I'm sitting at a charging station, sipping on a coffee, and overhearing a conversation between two EV owners. They're discussing their insurance premiums, and one of them mentions that they're paying over $2,500 per year for their Tesla Model 3. The other owner chimes in, saying they're paying less than $1,800 for their Hyundai Ioniq 5. Sound familiar? Know what the kicker is? The second owner has a longer commute and a worse driving record. Wild, right?

MYTH_BUST — EV Depreciation and Insurance: Separating Fact from Fiction

EV depreciation and insurance is a complex topic, and there are many myths surrounding it. One common myth is that EVs depreciate faster than gas-powered vehicles. While it's true that EVs can depreciate quickly, it's not always the case. For example, the Tesla Model Y has held its value exceptionally well, with some models retaining up to 90% of their original price after three years. That's a significant factor in EV depreciation and insurance, as it affects the overall cost of ownership.

But what about insurance premiums? Well, actually, EV insurance premiums can be higher than those for gas-powered vehicles, but not always. It really depends on the specific model, your location, and your driving record. For instance, the Rivian R1T has a higher insurance premium than the BMW iX, despite being a similar luxury EV. And, yeah, I know, another insurance article. But hear me out.

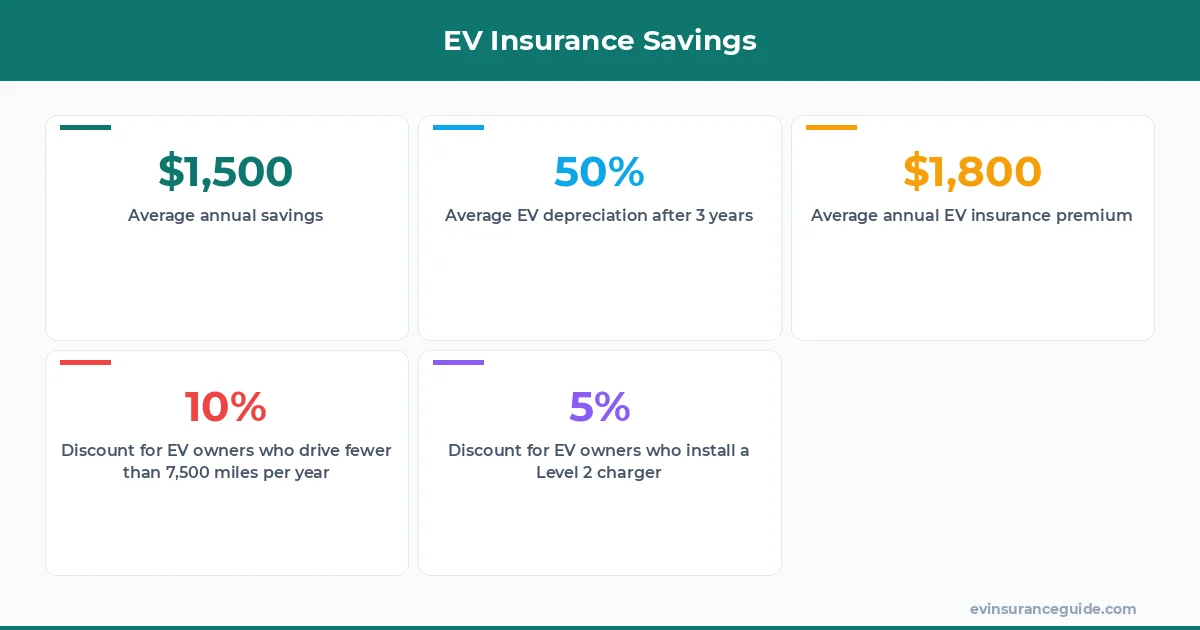

The key to understanding EV depreciation and insurance is to look at the data. According to a study by Kelley Blue Book, the average EV depreciates by around 50% after three years. However, some models, like the Nissan Leaf, can depreciate by as much as 60% in the same timeframe. That's a significant difference, and it's something to consider when purchasing an EV. EV depreciation and insurance are closely linked, and understanding this relationship can help you make informed decisions.

