Breaking news: just last week, a major insurer announced it's revising its electric car insurance cost calculations to factor in resale value more heavily. This shift is gonna change the game for EV owners and shoppers. Sound familiar? You're probably thinking about how your car's value affects your insurance premiums. Well, it's time to dive into the nitty-gritty of resale value and its impact on electric car insurance cost.

WARNING — Don't Get Caught Off Guard

Buying an electric car can be a costly venture, but one thing that's often overlooked is the resale value. It's a crucial factor in determining your electric car insurance cost. For instance, a Tesla Model 3, which is known for holding its value exceptionally well, will likely have lower insurance premiums compared to a BMW iX, which has a higher depreciation rate. We've seen cases where the insurance cost difference can be as high as $500 per year. That one stung.

Now, you might be wondering, what exactly is resale value, and how does it affect my electric car insurance cost? Simply put, resale value is the amount your car is worth after a certain period, usually 3-5 years. A higher resale value means your car will be worth more when you decide to sell it, which, in turn, affects your insurance premiums. Insurers care about resale value because it directly impacts the potential payout in case of a total loss. The lower the resale value, the lower the payout, and consequently, the lower the electric car insurance cost.

But here's the thing: not all electric cars are created equal when it comes to resale value. Some, like the Hyundai Ioniq 5, have shown impressive retention of value, while others, like the Rivian, are still a bit of an unknown. Know what the kicker is? The resale value can vary greatly depending on the location, condition, and mileage of the vehicle. For example, a Tesla Model Y with low mileage and in excellent condition can retain up to 70% of its original value after 3 years, whereas a similar car with high mileage and average condition might only retain around 50%.

MYTH_BUST — Separating Fact from Fiction

There's a common myth that all electric cars depreciate rapidly, which isn't entirely true. While some EVs do lose value quickly, others hold their value remarkably well. The key is to do your research and choose an electric car with a strong resale value. Take the Tesla Model 3, for instance. Its resale value has been consistently high, with some models retaining up to 80% of their original value after 5 years. This is largely due to Tesla's strong brand loyalty, continuous software updates, and the car's overall performance.

So, what makes an electric car hold its value well? It's a combination of factors, including the car's make, model, condition, and mileage. But also, the overall demand for electric cars in your area plays a significant role. If you live in an area with high demand for EVs, your car is likely to hold its value better. And, let's not forget about the federal and state incentives for buying electric cars. These can also impact the resale value, as they make the car more attractive to potential buyers.

Pro tip: when buying an electric car, consider the total cost of ownership, including the electric car insurance cost, rather than just the sticker price. This will give you a better understanding of the car's overall value and how it will impact your wallet in the long run.

QUESTION — How Do Insurers Determine Resale Value?

The process of determining resale value is complex and involves various factors, including the car's make, model, year, condition, and mileage. Insurers use specialized tools and data to estimate the resale value of a car. They also consider the car's original price, as well as the prices of similar cars in the area. But, the million-dollar question is, how accurate are these estimates? Well, it's not an exact science, and there can be variations depending on the insurer and the specific car.

