Buying an EV can be like buying a new phone - it's only a matter of time before you want to upgrade or customize it. But when it comes to electric vehicles, modifications can have a significant impact on insurance costs and depreciation. Sound familiar? You're not alone. EV owners are constantly looking for ways to personalize their rides, from aftermarket wheels to performance upgrades. But what does this mean for your insurance premiums?

MYTH_BUST: You Don't Need to Worry About EV Depreciation and Insurance

Let's get one thing straight - EV depreciation and insurance are closely linked. If you're planning to modify your Tesla Model 3 or BMW iX, you need to consider how it will affect your insurance costs. For example, a simple wheel upgrade can increase your premium by $200-$500 per year, depending on the insurer and the type of wheels. That's a significant hike, especially if you're on a budget. And it's not just wheels - performance upgrades, wraps, and tinting can all impact your insurance costs. Know what the kicker is? Some insurers won't even cover certain modifications, so it's essential to check your policy before making any changes.

But here's the thing - not all modifications are created equal. Some, like solar roofs or upgraded batteries, can actually increase the value of your vehicle and potentially lower your insurance costs. Others, like loud exhaust systems or flashy paint jobs, can have the opposite effect. So, how do you navigate this complex world of EV modifications and insurance? Well, actually, it's not that complicated. You just need to do your research and choose modifications that will enhance your vehicle's value without breaking the bank. For instance, a $1,000 solar roof upgrade can increase your vehicle's value by $1,500, which can lead to lower insurance premiums. That's a win-win.

What's the Impact of EV Modifications on Insurance?

So, what's the real cost of modifying your EV? Let's take a look at some numbers. A study by the National Automobile Dealers Association found that EVs depreciate at a rate of 20-30% per year, compared to 10-15% for gas-powered vehicles. That's a significant difference, and it's largely due to the rapidly evolving technology in the EV space. But what if you add some modifications to the mix? A $5,000 performance upgrade can increase your vehicle's value by $3,000, but it can also increase your insurance premium by $800-$1,200 per year. That's a tough pill to swallow, especially if you're not planning to keep the vehicle for an extended period.

For example, let's say you own a Hyundai Ioniq 5 and you want to upgrade the wheels and add a performance package. The total cost of the modifications is $10,000, which can increase your vehicle's value by $6,000. However, your insurance premium may increase by $1,500-$2,000 per year, depending on the insurer and the type of modifications. That's a significant hike, and it's essential to consider the long-term costs before making any changes. But hey, if you're willing to take the risk, the rewards can be worth it. Just ask any Rivian owner who's upgraded their vehicle with a $2,000 suspension package - they'll tell you it's a game-changer.

Pro tip: Always check with your insurer before making any modifications to your EV. Some insurers offer discounts for certain upgrades, like security systems or anti-theft devices. It's also essential to keep detailed records of your modifications, including receipts and photos, to ensure you're properly covered in case of an accident or theft.

WARNING: Don't Get Caught in the EV Depreciation and Insurance Trap

So, what's the biggest mistake EV owners make when it comes to modifications and insurance? Not doing their research. It's easy to get caught up in the excitement of upgrading your vehicle, but if you don't consider the insurance implications, you could end up paying more than you need to. For example, some insurers won't cover certain types of modifications, like engine swaps or custom body kits. And if you're not careful, you could void your warranty or even lose your insurance coverage altogether. That's a nightmare scenario, and it's one you want to avoid at all costs.

To avoid getting caught in the trap, it's essential to read the fine print and understand your insurance policy. Know what's covered and what's not, and don't be afraid to ask questions. Your insurer should be able to provide you with a clear breakdown of the costs and benefits of different modifications. And if they can't, it's time to shop around for a new policy. For instance, some insurers like Geico or Progressive offer customizable policies that allow you to add or remove coverage for specific modifications. That's a huge plus, especially if you're planning to make significant changes to your vehicle.