WARNING — The Hidden Costs of EV Insurance

One of the biggest mistakes EV owners make is not considering the hidden costs of insurance. For example, some insurance companies charge higher premiums for EVs with advanced safety features, like adaptive cruise control or lane departure warning. And, let's be real, those features are a major selling point for many EVs. But, dead serious, they can also increase your insurance premium.

Another hidden cost is the potential for higher repair costs. EVs often require specialized repair shops and technicians, which can drive up the cost of repairs. According to a report by the National Association of Insurance Commissioners, the average repair cost for an EV is around $1,500, compared to $1,000 for a gas-powered vehicle. That's a significant difference, and it's something to consider when purchasing an EV. EV depreciation and insurance are closely tied to these costs, and understanding them can help you save money.

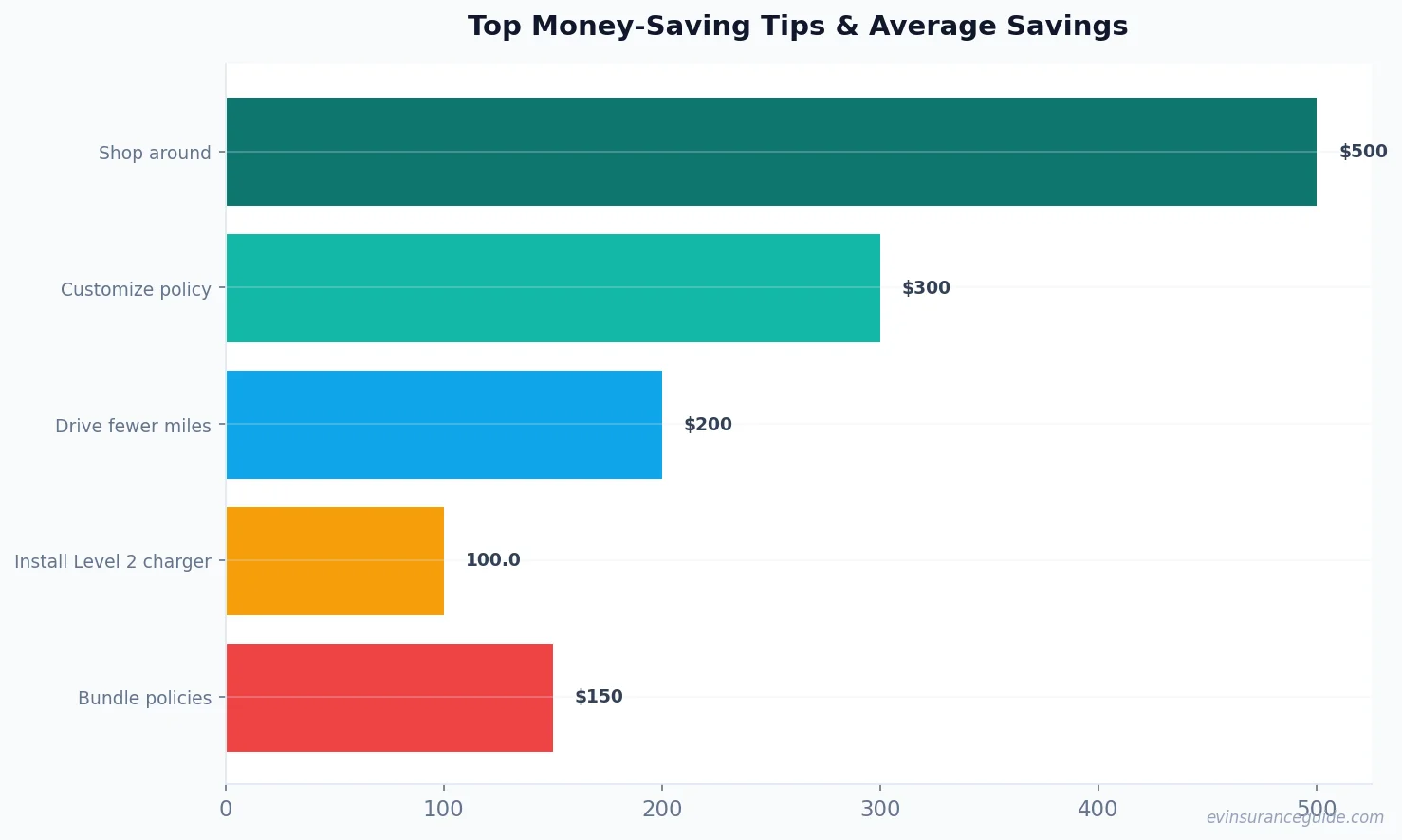

But, on the other hand, some insurance companies offer discounts for EV owners who charge their vehicles at home. For example, State Farm offers a 5% discount for EV owners who install a Level 2 charger at their home. That's a great way to save money, and it's something to consider when shopping for insurance.