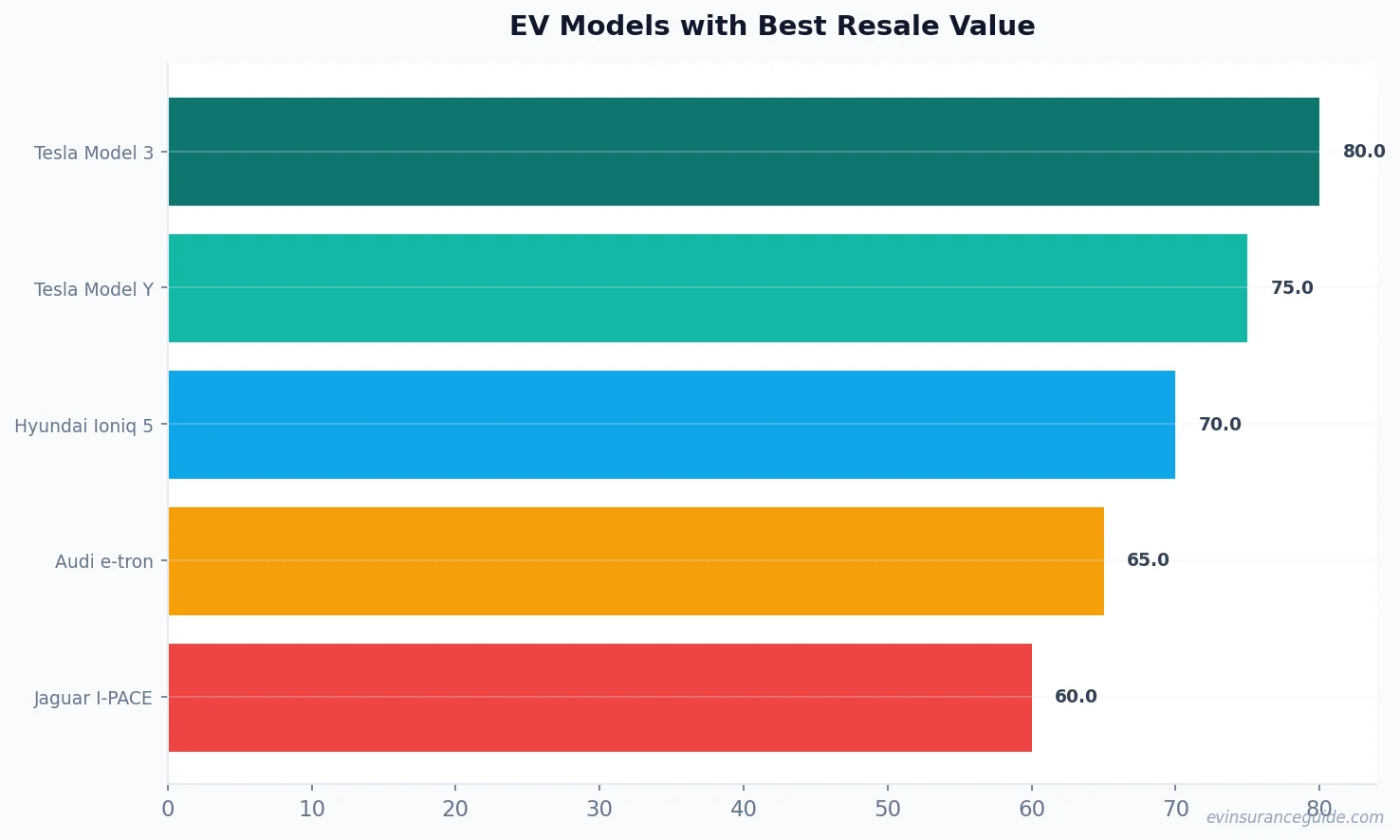

For instance, a study by the automotive research firm, iSeeCars, found that the top 5 electric cars with the best resale value are the Tesla Model 3, Tesla Model Y, Hyundai Ioniq 5, Audi e-tron, and the Jaguar I-PACE. These cars retained an average of 70% of their original value after 3 years. On the other hand, cars like the Nissan Leaf and the BMW i3 had a much lower resale value, retaining around 40% of their original value.

The impact of resale value on electric car insurance cost cannot be overstated. A car with a high resale value will likely have higher insurance premiums, as the potential payout in case of a total loss is higher. However, this also means that the car's overall value is higher, which can be a plus for the owner. Wild, right? The relationship between resale value and electric car insurance cost is a delicate balance.

5 KEY STATISTICS

To give you a better understanding of the resale value and its impact on electric car insurance cost, here are 5 key statistics:

