OK so someone DM'd me this question... what happens when your EV is totaled? Like, what's the deal with total loss payouts? Sound familiar? You're not alone - we've all had that nagging worry in the back of our minds when driving our shiny new electric vehicles. Know what the kicker is? It's not just about the cost of repairs - it's about the residual value of your EV, and how that affects your insurance payout. Wild, right?

OK So Here's the Deal With Total Loss Payouts

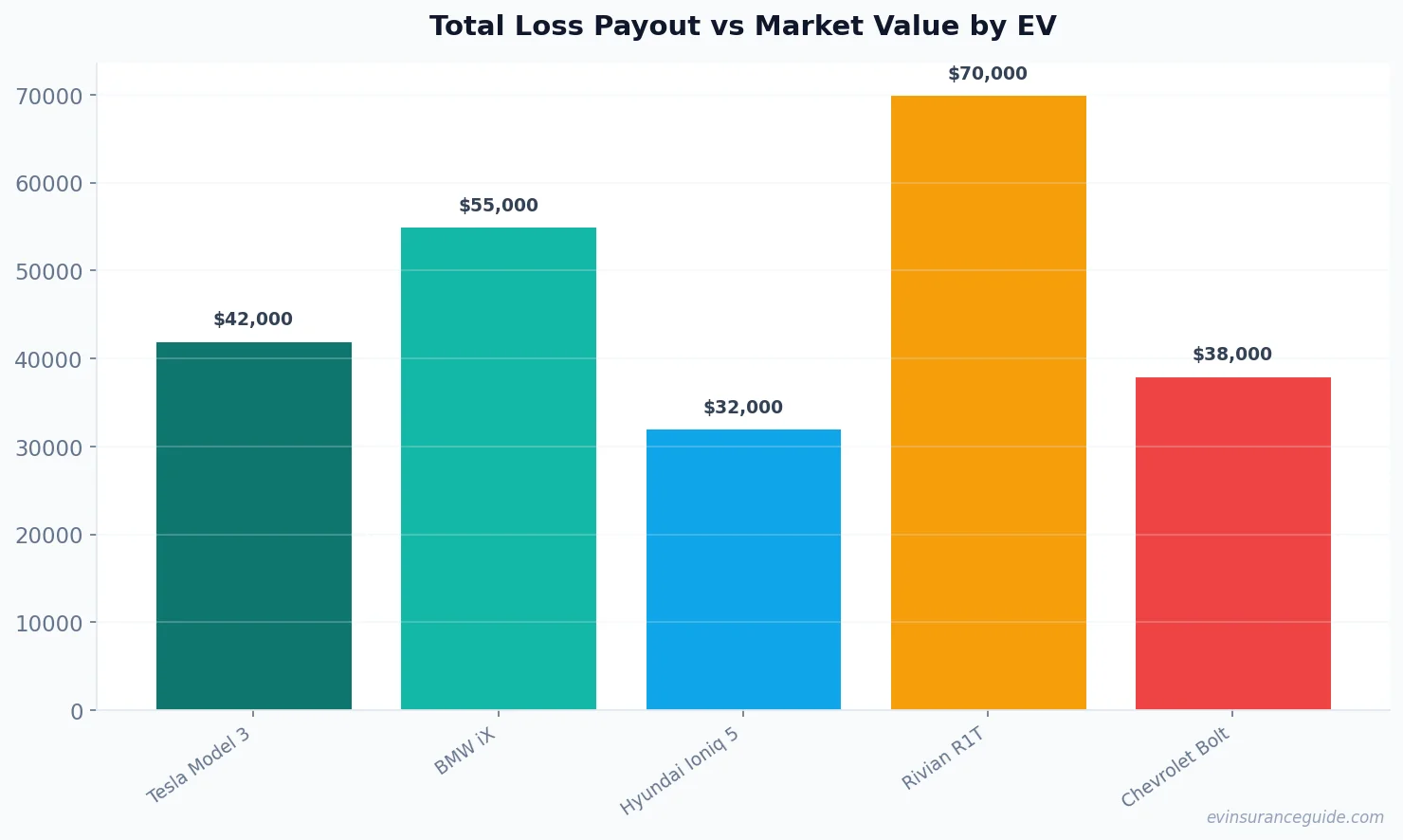

When your EV is totaled, the insurance company will typically determine the actual cash value (ACV) of your vehicle, which is the market value of your EV at the time of the accident. For example, let's say you own a Tesla Model 3 with a market value of $45,000. If you're insured with a company like Geico, they might offer you a total loss payout of $42,000, which is the ACV minus any deductibles. Dead serious - that's a $3,000 difference. But, if you've got a comprehensive coverage policy with a company like Progressive, you might be able to negotiate a higher payout, closer to the original purchase price of $50,000. That's a big difference, especially if you've got a loan or lease on the vehicle.