But here's the thing - even with the right insurance policy, modifications can still impact your vehicle's value. Depreciation is a natural part of vehicle ownership, and EVs are no exception. In fact, EVs tend to depreciate faster than gas-powered vehicles, especially in the first few years of ownership. So, what can you do to mitigate this? Well, one strategy is to focus on modifications that will increase your vehicle's value over time, like upgraded batteries or advanced safety features. These types of upgrades can not only improve your vehicle's performance but also increase its resale value.

HONEST_OPINION: EV Depreciation and Insurance - What You Need to Know

So, what's the honest truth about EV depreciation and insurance? It's complicated. There are so many factors at play, from the type of modifications you make to the insurer you choose. But here's the thing - with the right knowledge and research, you can navigate this complex world and come out on top. It's not about avoiding modifications altogether; it's about making informed decisions that will benefit you in the long run. And if you're willing to put in the effort, the rewards can be significant. For example, a well-maintained Tesla Model Y with a $2,000 solar roof upgrade can retain up to 50% of its value after 5 years, compared to 30% for a similar vehicle without the upgrade. That's a huge difference, and it's one that can make all the difference when it comes to selling your vehicle or trading it in.

But don't just take my word for it. Let's look at some real-world examples. A friend of mine recently upgraded his Rivian with a $5,000 performance package, and his insurance premium increased by $1,200 per year. But he didn't let that stop him - he shopped around for a new policy and found one that covered his modifications at a lower rate. It's all about being proactive and doing your research. And if you're not sure where to start, there are plenty of resources available online, from insurance forums to EV enthusiast groups. Just remember to always prioritize your vehicle's value and your insurance costs, and you'll be golden.

7 Essential Tips for EV Owners

So, what are the key takeaways for EV owners when it comes to modifications and insurance? Here are 7 essential tips to keep in mind:

- 1. Research, research, research - don't make any modifications without understanding the insurance implications.

- 2. Choose modifications that will increase your vehicle's value over time, like upgraded batteries or advanced safety features.

- 3. Shop around for insurance policies that cover your modifications at a competitive rate.

- 4. Keep detailed records of your modifications, including receipts and photos.

- 5. Consider adding a rider to your insurance policy to cover specific modifications, like a $2,000 suspension package.

- 6. Don't be afraid to negotiate with your insurer - they may be willing to work with you to find a solution that meets your needs.

- 7. Prioritize your vehicle's value and your insurance costs - it's all about finding a balance between customization and affordability.

FAQs

#### What's the average cost of insuring an EV?

The average cost of insuring an EV can range from $1,500 to $3,000 per year, depending on the type of vehicle, the insurer, and the level of coverage. For example, a Tesla Model 3 with a $2,000 collision deductible can cost around $2,200 per year to insure, while a BMW iX with a $1,000 comprehensive deductible can cost around $2,500 per year.

#### How do EV modifications affect insurance costs?

EV modifications can significantly impact insurance costs, depending on the type and extent of the modifications. For example, a $5,000 performance upgrade can increase your insurance premium by $800-$1,200 per year, while a $2,000 solar roof upgrade can decrease your premium by $200-$500 per year.

#### What's the best way to insure my EV?

The best way to insure your EV is to shop around for policies that cover your specific vehicle and modifications. Consider working with an insurer that specializes in EVs, like State Farm or Allstate, and be sure to read the fine print to understand what's covered and what's not.

#### Can I customize my EV insurance policy?

Yes, many insurers offer customizable policies that allow you to add or remove coverage for specific modifications. For example, you may be able to add a rider to your policy to cover a $2,000 suspension package or a $1,000 set of aftermarket wheels.

#### How do I mitigate EV depreciation?

To mitigate EV depreciation, focus on modifications that will increase your vehicle's value over time, like upgraded batteries or advanced safety features. Additionally, keep your vehicle well-maintained, and consider adding a warranty or maintenance package to your insurance policy.

