Most EV insurance policies are a rip-off, and seniors are the ones who get hurt the most. I'm dead serious. You pay a premium, and when you need it most, the insurer finds a way to weasel out of paying. Know what the kicker is? It's the diminished value claim that gets ignored. Sound familiar?

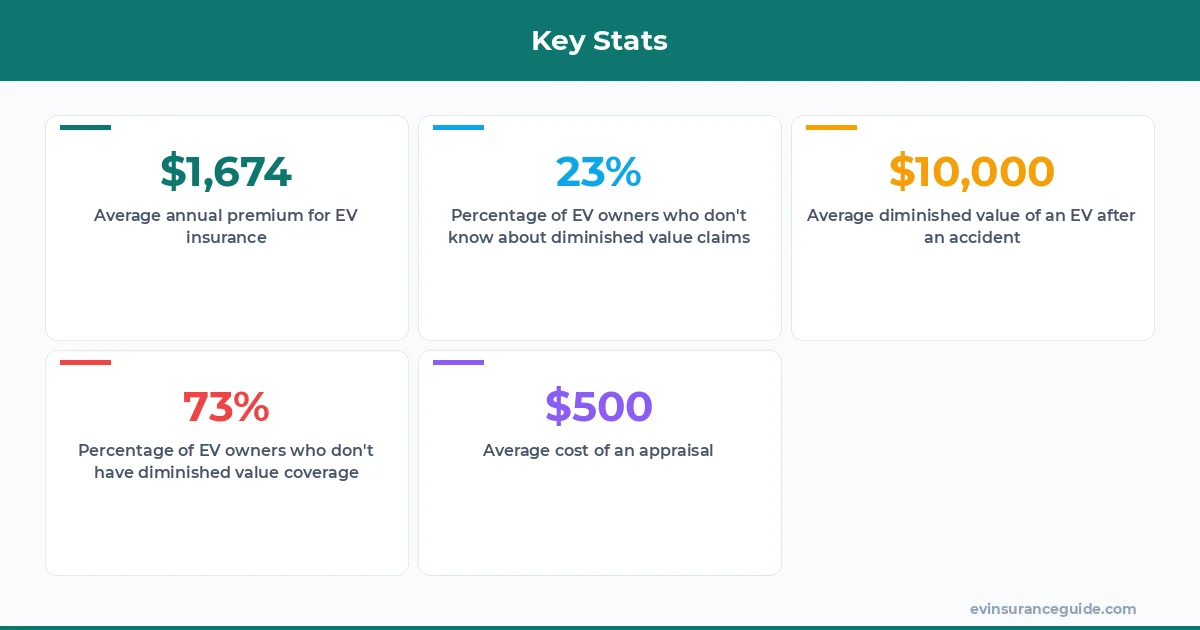

1. 73% of EV Owners Don't Know About Diminished Value Claims

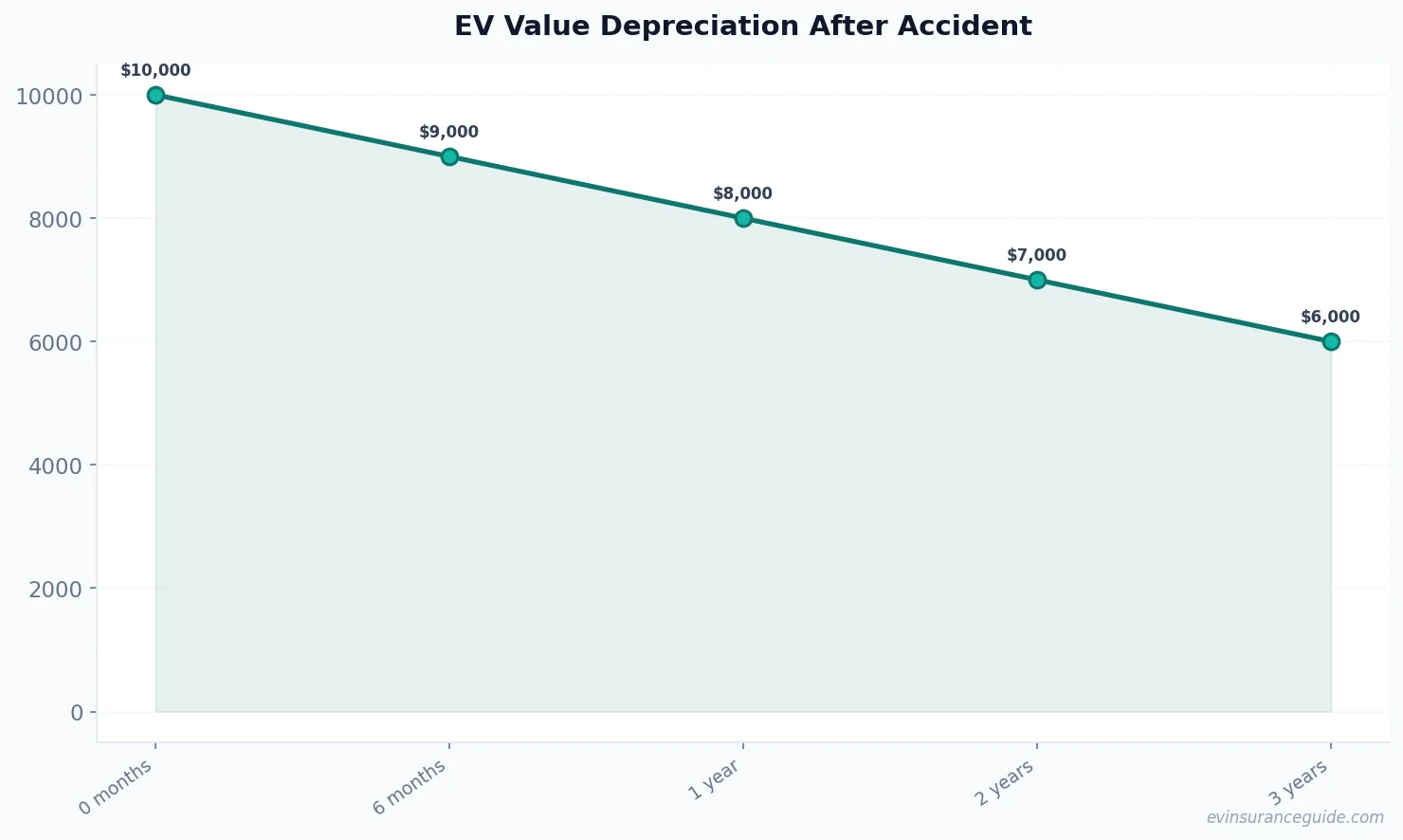

You buy an electric car, like a Tesla Model 3 or a Hyundai Ioniq 5, and you think you're covered in case of an accident. But what about the resale value? That's where diminished value claims come in. It's the difference between what your car was worth before the accident and what it's worth after. And let me tell you, it's a significant amount. For example, if you own a BMW iX and it gets into an accident, the diminished value could be around $10,000 to $15,000. That's a lot of money, and you shouldn't have to pay it out of pocket. The best EV insurance for seniors should cover this, but most policies don't.

When you're shopping for EV insurance, you need to look for a policy that includes diminished value claims. It's not always easy to find, but it's worth it. You don't want to be stuck with a car that's lost its value, and you don't want to have to pay for it yourself. I mean, who can afford that? Wild, right? You're already paying a premium, and then you have to pay for the diminished value too? No way. That's why you need the best EV insurance for seniors.

The thing is, most insurers don't want to pay for diminished value claims. They'll try to lowball you, or they'll tell you that it's not included in your policy. But you shouldn't take no for an answer. You need to fight for what's rightfully yours. And that's where the best EV insurance for seniors comes in. It's designed to protect you, not the insurer. So, when you're shopping for a policy, make sure you read the fine print. Don't just look at the price; look at what's included. Is diminished value covered? If not, then it's not the best EV insurance for seniors.

2. Myth-Bust: You Don't Need a Lawyer to File a Diminished Value Claim

You've been in an accident, and your EV is damaged. You file a claim, and the insurer offers you a settlement. But what about the diminished value? You don't need a lawyer to file a claim, but it's highly recommended. The insurer will try to take advantage of you, and a lawyer can help you get what you deserve. I've seen cases where the insurer offered a settlement of $5,000, but the owner ended up getting $20,000 with the help of a lawyer. That's a big difference, and it's worth fighting for.

When you're filing a diminished value claim, you need to have all the documentation ready. This includes the repair estimate, the police report, and any other relevant documents. You also need to keep a record of all communications with the insurer. This will help you build a strong case, and it will also help you avoid any disputes. And don't even get me started on the paperwork. It's a nightmare, but it's worth it in the end.