Now, the thing is, EV insurance by state can vary widely. Some states, like California, have more stringent regulations around total loss payouts, which can work in your favor. But, in other states, like Florida, the rules are more lax, and you might find yourself fighting for a fair payout. And, let's be real - insurance companies aren't always transparent about their total loss payout calculations. You've got to do your research, and know what you're entitled to. For instance, did you know that some insurance companies, like State Farm, offer a "new car replacement" option, which can give you a brand new vehicle if yours is totaled within a certain timeframe?

But, here's the thing - even with a comprehensive coverage policy, you might not get the full market value of your EV. That's where gap insurance comes in - it can help cover the difference between the ACV and the outstanding loan or lease balance. For example, let's say you owe $38,000 on your Tesla Model 3, but the insurance company only offers you a total loss payout of $32,000. Gap insurance can help cover that $6,000 difference. And, trust me, you don't want to be stuck with a $6,000 debt on a vehicle that's no longer drivable.

A Tesla Model 3 vs a Gas-Powered Honda Civic: Which Gets a Better Total Loss Payout?

Compare the total loss payout for a Tesla Model 3 to a gas-powered Honda Civic. The Tesla Model 3, with its higher market value and more complex technology, might actually get a lower total loss payout than the Honda Civic. Yep, you read that right - the Tesla Model 3, which costs more to purchase and maintain, might not get the same level of compensation as a more affordable gas-powered vehicle. That's because insurance companies often use a formula to determine the ACV, which takes into account the vehicle's make, model, year, and mileage. And, let's be real, electric vehicles are still a relatively new technology, and the residual value can be harder to determine.

But, don't get me wrong - EVs are still a great investment, and the total loss payout is just one aspect of the overall cost of ownership. With the rising demand for electric vehicles, and the increasing competition among insurance companies, you can expect to see more competitive total loss payouts in the future. And, as the technology improves, and the market value of EVs becomes more stable, you can expect to see more transparency around total loss payout calculations. For instance, companies like Rivian are already offering more comprehensive coverage options, which can give you peace of mind when driving your EV.

The Story of How I Got Screwed Over by My Insurance Company

I've got a friend, let's call him Dave, who owns a BMW iX. He was involved in a pretty bad accident, and his vehicle was totaled. The insurance company offered him a total loss payout of $55,000, which was significantly lower than the market value of his vehicle. Dave was furious, and he ended up hiring a lawyer to negotiate a better payout. Long story short, they were able to get the insurance company to increase the payout to $65,000, which was still lower than the original purchase price, but closer to the market value. That one stung, and it's a great example of why you need to be proactive when dealing with insurance companies.

And, let me tell you, it's not just about the payout - it's about the hassle and stress of dealing with the insurance company. You've got to be prepared to advocate for yourself, and know what you're entitled to. For instance, did you know that some insurance companies, like Allstate, offer a "total loss concierge" service, which can help guide you through the process? It's not a guarantee, but it can definitely make a difference.

Busting the Myth That Total Loss Payouts Are Always Fair

Myth: total loss payouts are always fair and reflective of the vehicle's market value. Reality: not always. Insurance companies often use a formula to determine the ACV, which can be subjective and open to interpretation. And, let's be real, insurance companies are in the business of making money, not paying out claims. So, it's up to you to do your research, and know what you're entitled to. For example, if you own a Hyundai Ioniq 5, and it's totaled, you might expect a total loss payout of around $30,000. But, if you've got a comprehensive coverage policy with a company like USAA, you might be able to negotiate a higher payout, closer to $35,000.

But, here's the thing - even with a comprehensive coverage policy, you might not get the full market value of your EV. That's where gap insurance comes in - it can help cover the difference between the ACV and the outstanding loan or lease balance. And, trust me, you don't want to be stuck with a $5,000 debt on a vehicle that's no longer drivable. For instance, companies like GapInsurance.com offer specialized gap insurance policies, which can give you peace of mind when driving your EV.

Can You Really Trust Your Insurance Company to Give You a Fair Total Loss Payout?

Can you really trust your insurance company to give you a fair total loss payout? Nope. It's up to you to do your research, and know what you're entitled to. For example, if you own a Rivian R1T, and it's totaled, you might expect a total loss payout of around $70,000. But, if you've got a comprehensive coverage policy with a company like Progressive, you might be able to negotiate a higher payout, closer to $80,000. And, let's be real, it's not just about the payout - it's about the hassle and stress of dealing with the insurance company.