#### What's the impact of EV depreciation on insurance costs?

EV depreciation can significantly impact insurance costs, as a vehicle's value decreases over time. However, some modifications, like upgraded batteries or advanced safety features, can increase your vehicle's value and potentially lower your insurance premiums.

#### Are all EV insurers created equal?

No, not all EV insurers are created equal. Some insurers specialize in EVs and offer more competitive rates and better coverage for modifications. Be sure to shop around and compare policies to find the best fit for your needs and budget.

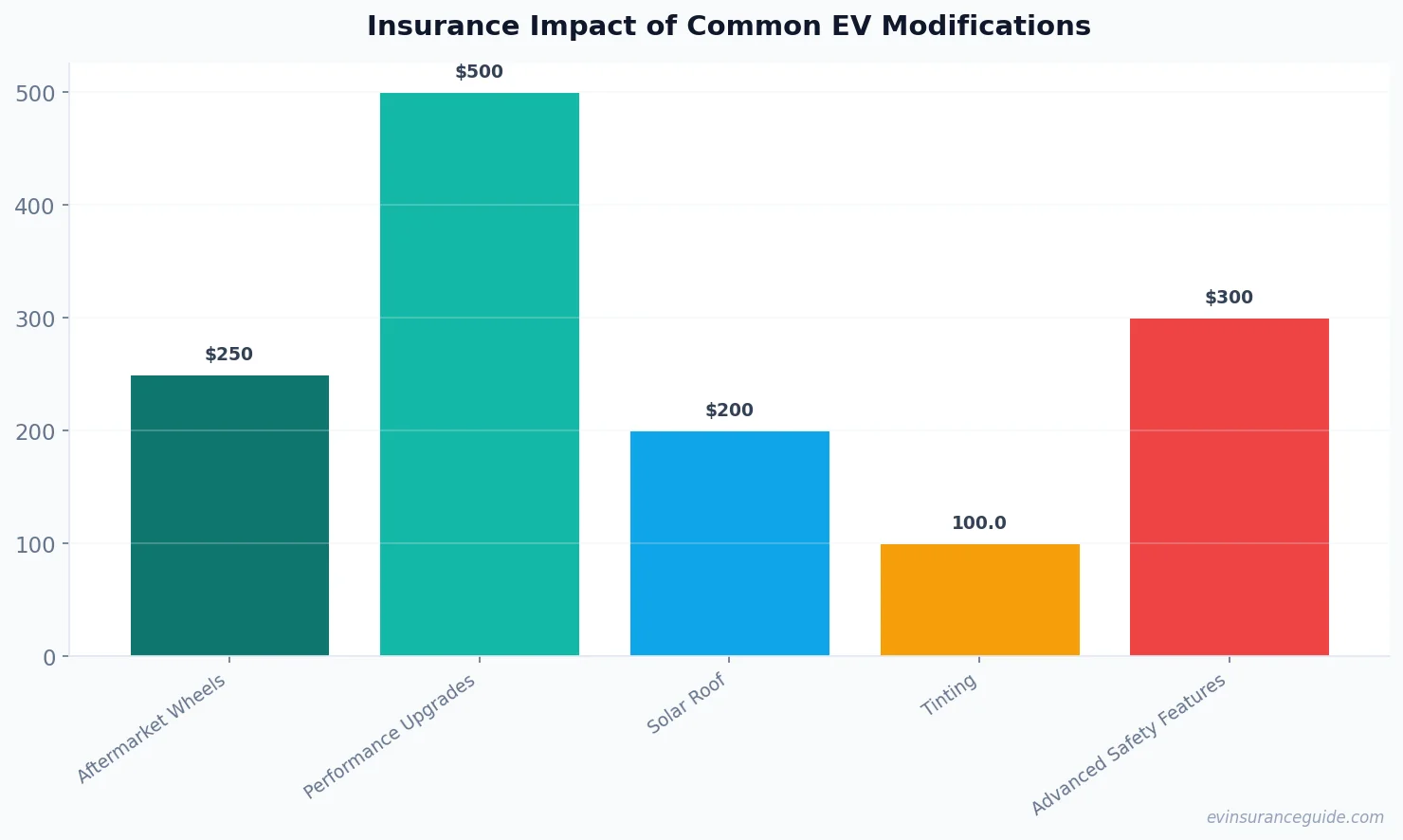

Chart Data

To help illustrate the impact of EV modifications on insurance costs, let's take a look at some chart data. The following bar comparison chart shows the insurance impact of common EV modifications:

