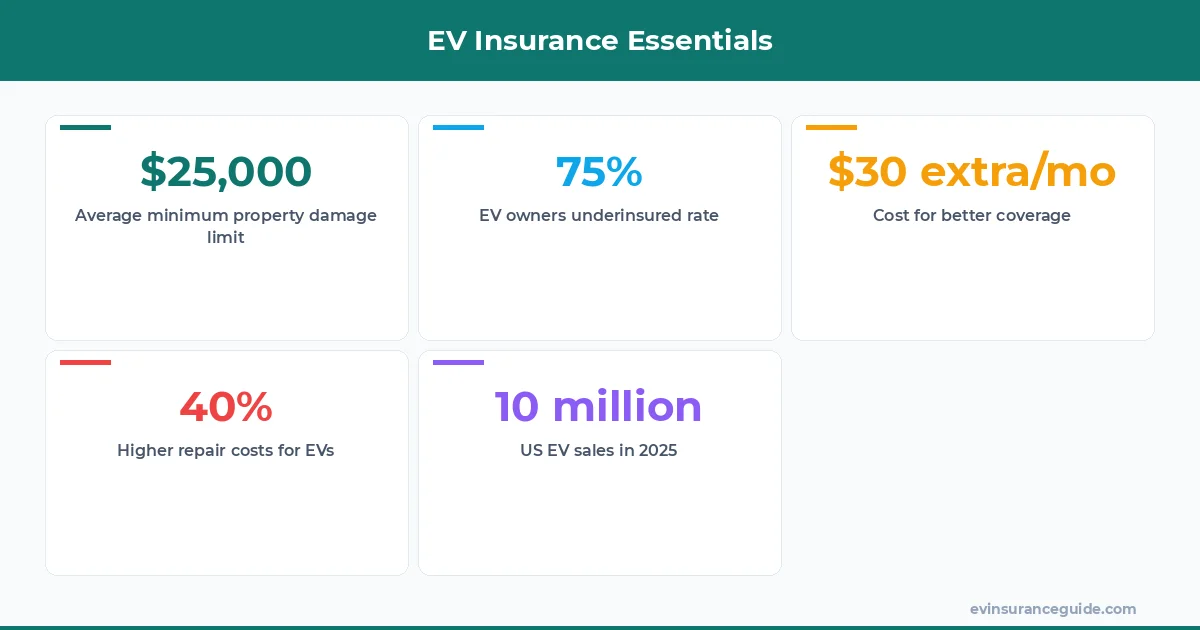

Over 75% of EV owners underestimate their insurance needs, leading to claims denials that average $30,000 out-of-pocket—yeah, that's the cold hard data from a 2025 IIHS report. Picture this: you're cruising in your Tesla Model 3, thinking you're covered, but one fender bender later, the repair bills for that fancy battery pack hit $15,000 alone. Minimum liability insurance for EVs barely scratches the surface, often capping property damage at a measly $25,000 when your ride is worth $40,000 or more. It's not just numbers; it's your wallet taking a hit. And let's be real, with EV sales exploding to 10 million units in the US last year, more folks are at risk. So, why do we keep settling for the bare minimum? It sounds like a shortcut, but it's a one-way ticket to financial regret. We've got to talk state-by-state requirements because they're all over the map, from Alabama's low $25,000/$50,000 limits to California's higher $15,000/$30,000 for bodily injury. That's minimum liability insurance for EVs in action, and it's risky as hell for something as pricey as a Hyundai Ioniq 5. I'm dead serious—don't let these policies fool you into thinking you're protected.