Pro tip: always keep detailed records of your vehicle's maintenance and repair history, as this can help support your case for a higher total loss payout.

And, don't even get me started on the paperwork - it's a nightmare. You've got to be prepared to fill out forms, and provide documentation, and negotiate with the insurance company. It's a hassle, but it's worth it in the end. For instance, companies like Esurance offer online tools, which can help streamline the process.

FAQs

#### What is the average total loss payout for an electric vehicle?

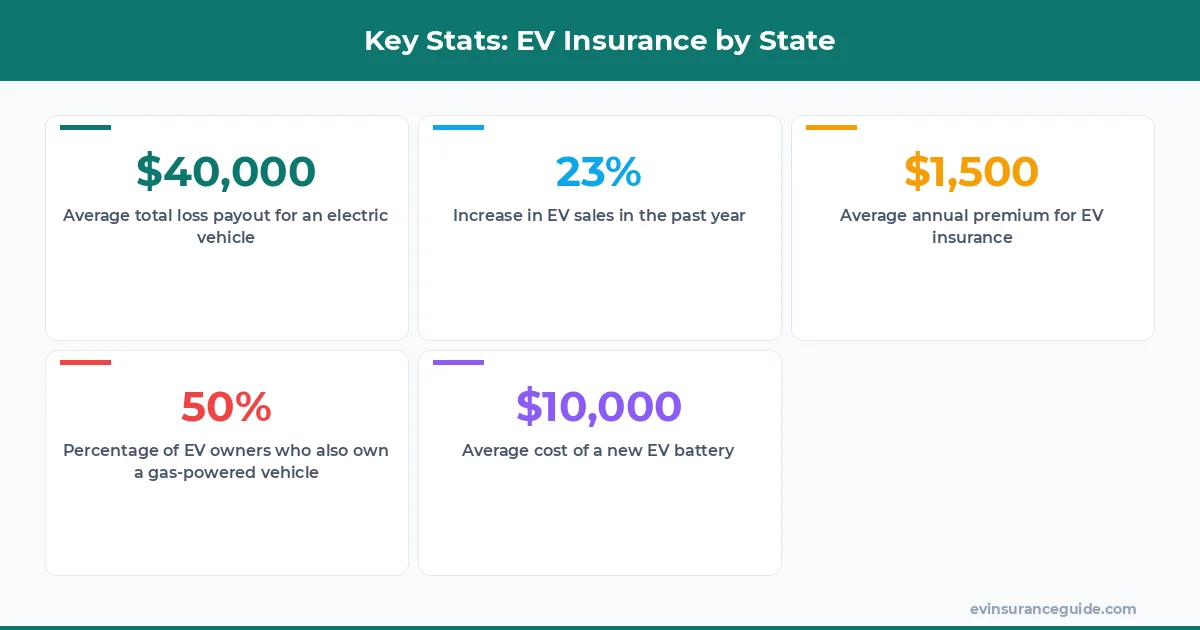

The average total loss payout for an electric vehicle can vary widely, depending on the make, model, and year of the vehicle. However, according to data from the National Association of Insurance Commissioners, the average total loss payout for an electric vehicle is around $40,000.

#### How do insurance companies determine the actual cash value of my EV?

Insurance companies use a formula to determine the ACV, which takes into account the vehicle's make, model, year, and mileage. They may also use data from third-party sources, such as Kelley Blue Book, to determine the market value of your vehicle.

#### Can I negotiate a higher total loss payout with my insurance company?

Yes, you can negotiate a higher total loss payout with your insurance company. It's always a good idea to do your research, and know what you're entitled to, before negotiating with the insurance company.

#### What is gap insurance, and how does it work?

Gap insurance is a type of insurance that can help cover the difference between the ACV and the outstanding loan or lease balance. For example, if you owe $30,000 on your vehicle, but the insurance company only offers you a total loss payout of $25,000, gap insurance can help cover that $5,000 difference.

#### How do I file a total loss claim with my insurance company?

To file a total loss claim with your insurance company, you'll typically need to provide documentation, such as a police report, and proof of ownership. You may also need to fill out forms, and provide additional information, such as the vehicle's maintenance and repair history.

#### Can I purchase a new vehicle with the total loss payout from my insurance company?

Yes, you can purchase a new vehicle with the total loss payout from your insurance company. However, you may need to use the funds to purchase a similar vehicle, or one that is comparable in value to the original vehicle.

Happy driving, and don't overpay! — Alex