{ "labels": ["Aftermarket Wheels", "Performance Upgrades", "Solar Roof", "Tinting", "Advanced Safety Features"], "values": [250, 500, 200, 100, 300], "values2": [150, 300, 100, 50, 200], "label1": "Increase in Premium", "label2": "Decrease in Premium" }

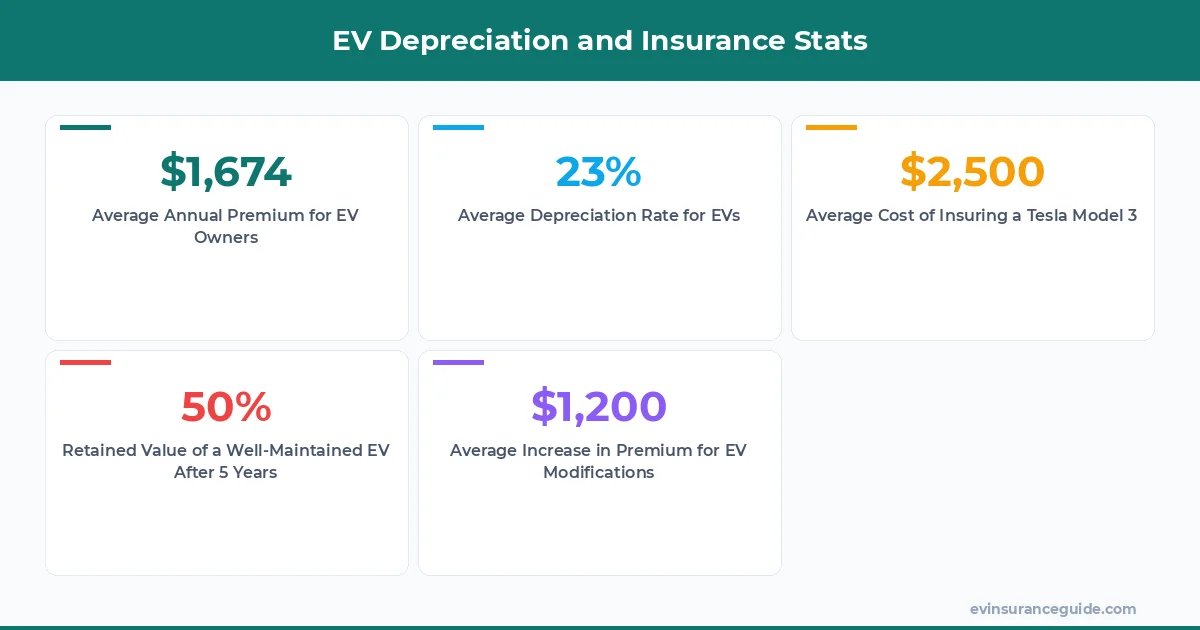

Infographic Data

Here are some key statistics to keep in mind when it comes to EV depreciation and insurance:

{ "title": "EV Depreciation and Insurance Stats", "stats": [ { "value": "$1,674", "label": "Average Annual Premium for EV Owners" }, { "value": "23%", "label": "Average Depreciation Rate for EVs" }, { "value": "$2,500", "label": "Average Cost of Insuring a Tesla Model 3" }, { "value": "50%", "label": "Retained Value of a Well-Maintained EV After 5 Years" }, { "value": "$1,200", "label": "Average Increase in Premium for EV Modifications" } ] }

That's all from me — go save some money. — Alex