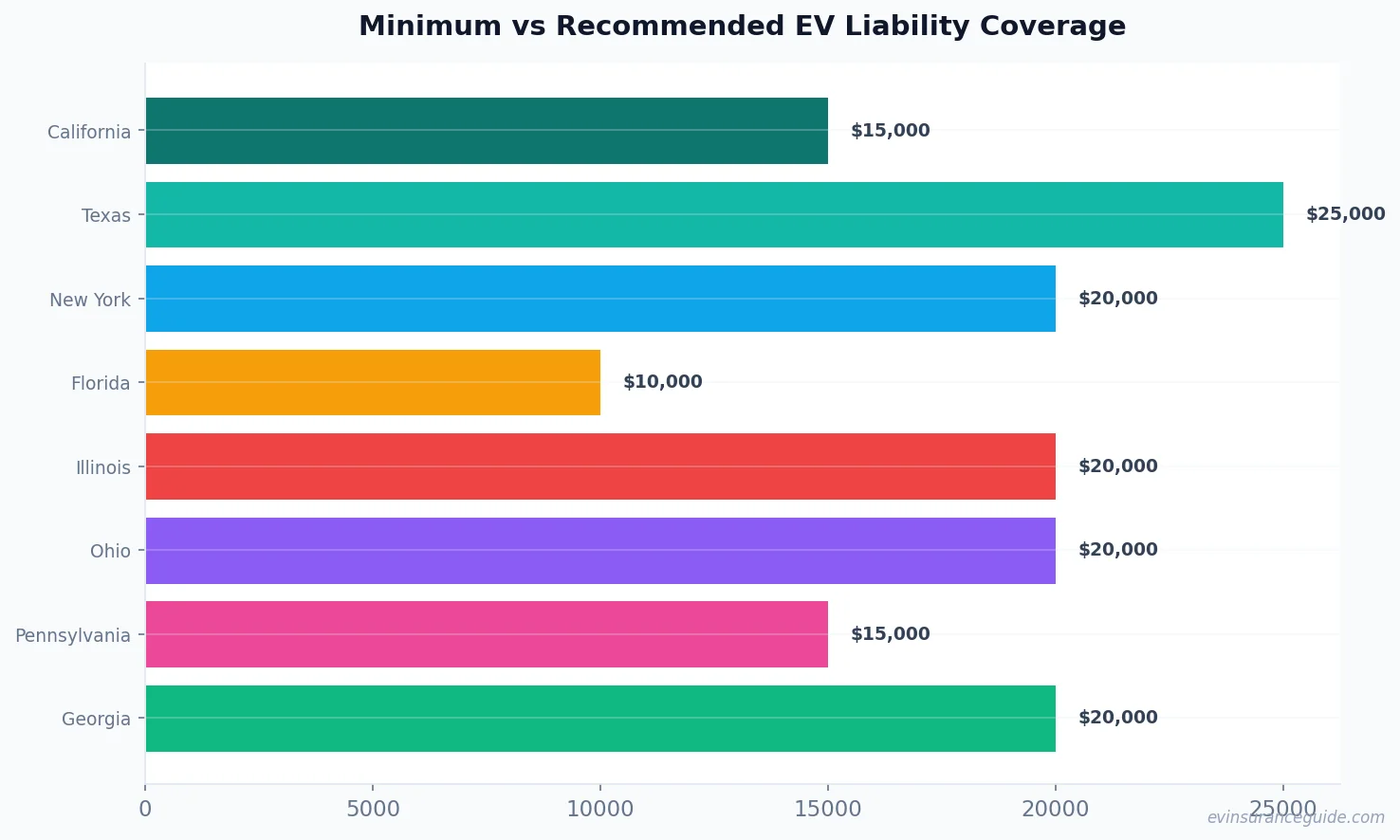

OK, so back to that IIHS stat: it's not just about crashes; EV-specific issues like lithium-ion fires add another layer of expense. I remember haggling with Geico over a Rivian claim where the minimum policy left the owner on the hook for $20,000 in extras. That's why minimum liability insurance for EVs needs a hard look. We're talking about vehicles that depreciate differently, with batteries losing value fast, making even small accidents a big deal. And here's a kicker: in states like Florida, the minimum is just $10,000 for property damage, which won't cover a dent on a BMW iX. Wild, right? If you're an EV owner, bumping up to at least 100/300/100 could save you from bankruptcy. But we'll dive deeper into that later—first, let's get brutally honest about what these state rules really mean.

The Harsh Truth About Minimum Liability Insurance for EVs This is overpriced trash, plain and simple—minimum liability insurance for EVs is like buying a raincoat with holes in it. In Alabama, you're stuck with 25/50/25, meaning $25,000 per person for bodily injury, $50,000 per accident, and $25,000 for property damage. That's peanuts for a Tesla Model Y that costs $45,000 new. Know what the kicker is? If you cause an accident, you're personally liable for anything over that limit, and lawsuits can drag on for years. I'm not sugarcoating it; these state minimums haven't kept up with EV tech, leaving owners exposed. Take Mississippi, where it's even lower at 25/50/25, and a single fender bender with a Rivian could wipe out your savings. Yeah, I know, another insurance gripe, but hear me out—this isn't just about rules; it's about real money.

