OK so someone DM'd me this question the other day — 'Alex, what's really gonna happen with EV insurance in the next few years? I've got a Tesla Model 3 and I'm worried about my premiums skyrocketing.' Yeah, I get it. We've all been there, staring at our policy statements like they're ancient hieroglyphs, trying to figure out if that next charge is justified. But let's cut to the chase: the future of EV insurance is wilder than you think, blending tech, data, and some corporate shakeups that could slash your costs or flip the script entirely. Take usage-based pricing, for instance — it's not just a buzzword anymore; by 2026, it's poised to become the default for EVs, meaning your driving habits could directly dictate what you pay, instead of that blanket fee we've all grumbled about. And that's just the start. With autonomous driving on the rise, liability might shift from you to the manufacturer, like Tesla or BMW, potentially turning your policy into a breeze. Or consider battery-as-a-service models from companies like Hyundai, which could erase those nightmare replacement costs for Ioniq 5 owners. We're talking real changes that could mean lower premiums by 2027-2030, but only if you play your cards right. EV-only insurers are gunning for market share, using connected car data to adjust rates in real time — think of it as your Rivian snitching on your speed to save you cash. I'm dead serious; this isn't sci-fi, it's happening, and it's gonna redefine how we insure our rides. So, if you're eyeing that new EV, knowing the future of EV insurance could be the difference between a steal and a rip-off. Wild, right? Let's break it down, because I've got stories from my days filing claims that prove these trends aren't just hype — they're game-changers for your wallet.

OK So Here's the Deal With Usage-Based Pricing Taking Over Usage-based pricing for EVs? It's about time. No more paying through the nose just for owning a Tesla Model 3 when you're barely driving it. By 2026, this is gonna be the norm, with companies like Progressive and Allstate pushing apps that track your mileage, speed, and even braking patterns to set your premium. Imagine saving 15-20% off your annual rate if you're a light driver — that's real money, like dropping from $1,800 to $1,440 for a BMW iX owner in urban areas. But here's the rub: if you're hammering the accelerator like a maniac, your premium could spike by 10-15%. Know what the kicker is? This future of EV insurance means safer drivers win big, which is music to my ears after arguing with adjusters over unnecessary claims.

And don't think this is one-size-fits-all. For a Hyundai Ioniq 5, you might see even steeper discounts if your usage data shows eco-friendly habits, like regenerative braking or optimized routes. That's gonna push traditional insurers to adapt or get left in the dust. Strong opinion here: if you're not opting in, you're basically leaving cash on the table. Sound familiar? It's like ignoring that gym membership discount because you're too lazy to sign up.