QUESTION — Can You Really Save Money on EV Insurance?

So, can you really save money on EV insurance? The answer is yes, but it depends on a variety of factors. For example, if you have a good driving record and live in a low-risk area, you may be able to qualify for a lower premium. Additionally, some insurance companies offer discounts for EV owners who drive fewer than 7,500 miles per year.

Pro tip: Shop around for insurance quotes and compare rates from different companies. You can save up to $500 per year by switching to a different insurance company. And, yeah, it's a pain to shop around, but it's worth it in the long run.

According to a study by the Insurance Institute for Highway Safety, the average EV owner can save around $200 per year by switching to a different insurance company. That's a significant savings, and it's something to consider when shopping for insurance. EV depreciation and insurance are closely tied to these costs, and understanding them can help you save money.

STORY_TEASE — My Friend's Experience with EV Insurance

I have a friend who owns a Rivian R1T, and he's had a wild experience with EV insurance. He initially purchased a policy from a well-known insurance company, but he soon realized that he was overpaying. He shopped around and found a better deal with a different company, saving him around $800 per year. That's a significant savings, and it's a great example of how shopping around can pay off.

But, here's the thing: my friend's experience is not unique. Many EV owners are overpaying for insurance, simply because they don't understand the complexities of EV depreciation and insurance. EV depreciation and insurance are closely linked, and understanding this relationship can help you make informed decisions.

COMPARISON — EV Insurance vs. Gas-Powered Vehicle Insurance

So, how does EV insurance compare to gas-powered vehicle insurance? Well, actually, it's a mixed bag. On the one hand, EVs often have higher insurance premiums due to their advanced technology and higher repair costs. On the other hand, EVs are often safer than gas-powered vehicles, which can result in lower premiums.

For example, the Tesla Model 3 has a 5-star safety rating and is considered one of the safest vehicles on the road. As a result, insurance premiums for the Model 3 are often lower than those for similar gas-powered vehicles. But, and this is a big but, the Model 3 is also a luxury vehicle, and that can drive up the cost of insurance.

FAQs

#### What is the average cost of EV insurance?

The average cost of EV insurance varies depending on the model, location, and driving record. However, according to a report by the National Association of Insurance Commissioners, the average annual premium for an EV is around $1,800.

#### Can I save money on EV insurance by driving fewer miles?

Yes, some insurance companies offer discounts for EV owners who drive fewer than 7,500 miles per year. For example, State Farm offers a 10% discount for EV owners who drive fewer than 7,500 miles per year.

#### What is the best way to compare EV insurance quotes?

The best way to compare EV insurance quotes is to shop around and compare rates from different companies. You can use online tools or work with an insurance agent to find the best rate.

#### How does EV depreciation affect insurance premiums?

EV depreciation can affect insurance premiums in a few ways. For example, if an EV depreciates quickly, the insurance company may charge a higher premium to reflect the lower value of the vehicle. On the other hand, if an EV holds its value well, the insurance company may charge a lower premium.

#### Can I customize my EV insurance policy to fit my needs?

Yes, many insurance companies offer customizable policies that allow you to choose the coverage and deductible that fit your needs. For example, you may be able to add coverage for roadside assistance or rental cars.

#### What is the most important factor in determining EV insurance premiums?

The most important factor in determining EV insurance premiums is the vehicle's value. Insurance companies use a variety of factors to determine the value of an EV, including its make, model, year, and condition.

And, finally, the key to saving money on EV insurance is to understand the complexities of EV depreciation and insurance. By shopping around, comparing rates, and customizing your policy, you can save up to $1,500 per year. That's a significant savings, and it's something to consider when purchasing an EV. EV depreciation and insurance are closely tied, and understanding this relationship can help you make informed decisions.

Stay charged and stay covered! — Alex