Buying a Rivian R1T feels like upgrading from a regular truck to something straight out of a sci-fi flick, but its insurance setup is more like swapping a basic sedan policy for one that actually notices the 100+ kWh battery pack hiding underneath. Most drivers assume EVs just slip into the same auto slot as gas cars, yet the real contrast shows up in how claims adjusters treat a dead battery versus a blown engine.

Busting the Myth That Do You Need Special EV Insurance Is Always Required

Plenty of owners panic when they see a $2,800 quote for their BMW iX and assume they must hunt down some EV-only policy. That's the myth getting busted right here. Standard auto insurance from GEICO or State Farm already covers collision, liability, and comprehensive for your Tesla Model 3 without forcing you into a specialty product. The battery itself falls under comprehensive in most cases, though depreciation hits harder than on a gas car.

One quick data point: average comprehensive claims for EVs run around $4,200 compared to $2,900 for ICE vehicles according to recent industry reports. Still, that doesn't mean you need a brand-new policy. It just means reading the fine print on what counts as wear and tear. Know what the kicker is? Many people overpay for unnecessary riders when their existing coverage already handles 80 percent of typical issues.

Sound familiar if you've ever shopped for a Hyundai Ioniq 5? The question of do you need special EV insurance pops up constantly, yet the answer stays no in most everyday scenarios. Roadside assistance is where things get tricky though, since a flat tire on an EV often requires flatbed towing to avoid damaging the battery. That's why checking your current policy's towing limits matters more than switching carriers outright.