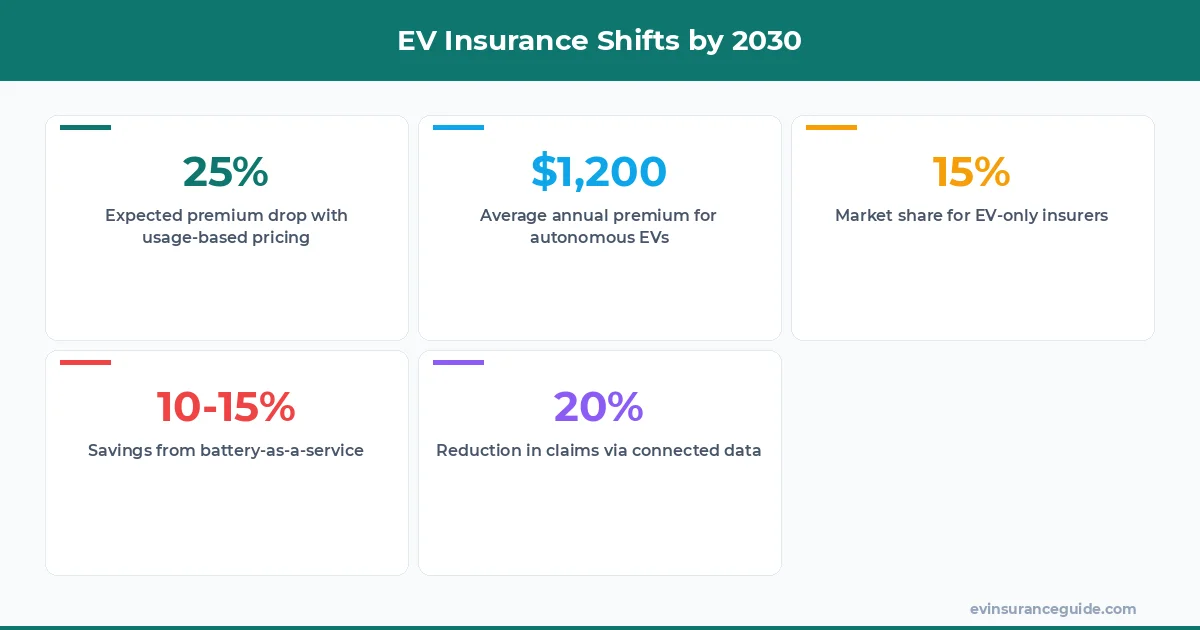

By 2027, I predict this'll be standard, cutting average premiums by 25% for low-mileage EV owners. That's not guesswork; it's based on early pilots from insurers like Lemonade, who've seen similar drops. So, yeah, the future of EV insurance is brighter if you're a cautious driver — but slouch, and you'll pay the price.