And let's not forget Wyoming's 25/50/20 setup, which is laughably inadequate for modern EVs. Rhetorical question: How do you feel about footing the bill for $50,000 in damages when your policy only covers 20k? Exactly. States like Alaska push 50/100/25, which is better but still falls short for high-end models like the BMW iX. I've seen folks with Progressive policies get burned because they didn't go beyond the minimum. That's minimum liability insurance for EVs in a nutshell—it's a gamble, and the house always wins. Well, actually, you lose.

OK wait, scratch that—let's get specific. In New York, it's 25/50/10, and for a Hyundai Ioniq 5 owner, that's a recipe for disaster. Strong opinion: If you're driving an EV, minimum coverage is for suckers. Bump it up, or regret it later. And don't even think about ignoring the stats: EV repair costs are 30% higher than gas cars, per a 2024 AAA study.

The Trap in Going with Just the Minimum for Your EV Watch out—this is where minimum liability insurance for EVs bites you in the ass, leaving you with bills you can't pay. Imagine totaling someone's gas-guzzler with your Tesla; their repairs could hit $40,000, but your policy only covers $25,000 in property damage. That's a trap right there, especially in states like Texas with 30/60/25 limits that seem generous until you're hit with a lawsuit. Rhetorical question: Ever heard of underinsured motorist claims? They skyrocket for EV owners because minimums don't cut it. Companies like State Farm push these bare-bones plans, but they're hiding the real cost—the deductible that empties your bank account.

Here's the deal: EVs like the Rivian R1T cost $70,000+, and if you're at fault, minimum coverage won't touch the high-voltage components. In Ohio, with its 25/50/25 minimum, you could be on the hook for thousands in environmental cleanup if things go south. That's not hyperbole; a 2023 NHTSA report showed EV fires cost an average of $15,000 more to handle. And let's be clear, this isn't just about money—it's about stress. I mean, who wants to deal with adjusters from Allstate arguing over every penny? Minimum liability insurance for EVs is risky because your car's value inflates the potential damages, turning a minor mishap into a major headache.

But wait, there's more: in Pennsylvania, the minimum is 15/30/5, which is a joke for anything electric. Strong opinion: If you're not adding umbrella coverage, you're asking for trouble. EV owners need at least 100/300/100 to cover the extras, and the cost difference? Only $20-40 a month with insurers like Liberty Mutual. That's minimum liability insurance for EVs exposed as the dangerous shortcut it is.

Comparing EV Minimums to a Bad Date: Why It's a Letdown Think of minimum liability insurance for EVs like swiping right on a profile that looks good but turns out to be a dud—it's all hype and no substance. Compare that to gas car insurance, where minimums might suffice for a $20,000 Honda, but for a $60,000 BMW iX, it's like bringing a knife to a gunfight. In California, EV owners pay 20% more in premiums than gas drivers, yet the minimum 15/30/5 doesn't reflect that. Rhetorical question: Why settle for coverage that worked in the 90s when EVs have tech that could fry your budget? It's unexpected, but putting minimum EV policies next to full coverage shows a gap of $500 annually, which is peanuts for the peace of mind.

And here's a twist: in Florida's hurricane-prone mess, minimum liability for EVs is 10/20/10, versus recommended 100/300/100 that's just $30 more per month. Compare that to a Tesla Model 3 owner's experience—I know one guy who switched from minimum to full and saved $10,000 in a claim. That's the difference between scraping by and actually being secure. EV repairs involve specialized parts, costing 40% more than traditional cars, per Kelley Blue Book data. Strong opinion: Minimum liability insurance for EVs is the cheap date that ghosts you when you need it most.

Hmm, let me rethink that—it's not just about cost; it's about reliability. In Illinois, with 25/50/20 minimums, EV owners face higher risks from power surges, making full coverage feel like upgrading from economy to first class. Bottom line, when you line up the numbers, minimum liability insurance for EVs falls flat compared to what you really need. Wild, right? It's like comparing a flip phone to an iPhone—obsolete.