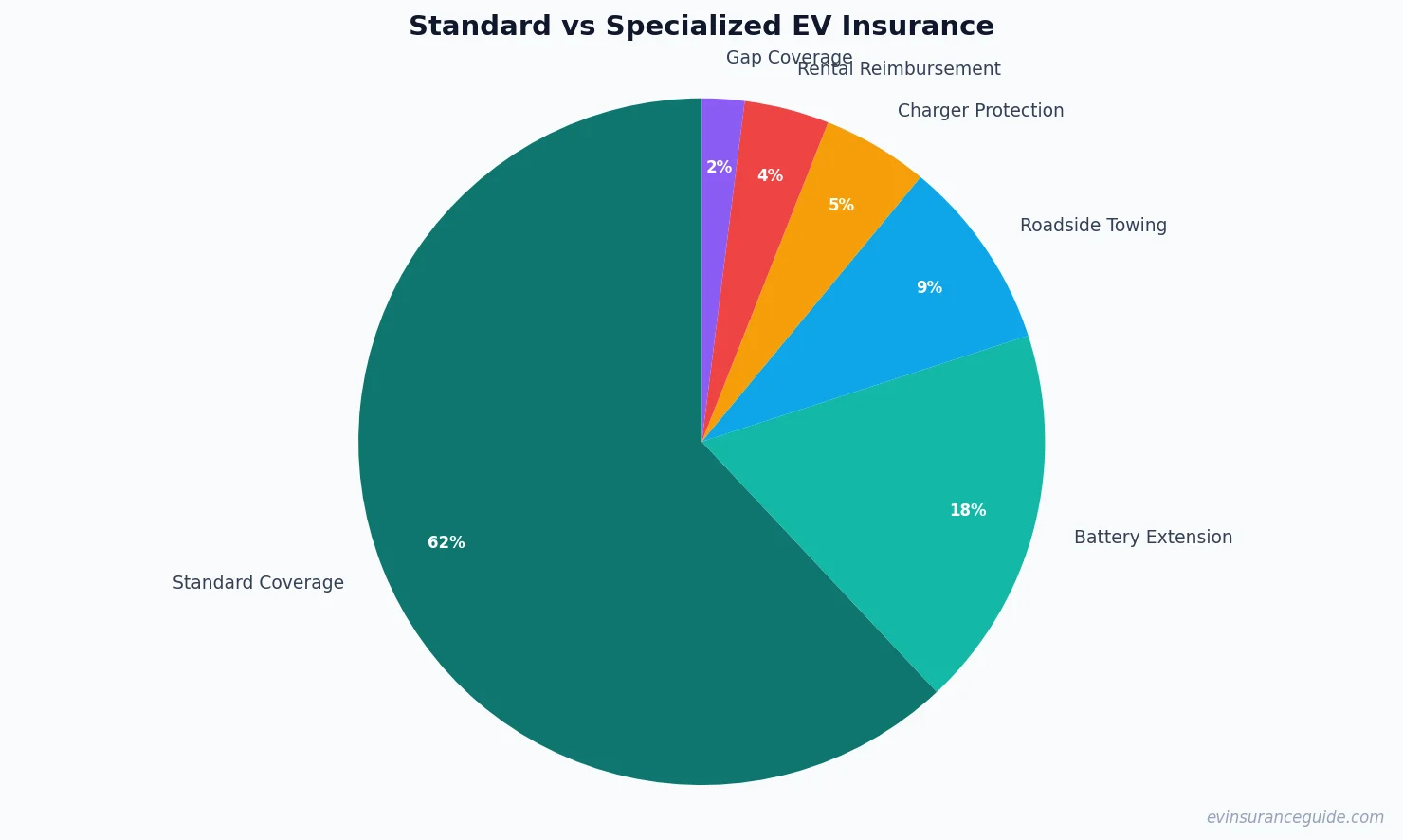

5 Add-Ons Worth Adding Even If Standard Coverage Handles Most Needs

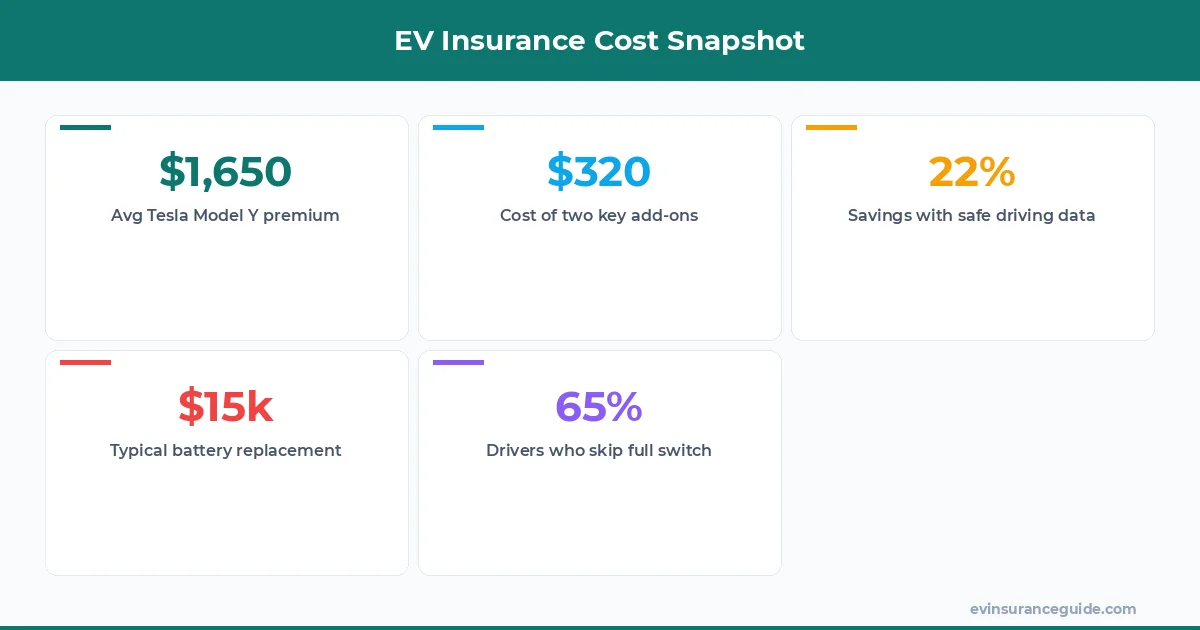

Start with battery coverage extension because a new pack for a Tesla Model Y can run $15,000 to $20,000 out of pocket after the factory warranty fades. Extending that protection through State Farm costs roughly $180 extra per year but pays off fast if you're keeping the car past year eight. Second, charging equipment coverage protects your home wallbox against surges or theft, something basic policies ignore.

Third comes roadside assistance that specifically includes flatbed towing. GEICO offers this for about $50 annually while many EV-only plans bake it in automatically. Fourth is rental car reimbursement that actually covers another EV when your Rivian is in the shop, since gas alternatives feel like a downgrade. Fifth is gap coverage if you're financing, because EVs lose value quicker than expected in the first three years.

Do you need special EV insurance to bundle these? Not always. Adding them piecemeal to an existing policy keeps costs lower than jumping to Tesla Insurance for most drivers with clean records. One realistic stat: bundling battery extension and EV towing adds only $320 yearly on average versus $650 for a full specialized switch.

