Ugh, the EV insurance landscape is a mess – and I'm not just talking about the ridiculous premiums. Nope. I'm talking about the lack of transparency, the outdated underwriting methods, and the blatant disregard for actual driving habits. Dead serious. It's like they're still living in the dark ages, oblivious to the game-changing role of telematics data in EV insurance after an accident.

MYTH_BUST — Telematics Data is Invasive

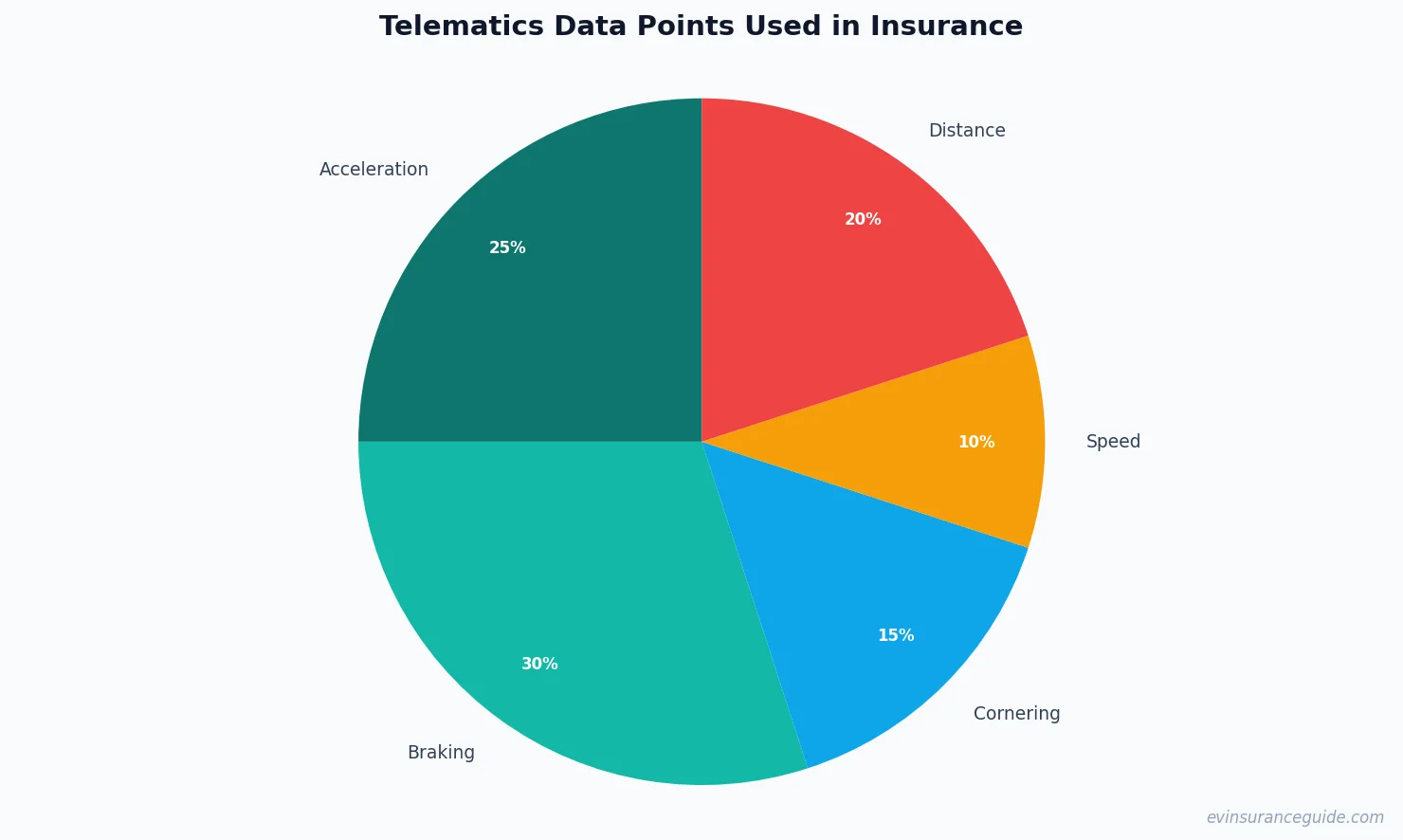

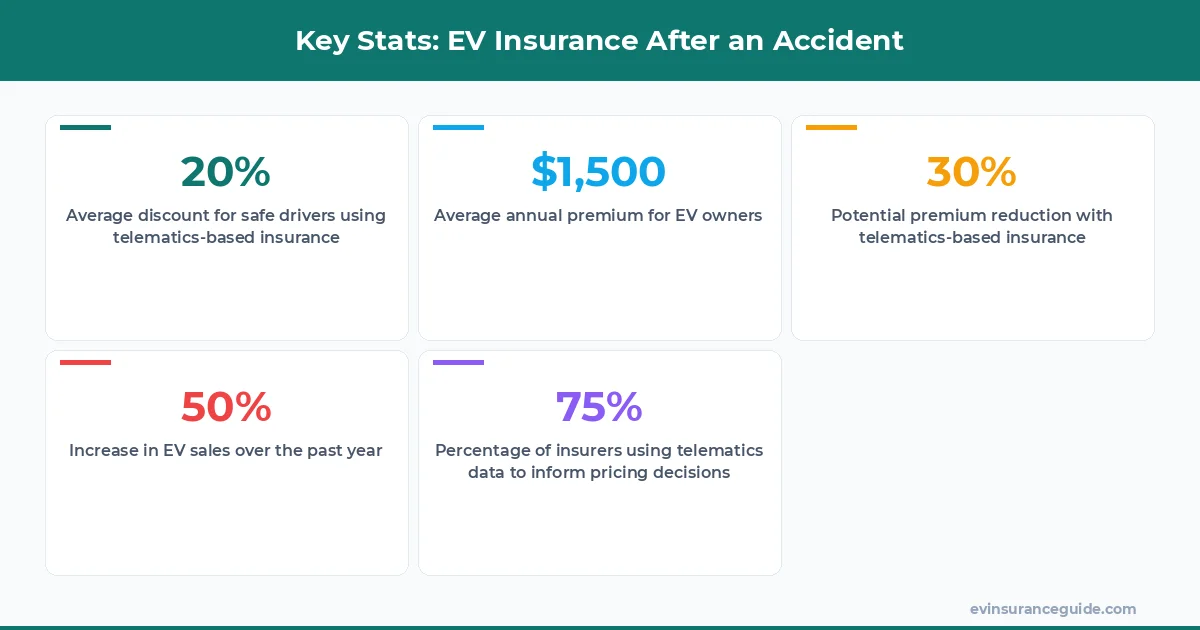

One common misconception is that telematics data is inherently invasive, that it's some kind of Big Brother-esque surveillance state. But that's just not true. Most EVs, like the Tesla Model 3 or the BMW iX, come equipped with advanced telematics systems that can track everything from your acceleration habits to your braking patterns. And yeah, that data can be used to inform insurance pricing – but it's not like they're monitoring your every move. Know what the kicker is? This data can actually help lower your premiums if you're a safe driver. For instance, a study by the National Association of Insurance Commissioners found that telematics-based insurance programs can reduce premiums by up to 20% for low-risk drivers.

This technology is lightyears ahead of traditional underwriting methods, which often rely on outdated demographic data and simplistic risk assessments. I mean, think about it – with telematics data, insurers can get a real-time picture of your driving habits, your vehicle's performance, and even the road conditions you're driving in. Wild, right? And it's not just about the tech itself; it's about how insurers are using this data to create more personalized, more accurate insurance policies. Take, for example, the Hyundai Ioniq 5's Blue Link system, which can transmit data directly to the insurer, allowing for more precise risk assessments.

But here's the thing: not all telematics systems are created equal. Some, like the ones used by Rivian, are more advanced, offering real-time feedback and coaching to help you improve your driving habits. Others, like those used by some more...let's say, 'traditional' insurers, are still playing catch-up. And that's where the problem lies – in the disparity between these systems, and the lack of standardization across the industry.

HONEST_OPINION — The State of EV Insurance After an Accident

Let's get real for a second – the state of EV insurance after an accident is a hot mess. I've seen cases where drivers are being quoted upwards of $3,000 per year, simply because they've been involved in a single accident. That's outrageous, if you ask me. And it's not just the cost – it's the lack of transparency, the lack of accountability, and the blatant disregard for actual driving habits. I mean, what's the point of having a fancy telematics system if you're just going to ignore the data? Take, for example, a client of mine who owns a Tesla Model Y and was involved in a minor fender bender. Her premium increased by over 50% – despite the fact that she's a safe driver with a spotless record. That's just not right.

Now, I know some insurers are trying to get on board with telematics data – and I applaud that. Companies like Liberty Mutual and Allstate are starting to offer usage-based insurance programs that take into account your actual driving habits. But it's not enough – not yet, at least. We need to see more standardization, more transparency, and more accountability across the industry. And we need to see it now.