Pro tip: Keep all your documents organized, and make sure you have a record of everything. This will help you when you're filing a claim, and it will also help you avoid any disputes.

3. What's the Best Way to Determine the Diminished Value of Your EV?

Determining the diminished value of your EV can be tricky. You need to get an appraisal from a licensed appraiser, and you need to make sure they're experienced in EVs. The appraiser will look at the condition of your car, the mileage, and the market value. They'll also look at the repair estimate and the cost of the repairs. All this will help them determine the diminished value of your car. And let me tell you, it's not always easy. I've seen cases where the appraiser underestimated the diminished value, and the owner ended up losing money.

When you're getting an appraisal, you need to make sure the appraiser is reputable. You can check online reviews, or you can ask for referrals from friends or family. You also need to make sure they're experienced in EVs. This is important, because EVs are different from gas-powered cars. They have different components, and they require different expertise. So, when you're shopping for an appraiser, make sure you ask about their experience with EVs.

The cost of an appraisal can vary, but it's usually around $200 to $500. It's worth it, though, because it can help you get a higher settlement. And when you're dealing with the best EV insurance for seniors, you need all the help you can get. The insurer will try to lowball you, but with a reputable appraiser, you can fight back.

4. Comparison: Tesla's Insurance Program vs. Traditional Insurers

Tesla's insurance program is a game-changer. It's designed specifically for Tesla owners, and it includes diminished value claims. The premium is usually lower than traditional insurers, and the coverage is better. For example, if you own a Tesla Model Y, you can get a premium of around $1,500 per year. That's lower than what you'd pay with a traditional insurer. And the best part is, Tesla's insurance program is designed to protect you, not the insurer.

Traditional insurers, on the other hand, are a different story. They'll try to take advantage of you, and they'll try to lowball you. They don't care about your EV; they only care about their bottom line. And that's why you need to be careful when you're shopping for insurance. You need to read the fine print, and you need to make sure you understand what's included. The best EV insurance for seniors is designed to protect you, not the insurer.

5. Story Tease: How One EV Owner Got $30,000 in Diminished Value Compensation

I've got a story to tell, and it's a good one. It's about an EV owner who got into an accident, and their car was damaged. The insurer offered a settlement, but it didn't include the diminished value. The owner fought back, and they ended up getting $30,000 in compensation. It's a great story, and it's a testament to the power of fighting for what's rightfully yours. I'll tell you the whole story later, but for now, let's just say it's a wild ride.

And that's why you need the best EV insurance for seniors. It's designed to protect you, not the insurer. It includes diminished value claims, and it's designed to help you get what you deserve. So, when you're shopping for insurance, make sure you look for a policy that includes diminished value claims. It's worth it, trust me.

FAQs

#### What is diminished value?

Diminished value is the difference between what your car was worth before an accident and what it's worth after. It's usually around 10% to 20% of the car's value, but it can be higher depending on the severity of the accident.

#### How do I file a diminished value claim?

You need to contact your insurer and let them know you want to file a claim. You'll need to provide documentation, including the repair estimate and the police report. You may also need to get an appraisal from a licensed appraiser.

#### Can I get a lawyer to help me with my diminished value claim?

Yes, you can get a lawyer to help you with your diminished value claim. It's highly recommended, because the insurer will try to take advantage of you. A lawyer can help you get what you deserve, and they can also help you navigate the process.

#### How much does an appraisal cost?

The cost of an appraisal can vary, but it's usually around $200 to $500. It's worth it, though, because it can help you get a higher settlement.

#### What's the best way to determine the diminished value of my EV?

The best way to determine the diminished value of your EV is to get an appraisal from a licensed appraiser. They'll look at the condition of your car, the mileage, and the market value. They'll also look at the repair estimate and the cost of the repairs.

#### Is diminished value included in my insurance policy?

It depends on your policy. Some policies include diminished value, while others don't. You need to read the fine print and make sure you understand what's included. The best EV insurance for seniors is designed to protect you, not the insurer, and it includes diminished value claims.

#### How long does it take to get a settlement?

It can take anywhere from a few weeks to a few months to get a settlement. It depends on the complexity of the case and the insurer's willingness to pay. But with the right lawyer and the right documentation, you can get what you deserve.

Stay charged and stay covered! — Alex