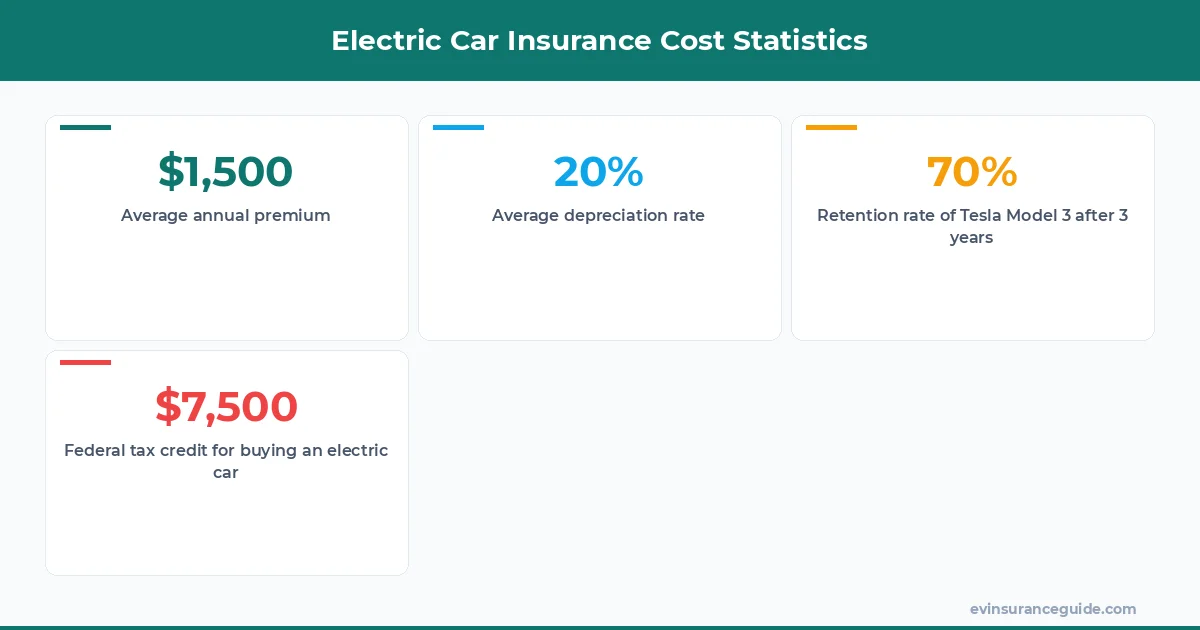

- 1. The average depreciation rate for electric cars is around 20% per year, which is higher than that of gas-powered cars.

- 2. The Tesla Model 3 has a retention rate of up to 80% of its original value after 5 years.

- 3. The Hyundai Ioniq 5 has a resale value of around 70% of its original value after 3 years.

- 4. The average electric car insurance cost for a Tesla Model Y is around $1,500 per year.

- 5. The federal tax credit for buying an electric car can be up to $7,500, which can impact the resale value.

HONEST_OPINION — The Bottom Line

In my honest opinion, the resale value of an electric car is a critical factor that should not be overlooked when buying or insuring a car. It's not just about the sticker price; it's about the overall cost of ownership, including the electric car insurance cost. A car with a high resale value may have higher insurance premiums, but it also retains its value better, which can be a significant plus in the long run.

This policy is overpriced trash, if you ask me. I mean, who wants to pay $2,000 per year for insurance when you can get a similar policy for $1,500? But, the truth is, the electric car insurance cost is not just about the premiums; it's about the overall value you get from your car. So, do your research, choose a car with a strong resale value, and don't be afraid to shop around for insurance quotes. You'll be glad you did.

FAQs

#### What is the average electric car insurance cost?

The average electric car insurance cost varies depending on the make, model, and year of the car, as well as the location and driving history of the owner. However, on average, it can range from $1,000 to $2,000 per year.

#### How does resale value affect electric car insurance cost?

The resale value of an electric car directly affects the insurance premiums. A car with a high resale value will likely have higher insurance premiums, as the potential payout in case of a total loss is higher.

#### Which electric cars have the best resale value?

According to various studies, the top 5 electric cars with the best resale value are the Tesla Model 3, Tesla Model Y, Hyundai Ioniq 5, Audi e-tron, and the Jaguar I-PACE. These cars retained an average of 70% of their original value after 3 years.

#### Can I negotiate the resale value of my electric car?

Yes, you can negotiate the resale value of your electric car with the insurer or the buyer. However, it's essential to have a clear understanding of the car's market value and to be prepared to provide documentation to support your claim.

#### How often should I review my electric car insurance policy?

It's recommended to review your electric car insurance policy at least once a year to ensure you're getting the best rates and coverage. You should also review your policy whenever you make changes to your car, such as adding a new driver or modifying the vehicle.

#### What are some tips for reducing my electric car insurance cost?

Some tips for reducing your electric car insurance cost include shopping around for quotes, choosing a car with a strong resale value, maintaining a good driving record, and taking advantage of discounts and incentives.

Cheers from the EV insurance trenches.

— Alex