can cost upwards of $70,000. If you're involved in an accident and your Rivian is totaled, you could be looking at a payout of $60,000 or less, depending on the ACV of your vehicle. That means you could be out of pocket for thousands of dollars, which can be a significant financial burden. And that's not even considering the cost of replacing your EV, which can be even higher. So, can you afford the real cost of total loss? Probably not, if you're not prepared.

Pro tip: Make sure you understand what's covered in your insurance policy, including the ACV of your EV. You don't want to be caught off guard if you're involved in an accident and your EV is totaled. Consider purchasing gap insurance, which can help cover the difference between the ACV of your EV and the amount you still owe on your loan.

The cost of gap insurance can vary depending on the insurance company and the make and model of your EV. On average, gap insurance can cost between $20 to $50 per year, which is a small price to pay for the added protection. And speaking of protection, it's essential to have the right insurance coverage for your EV. Why is EV insurance so expensive? One reason is that EVs are often more expensive to repair or replace than gas-powered vehicles. But with the right coverage, you can protect yourself from financial loss in the event of an accident.

How Much Will You Get Paid - The Total Loss Payout

When it comes to total loss, the payout can vary widely depending on the insurance company and the make and model of your EV. On average, the payout for a totaled EV can range from $30,000 to $60,000, depending on the ACV of the vehicle. But what if you owe more on your loan than the payout amount? That's where gap insurance comes in - it can help cover the difference between the ACV of your EV and the amount you still owe on your loan. For example, let's say you owe $50,000 on your loan, but the payout for your totaled EV is only $40,000. Gap insurance can help cover the remaining $10,000, which can be a significant financial burden.

Warning - Don't Get Caught Off Guard by Hidden Fees

When it comes to total loss, there are often hidden fees and costs that can add up quickly. For example, some insurance companies may charge a fee for towing or storage, which can range from $100 to $500. And then there's the cost of replacing your EV, which can be even higher. So, how can you avoid getting caught off guard by these hidden fees? The key is to understand what's covered in your insurance policy and to ask questions if you're not sure. Don't be afraid to negotiate with your insurance company, either - they may be willing to waive certain fees or costs if you're a loyal customer.

5 Things You Need to Know About Total Loss

Here are five things you need to know about total loss and EV insurance:

- 1. The ACV of your EV can be lower than the purchase price, especially if it's a newer model.

- 2. Gap insurance can help cover the difference between the ACV of your EV and the amount you still owe on your loan.

- 3. The cost of EV insurance can vary widely depending on several factors, including the make and model of the EV and the driver's location.

- 4. Why is EV insurance so expensive? One reason is that EVs are often more expensive to repair or replace than gas-powered vehicles.

- 5. The payout for a totaled EV can range from $30,000 to $60,000, depending on the ACV of the vehicle.

FAQs

#### What is total loss?

Total loss refers to the situation when an EV is damaged beyond repair and is considered a total loss by the insurance company. In this case, the insurance company will typically pay out the ACV of the vehicle, which can be lower than the purchase price.

#### How much does EV insurance cost?

The cost of EV insurance can vary widely depending on several factors, including the make and model of the EV, the driver's location, and their driving history. On average, EV insurance can cost between $1,500 to $3,000 per year.

#### What is gap insurance?

Gap insurance is a type of insurance that can help cover the difference between the ACV of your EV and the amount you still owe on your loan. This can be a valuable addition to your insurance policy, especially if you're financing your EV.

#### Can I negotiate with my insurance company?

Yes, you can negotiate with your insurance company to get a better deal on your EV insurance. Be sure to ask questions and understand what's covered in your policy, and don't be afraid to shop around for quotes from different insurance companies.

#### How much will I get paid if my EV is totaled?

The payout for a totaled EV can vary widely depending on the insurance company and the make and model of your EV. On average, the payout can range from $30,000 to $60,000, depending on the ACV of the vehicle.

#### What are some tips for buying EV insurance?

Some tips for buying EV insurance include shopping around for quotes from different insurance companies, understanding what's covered in your policy, and considering the cost of gap insurance. It's also essential to read reviews and ask for referrals from friends or family members who have purchased EV insurance.

And that's not all - there are many other factors to consider when buying EV insurance. For example, some insurance companies may offer discounts for certain safety features or driving habits. Others may have more comprehensive coverage options, such as roadside assistance or rental car coverage. So, be sure to do your research and compare quotes from different insurance companies to find the best deal for your needs.

That's my two cents. Take it or leave it — but I hope it helps. — Alex