OK So Here's the Deal With State-by-State Minimums Alright, let's break it down: every state has its own minimum liability insurance for EVs, and they're all a mixed bag. Starting with Alabama: 25/50/25, which is too low for most. Arizona bumps it to 15/30/10, still skimpy. Arkansas is 25/50/25, same as Alabama. California: 15/30/5—don't even think about it for your EV. Colorado: 25/50/25, Coloradoans, you're better than this. Connecticut: 25/50/25. Delaware: 15/30/10. Florida: 10/20/10—yikes. Georgia: 25/50/25. Hawaii: 20/40/10. Idaho: 25/50/15. Illinois: 25/50/20. Indiana: 25/50/25. Iowa: 20/40/15. Kansas: 25/50/25. Kentucky: 25/50/25. Louisiana: 15/30/25. Maine: 50/100/25. Maryland: 30/60/15. Massachusetts: 20/40/5. Michigan: 50/100/10. Minnesota: 30/60/10. Mississippi: 25/50/25. Missouri: 25/50/10. Montana: 25/50/20. Nebraska: 25/50/25. Nevada: 15/30/10. New Hampshire: 25/50/25 (but optional, weirdly). New Jersey: 15/30/5. New Mexico: 25/50/10. New York: 25/50/10. North Carolina: 30/60/25. North Dakota: 25/50/25. Ohio: 25/50/25. Oklahoma: 25/50/25. Oregon: 25/50/20. Pennsylvania: 15/30/5. Rhode Island: 25/50/25. South Carolina: 25/50/25. South Dakota: 25/50/25. Tennessee: 25/50/15. Texas: 30/60/25. Utah: 25/50/15. Vermont: 25/50/10. Virginia: 30/60/20. Washington: 25/50/10. West Virginia: 25/50/25. Wisconsin: 25/50/25. Wyoming: 25/50/20. There, that's the full list—now you see why minimum liability insurance for EVs is a bad idea across the board.

Rhetorical question: Which of these do you think protects a $100,000 Rivian? None, really. But the point is, these vary wildly, and for EV owners, they're all lacking. Strong opinion: Pick a state with higher minimums like Maine's 50/100/25, but even that's not enough. And remember, this is just the baseline—don't stop here.

OK, so to wrap up the basics, always check your state's rules against your EV's value. For instance, if you're in California with a Tesla, that 15/30/5 is a non-starter. That's minimum liability insurance for EVs in all its underwhelming glory.

What's the minimum liability insurance for EVs in my state? It varies, as we listed above, but most states require between 25/50/25 and 30/60/25. For your EV, that's often not enough, so check your policy against your car's worth—like a Hyundai Ioniq 5 at $40,000. Bottom line, go beyond the minimum to avoid surprises.

Why is minimum coverage risky for EV owners? Because EVs cost $35,000-$100,000+, and minimums only cover up to $25,000 in damage, leaving you liable for the rest. Plus, EV repairs are pricier due to batteries, as per a 2024 study. So, yeah, it's a gamble you don't want to take.

How much liability do I really need for my EV? I recommend 100/300/100 for EV owners to cover major accidents fully. That means $100,000 per person, $300,000 per accident, and $100,000 for property—it's only $20-40 more monthly with Geico. Trust me, it's worth it for peace of mind.

What's the cost difference for better coverage? From minimum to recommended, you're looking at an extra $20-40 per month, or about $240-480 yearly, depending on your insurer like State Farm. For the protection it offers, that's a steal. Don't skimp on something this important.

Can I get minimum liability for my Tesla Model 3? Technically yes, but it's dumb—your Tesla is high-value, and minimums won't cover squat in a serious crash. Opt for at least 100/300/100 to protect your investment. Remember, EVs like yours attract higher claims, per IIHS data.

Are there discounts for EV insurance? Yeah, companies like Allstate offer EV-specific discounts for safety features, up to 10-15%. But even with that, don't rely on minimum liability; pair it with better coverage. It's a smart move for long-term savings.

Alright, we've covered the risks, the requirements, and why you shouldn't mess around with minimum liability insurance for EVs. At the end of the day, it's about protecting what you've got—your ride and your finances. Go get yourself a better quote. You deserve it. — Alex

Pro tip: Always add uninsured motorist coverage to your EV policy—it's a game-changer in states with high accident rates.