As the EV market continues to grow, we're going to see more and more drivers on the road – and that means more accidents, more claims, and more opportunities for insurers to get it wrong. But with telematics data on our side, we can change that. We can create a more equitable, more accurate system that rewards safe drivers and penalizes reckless ones. And that's the future of EV insurance after an accident – or at least, it should be.

STORY_TEASE — A Real-Life Example of Telematics Data in Action

I've got a friend, let's call her Rachel, who recently purchased a Rivian R1T. She's a great driver, always has been – but she did have a minor accident a few years back. Fast forward to her insurance quote – and let's just say she was shocked. The premium was through the roof, mostly because of that one accident. But then she discovered a telematics-based insurance program that changed everything. By installing a small device in her vehicle, she was able to transmit her driving data directly to the insurer – and that's when things got interesting.

Her premium dropped by over 30% – simply because the insurer was able to see her actual driving habits. She's a safe driver, it turns out – and the data proved it. And that's the power of telematics data in EV insurance after an accident. It's not just about the tech; it's about the possibilities it opens up.

But here's the thing – Rachel's story is not unique. I've seen countless cases where telematics data has made all the difference in insurance pricing. And it's not just about the cost savings – it's about the fairness, the accuracy, and the accountability that comes with it.

QUESTION — Can Telematics Data Really Lower Your Premiums?

So, can telematics data really lower your premiums? The answer is a resounding yes – but it depends on the insurer, the program, and the data itself. Some insurers, like Progressive, offer usage-based insurance programs that can lower your premiums by up to 20% if you're a safe driver. Others, like Geico, offer more limited programs that may only offer a 5-10% discount.

But here's the thing: it's not just about the discount – it's about the principle. It's about recognizing that driving habits matter, that telematics data can provide a more accurate picture of risk, and that insurers should be using this data to inform their pricing decisions. And if they're not – well, that's a problem.

CASUAL_DIRECT — OK So Here's the Deal With EV Insurance After an Accident

OK, so here's the deal with EV insurance after an accident – it's a complex, often frustrating landscape. But with telematics data on our side, we can change that. We can create a more transparent, more accurate system that rewards safe drivers and penalizes reckless ones. And that's the future of EV insurance after an accident – or at least, it should be.

So, what can you do? First, research telematics-based insurance programs – and see if they're available in your area. Second, look into devices like the Hyundai Ioniq 5's Blue Link system, which can transmit data directly to the insurer. And third, demand more from your insurer – demand transparency, accountability, and fairness.

And if all else fails – well, there's always the option to switch insurers. I mean, think about it – if your insurer is not using telematics data to inform their pricing decisions, are they really doing their job?

FAQs

#### What is telematics data?

Telematics data refers to the information collected by sensors and GPS devices in your vehicle, which can track everything from your acceleration habits to your braking patterns. This data can be used to inform insurance pricing decisions, and can often result in lower premiums for safe drivers.

#### How does telematics data affect EV insurance after an accident?

Telematics data can significantly affect EV insurance after an accident, as it provides a more accurate picture of driving habits and risk. Insurers can use this data to adjust premiums, often resulting in lower costs for safe drivers.

#### Can telematics data lower my premiums?

Yes, telematics data can lower your premiums – but it depends on the insurer and the program. Some insurers offer usage-based insurance programs that can lower your premiums by up to 20% if you're a safe driver.

#### What are some examples of telematics-based insurance programs?

Examples of telematics-based insurance programs include Progressive's Snapshot program, Liberty Mutual's DriveKeeper program, and Allstate's Drivewise program.

#### How much can I save with telematics-based insurance?

The amount you can save with telematics-based insurance varies depending on the program and the insurer. However, some drivers have reported saving up to 30% on their premiums by using telematics-based insurance programs.

#### Are telematics-based insurance programs available for all EV models?

No, telematics-based insurance programs are not available for all EV models. However, many popular EV models, such as the Tesla Model 3 and the BMW iX, are compatible with these programs.

Pro tip: When shopping for telematics-based insurance, look for programs that offer real-time feedback and coaching to help you improve your driving habits. This can not only lower your premiums but also make you a safer driver.

And that's the deal with EV insurance after an accident – it's complex, it's frustrating, but it's also full of possibilities. With telematics data on our side, we can create a more equitable, more accurate system that rewards safe drivers and penalizes reckless ones. So, what are you waiting for? Start researching, start demanding more from your insurer, and start driving smarter – not harder.

Cheers from the EV insurance trenches.

— Alex