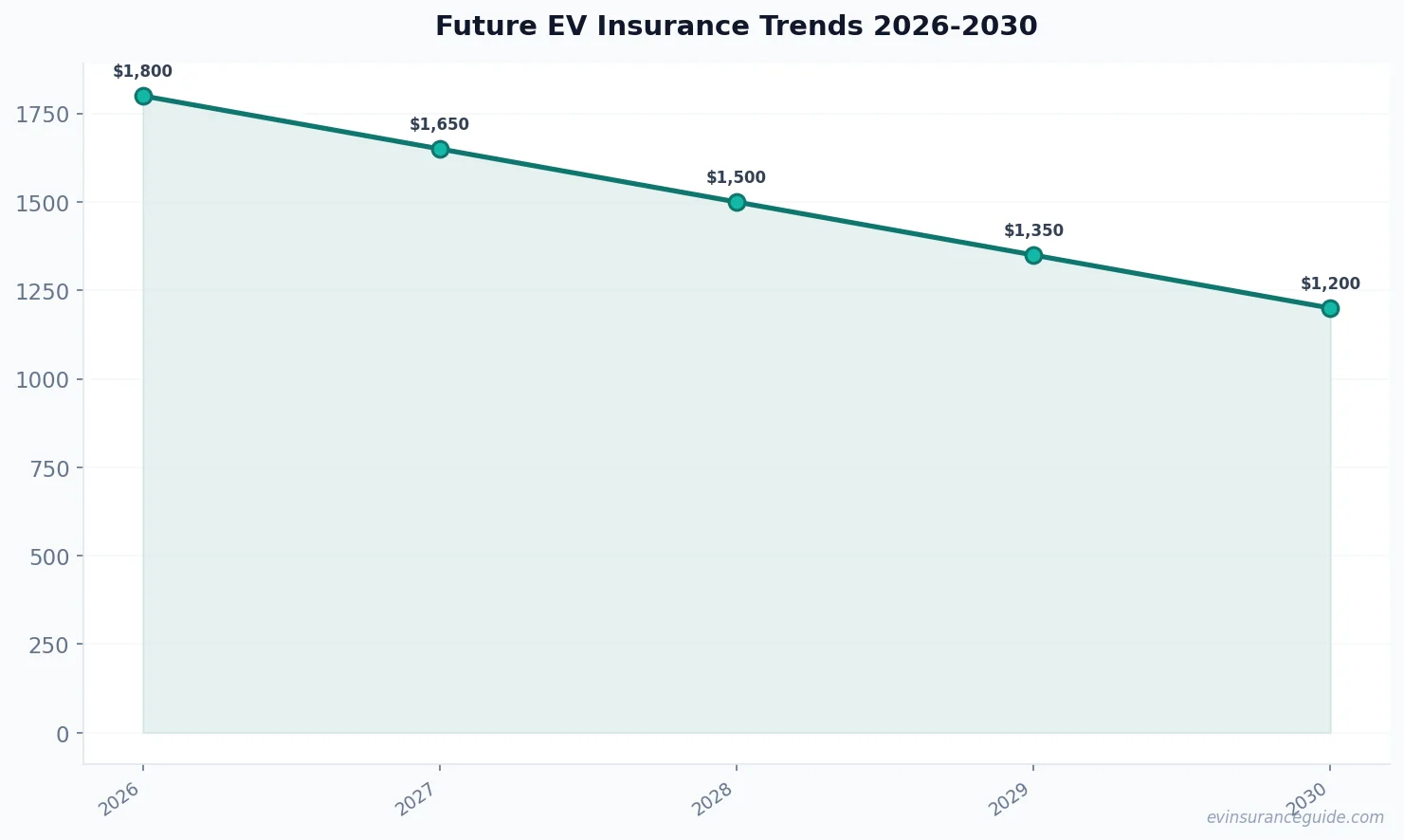

That Wild Story About Autonomous Driving Flipping Liability Ever wonder what happens when your car drives itself? Picture this: you're in a Rivian, cruising on autopilot, and bam — something goes wrong. In the future of EV insurance, liability shifts from you to manufacturers like Tesla, and that's a story worth telling. I remember a buddy who barely escaped a fender-bender in his Model Y; if that were 2026, Tesla might be on the hook instead of him fighting with his insurer. This trend means premiums could drop by 30% for autonomous vehicle owners, as companies absorb more risk — think policies around $1,200 annually versus $1,700 today.

But hold on, it's not all roses. While BMW iX owners might celebrate lower rates, what if software glitches cause issues? Manufacturers will have to step up, potentially raising vehicle prices to cover insurance costs. Rhetorical question: Is that a fair trade for hands-free driving? In my book, yes, because it forces big auto to build better tech.

Fast-forward to 2030, and this could dominate the market, with EV-only players like Root gaining ground. The future of EV insurance hinges on this shift, making policies simpler and cheaper — or more complicated if regulations lag.

Busting the Myth That Battery Worries Will Break the Bank Here's a myth that needs smashing: EVs are a battery nightmare, costing a fortune to replace. Wrong. With battery-as-a-service models from Hyundai and similar, that's changing fast, especially for Ioniq 5 and other models. By 2026, you won't sweat a dead battery; instead, lease it like a phone plan, slashing replacement fears and keeping premiums steady at around $1,500 for the average EV owner. OK, wait, scratch that — it's even better, as this service could reduce overall policy costs by 10-15% through warranties and maintenance deals.

Think about it: no more $10,000 surprises for a Tesla pack; companies handle swaps, and you just pay a monthly fee. Is this the end of battery anxiety? Absolutely, and it's a game-changer for the future of EV insurance. Strong opinion: Traditional insurers who ignore this are doomed, while EV specialists thrive.

By 2028, expect this to be widespread, with data showing a 20% drop in related claims. That's the future of EV insurance in action — affordable, reliable, and myth-free.

What's usage-based pricing, and how does it affect my EV premium? It's basically an app tracking your driving to set rates, so for a BMW iX, safe habits could cut your premium by 20% — no more overpaying for idle time.

But if you're a speed demon, expect hikes; by 2027, this could be standard, making the future of EV insurance more personalized.

Will autonomous driving really lower my insurance costs? Yes, as liability shifts to manufacturers, your Tesla Model 3 policy might drop 25-30% by 2030, but only if the tech proves reliable.

Still, early adopters could face higher initial rates until regulations catch up, reshaping the future of EV insurance for everyone.

How does battery-as-a-service work for EVs like the Rivian? It lets you lease the battery, avoiding big replacement bills, potentially saving Hyundai Ioniq 5 owners $500 yearly on premiums through included maintenance.

This trend means less worry about depreciation, a key part of the future of EV insurance starting in 2026.

Can connected car data really adjust premiums in real time? Absolutely, with your EV sending data to insurers, rates might fluctuate daily based on your driving, like dropping 5% for consistent eco-mode use.

By 2029, this could optimize costs, but privacy concerns might slow adoption in the future of EV insurance.

Are EV-only insurance companies worth switching to? If you're driving a Rivian or similar, yes — they offer tailored policies that could undercut traditional ones by 15%, especially with perks for low emissions.

As they gain market share, the future of EV insurance might favor these specialists over the big names.

Alright, so there you have it — the shifts that'll make or break your EV insurance game in the coming years. Whether it's dodging higher premiums or scoring deals with these trends, keep an eye on how the future of EV insurance evolves. Cheers from the EV insurance trenches. — Alex

Pro tip: Always check your driving data before renewing; it could knock 10% off your rate easier than you think.