Tesla Insurance Versus State Farm Ends Up More Lopsided Than Anyone Expects

Picture Tesla Insurance as the flashy new sports drink while State Farm is the reliable water bottle everyone grew up with. Tesla Insurance uses real-time driving data from the car itself to drop rates for careful owners of Model 3 and Model Y vehicles down to $1,450 a year in some states. State Farm counters with broader network repair shops and easier claims handling for the BMW iX crowd, though their base premiums sit closer to $1,950.

The unexpected twist appears in how each handles charging station damage. Tesla Insurance covers up to $1,000 for home units without extra riders in select plans. State Farm requires an add-on that runs $95 yearly but works across any brand. Wild right? Owners who rarely drive fast or at night often save more with Tesla while frequent road-trippers lean toward traditional carriers for better roadside response times.

Still wondering if do you need special EV insurance in this matchup? The numbers say try your current insurer first before switching. Real claims data shows State Farm settles EV battery issues 12 days faster on average, but Tesla Insurance cuts premiums 22 percent for drivers scoring above 95 on safety metrics.

The Blunt Truth Is Most People Waste Money Chasing EV-Only Policies

Here's the honest take. If your driving record is clean and you're not parking a $90,000 BMW iX, standard coverage from GEICO or Progressive already does the job without drama. Specialized insurers shine only when you want usage-based discounts tied directly to your EV's telemetry or when you plan to keep the car long enough for battery replacement worries to hit.

Do you need special EV insurance for peace of mind alone? Maybe, but the math rarely justifies it for shorter ownership periods. Hyundai Ioniq 5 drivers especially notice this because their vehicles hold value better and repair networks have expanded quickly. Paying extra for Rivian-specific coverage only makes sense if you rack up serious mileage in remote areas where flatbed access matters.

One more stat to chew on: switching solely for EV perks costs an extra $400 to $700 annually for 65 percent of policyholders who never file battery claims. Stick with what you have unless your quote includes those five add-ons I mentioned earlier at a reasonable price.

OK So Here's the Deal With Do You Need Special EV Insurance in Practice

Run your existing policy through a quick audit first. Compare the cost of adding battery extension plus EV towing to State Farm against a fresh quote from Tesla Insurance or Rivian’s partner programs. Most folks land on the side of keeping standard coverage and bolting on just two riders.

Rhetorical questions keep coming up here because the decision hinges on your specific car and habits. A Tesla Model 3 commuter in the suburbs rarely needs the full EV treatment. A Rivian R1T hauling gear into the mountains benefits more from specialized roadside options. Test both angles before deciding.

Real-world example: one owner with a 2022 Hyundai Ioniq 5 kept State Farm and added charging coverage for $110 a year. Total savings versus switching hit $380 annually with no loss in protection quality.

Pro tip: Always request an itemized quote that breaks out battery replacement limits and towing restrictions before signing anything.

Frequently Asked Questions About EV Coverage

Does comprehensive insurance cover EV battery damage?

Yes in most standard policies, though limits vary by carrier. State Farm caps new battery replacement at the depreciated value after year seven while Tesla Insurance offers optional extensions that restore full replacement cost. Check your declarations page for exact wording.

How much does adding battery coverage actually cost?

Expect $150 to $250 per year on top of a base policy for a Tesla Model Y. Hyundai Ioniq 5 owners often pay slightly less at $130 because the pack is smaller. These numbers come from recent 2024 rate comparisons across major carriers.

Will regular roadside assistance tow my EV correctly?

Only if it specifies flatbed service. Many basic plans still send wheel lifts that can damage the battery. GEICO’s EV-specific roadside upgrade guarantees flatbed use for $48 extra yearly.

Is Tesla Insurance cheaper than traditional companies?

For safe drivers with a Model 3 or Model Y it frequently is, dropping rates by up to 22 percent in states where it’s available. Riskier drivers or those with older credit scores often pay more than they would at State Farm.

Should I switch carriers just because I bought an EV?

Only if your current quote refuses to add the key riders at reasonable cost. Most people discover their existing insurer handles do you need special EV insurance questions without forcing a full switch.

What happens if my home charger gets stolen?

Standard homeowners policies may cover it, but auto add-ons through Progressive or GEICO protect it under your vehicle policy for an extra $90 to $120 annually. File the claim with whichever covers the loss faster.

Do Rivian owners need different coverage than Tesla drivers?

Not dramatically, though Rivian partners with specialized programs that bundle better towing distances. The core answer to do you need special EV insurance remains the same regardless of brand.

Shop around once, then stick with the winner for at least two renewal cycles. That approach beats chasing every new EV insurer that launches.

Stay charged and stay covered! — Alex