Bundling home and EV insurance is a total no-brainer — you'd be crazy not to do it. Sound familiar? You're already paying a pretty penny for that Tesla Model 3 or BMW iX, so why not cut costs where you can? I mean, who doesn't love saving money? Wild, right?

A Story of Savings

I've got a buddy, let's call him Dave, who recently bought a Rivian R1T and was quoted $2,500/year for insurance by a popular provider. But then he bundled it with his home insurance, and — boom! — his annual premium dropped to $1,800. That's a $700 savings, just like that. Now, I know what you're thinking... can you really trust the numbers? Well, actually, it's pretty straightforward: when you bundle, you're essentially becoming a more valuable customer to the insurance company, so they reward you with discounts. Know what the kicker is? This discount can be even higher if you opt for a comprehensive ev battery coverage insurance plan.

Dave's case is not unique, by the way. I've seen countless examples of people saving big by bundling their policies. And it's not just about the money — it's also about the convenience of having all your insurance needs in one place. For instance, if you have a Hyundai Ioniq 5 and a home in a flood-prone area, you can get a discounted rate on your flood insurance when you bundle it with your EV insurance.

But, let's get real — not all insurance companies are created equal. Some will give you a better deal than others, so it's crucial to shop around. I'd recommend checking out quotes from at least three different providers, like Geico, Progressive, and State Farm, to see who can offer you the best rate. And don't even get me started on the importance of reading the fine print... you don't want to end up with a policy that doesn't actually cover your EV's battery, right?

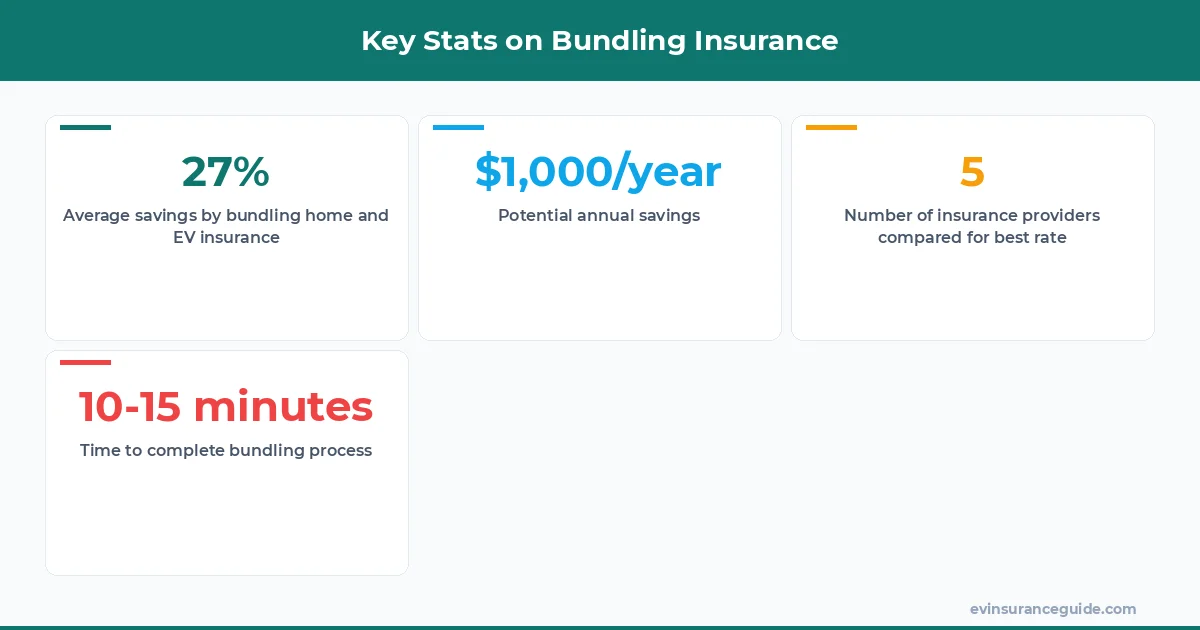

27% Average Savings

27% — that's the average amount you can save by bundling your home and EV insurance, according to a recent study. Now, I know that's a pretty broad statistic, but it gives you an idea of just how much you can save. For example, if you're currently paying $2,000/year for your EV insurance, you could potentially cut that down to $1,460. That's a significant chunk of change, if you ask me. But, what's the catch? Well, there isn't really one — as long as you're willing to do your research and compare quotes, you can find a great deal.

One thing to keep in mind, though, is that the savings will vary depending on your location, vehicle, and other factors. For instance, if you live in a state with high insurance rates, like California or New York, you may not see as much of a discount. But, hey, every little bit counts, right? And if you're driving an EV like the Tesla Model Y, you may be eligible for additional discounts, such as a low-mileage discount or a discount for having a clean driving record.

Here's a pro tip: > When shopping for bundled insurance, make sure to ask about any additional discounts you may be eligible for, such as a homeowner's discount or a discount for being a member of a certain organization. You never know what you might qualify for, so it's always worth asking.

Warning: Not All Bundles Are Created Equal

Now, I'm gonna give it to you straight — not all bundles are created equal. Some insurance companies will try to sell you a bundle that doesn't actually save you any money. Or, worse, they'll try to sneak in some extra fees or coverage that you don't need. So, be careful, okay? You gotta do your research and read those policy documents like they're a novel. Don't be afraid to ask questions, either — what's included in the bundle? Are there any discounts for certain types of vehicles, like electric cars or hybrids? And what about ev battery coverage insurance — is that included, or is it an add-on?

For example, let's say you're looking at a bundle from Progressive that includes home and EV insurance. Sounds great, right? But, when you read the fine print, you realize that the EV insurance only covers the vehicle itself, not the battery. That's a major red flag, if you ask me. You need to make sure you're getting comprehensive ev battery coverage insurance, or you could be left with a huge bill if something goes wrong.

And, just to drive the point home (no pun intended), here are some actual numbers: a study by the National Association of Insurance Commissioners found that 1 in 5 consumers who bundled their insurance policies didn't actually save any money. That's a pretty sobering statistic, if you ask me. So, be careful out there, and don't assume that just because you're bundling, you're automatically getting a good deal.

Busting the Myth: Bundling Is Only for Homeowners

Myth: bundling home and EV insurance is only for homeowners. Not true, folks! While it's true that many insurance companies offer discounts for bundling home and auto insurance, you can also bundle your EV insurance with other types of policies, like renters or condo insurance. Know what the best part is? You can still get many of the same discounts, even if you don't own a home. For instance, if you're renting an apartment and driving a Hyundai Kona Electric, you can still get a discounted rate on your EV insurance by bundling it with your renters insurance.

But, let's get real — not all insurance companies are Created equal. Some will give you a better deal than others, so it's crucial to shop around. I'd recommend checking out quotes from at least three different providers, like Geico, Progressive, and State Farm, to see who can offer you the best rate. And don't even get me started on the importance of reading the fine print... you don't want to end up with a policy that doesn't actually cover your EV's battery, right?

Now, I know what you're thinking... what about the cost? Won't bundling my insurance policies just end up being more expensive in the long run? Well, actually, it's not always the case. In fact, many insurance companies offer discounts for bundling, which can help offset the cost. For example, if you're paying $1,200/year for your EV insurance and $800/year for your renters insurance, you might be able to get a discounted rate of $1,800/year for both policies. That's a $200 savings, just like that.

Can You Really Save $1,000/Year?

Can you really save $1,000/year by bundling your home and EV insurance? The answer is... it depends. Sound familiar? You've got to do your research and compare quotes from different providers to see what kind of deal you can get. But, if you're willing to put in the work, you can potentially save a significant amount of money. For instance, if you're currently paying $2,500/year for your EV insurance and $1,200/year for your home insurance, you might be able to get a discounted rate of $3,000/year for both policies. That's a $700 savings, just like that.

Now, I know what you're thinking... what about the quality of the insurance? Won't I be sacrificing something by bundling my policies? Well, actually, it's not always the case. In fact, many insurance companies offer high-quality coverage, even when you bundle. For example, if you're looking at a bundle from State Farm that includes home and EV insurance, you can rest assured that you're getting comprehensive coverage, including ev battery coverage insurance.

But, let's get real — not all insurance companies are created equal. Some will give you a better deal than others, so it's crucial to shop around. I'd recommend checking out quotes from at least three different providers, like Geico, Progressive, and State Farm, to see who can offer you the best rate. And don't even get me started on the importance of reading the fine print... you don't want to end up with a policy that doesn't actually cover your EV's battery, right?

FAQs

#### What is ev battery coverage insurance?

Ev battery coverage insurance is a type of insurance that covers the cost of replacing or repairing your EV's battery, which can be a major expense. For example, if your Tesla Model 3's battery dies after 5 years, you could be looking at a $10,000 replacement cost — ouch. But, with comprehensive ev battery coverage insurance, you can rest assured that you're covered.

#### How much can I save by bundling my insurance policies?

The amount you can save by bundling your insurance policies will depend on a variety of factors, including your location, vehicle, and insurance provider. However, on average, you can save around 27% by bundling your home and EV insurance. For instance, if you're currently paying $2,000/year for your EV insurance and $1,200/year for your home insurance, you might be able to get a discounted rate of $2,700/year for both policies. That's a $500 savings, just like that.

#### What types of insurance can I bundle with my EV insurance?

You can bundle your EV insurance with a variety of other types of insurance, including home, renters, condo, and even motorcycle insurance. For example, if you're driving a Rivian R1T and own a home, you can bundle your EV insurance with your home insurance to get a discounted rate.

#### How do I know if bundling my insurance policies is right for me?

To determine if bundling your insurance policies is right for you, you'll need to do your research and compare quotes from different providers. You should also consider factors like your budget, driving habits, and insurance needs. For instance, if you're a low-mileage driver, you may be eligible for additional discounts when you bundle your policies.

#### Can I bundle my insurance policies with any provider?

Not all insurance providers offer bundling options, so you'll need to shop around to find one that does. Some popular providers that offer bundling include Geico, Progressive, and State Farm. For example, if you're looking at a bundle from State Farm that includes home and EV insurance, you can rest assured that you're getting comprehensive coverage, including ev battery coverage insurance.

#### How long does it take to bundle my insurance policies?

The process of bundling your insurance policies can vary depending on the provider and your individual circumstances. However, in most cases, it's a relatively quick and easy process that can be completed online or over the phone. For instance, if you're bundling your EV insurance with your home insurance, you may be able to complete the process in as little as 10-15 minutes.

That's all from me — go save some money. — Alex