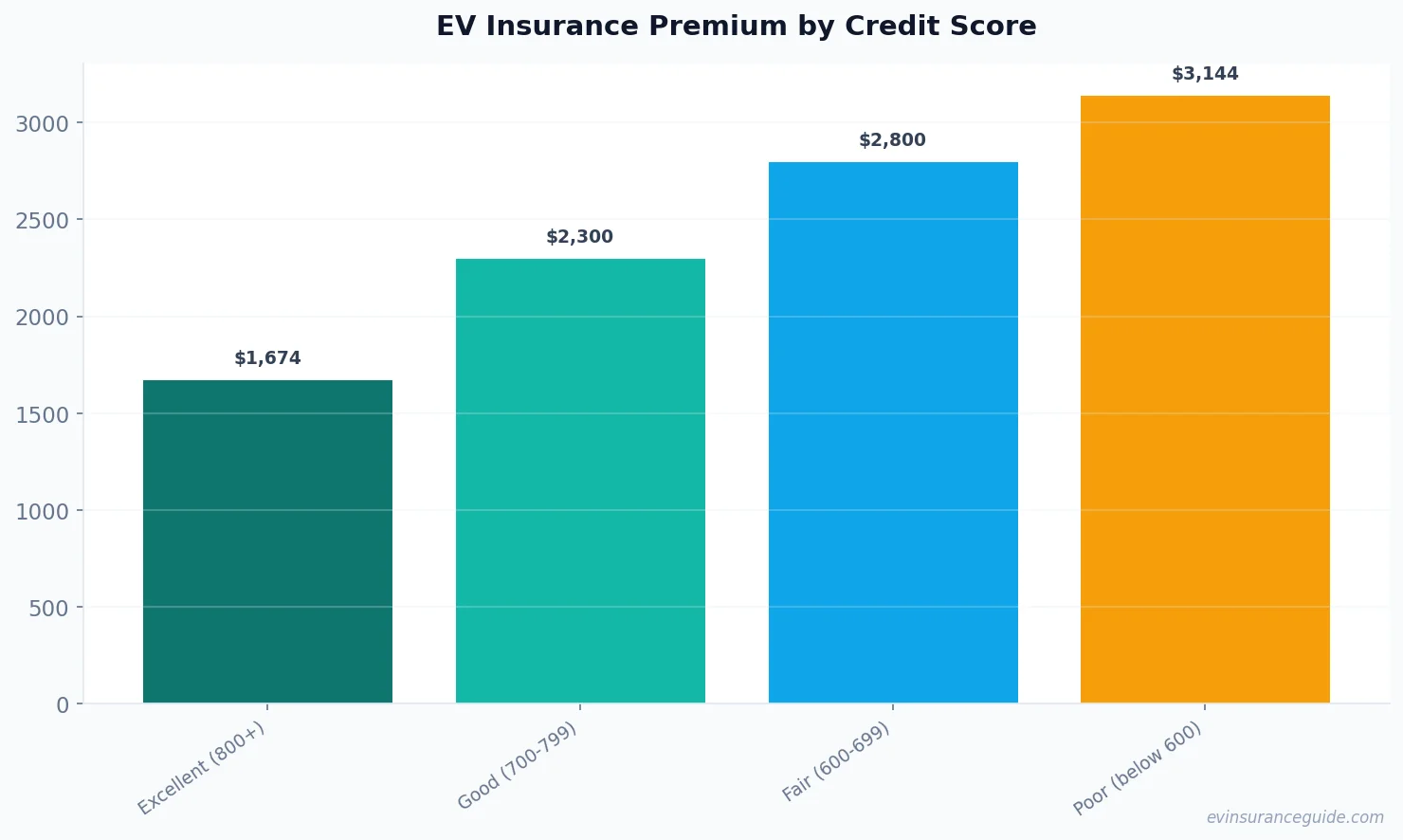

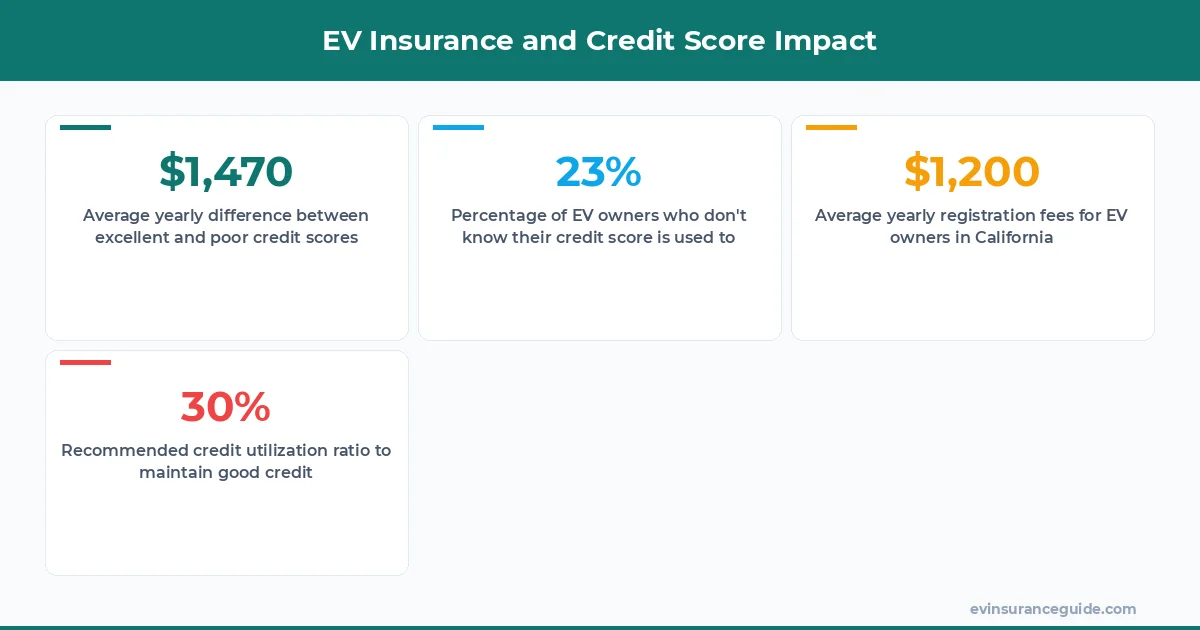

Breaking news: as of 2026, EV insurance rates are skyrocketing, and your credit score is playing a major role - we're talking $1,000+ per year. Sound familiar? You're not alone. I've been digging into the data, and it's mind-boggling. A recent study found that drivers with excellent credit (800+) pay an average of $1,674 per year, while those with poor credit (below 600) pay a whopping $3,144. That's a $1,470 difference. Wild, right?

WARNING — Don't Get Caught Off Guard

Your credit score can significantly impact your EV insurance rates. I've seen cases where a single point difference in credit score can mean hundreds of dollars in premiums. For instance, a Tesla Model 3 owner with a credit score of 750 might pay $2,300 per year, while someone with a score of 760 pays $2,000. That one stung - $300 just for a 10-point difference. Know what the kicker is? Most people don't even realize their credit score is being used to determine their insurance rates. Dead serious.

In some states, like California, Hawaii, Massachusetts, Michigan, Oregon, and Washington, insurance companies are banned from using credit-based insurance scoring. But for the rest of us, it's a different story. I've got a friend, let's call her Rachel, who owns a Hyundai Ioniq 5. She's got a good credit score, around 720, and she's paying $2,500 per year for her insurance. Not bad, right? But if she slips up and her score drops to 680, her rates could jump to $3,000. That's a $500 increase. And it's not just Rachel - millions of EV owners are facing similar rate hikes.

HONEST_OPINION — Credit Scores Are Unfair, But...

We've gotta deal with the system we have. And right now, that means your credit score is a major factor in determining your EV insurance rates. I'm not gonna sugarcoat it - it's unfair. But, if you've got excellent credit, you're gonna reap the rewards. For example, a Rivian owner with a credit score of 820 might pay as low as $1,800 per year. That's a steal. On the other hand, if you've got poor credit, you're gonna pay the price. It's not all doom and gloom, though - some insurers, like USAA and Geico, weigh credit less heavily than others. So, it's worth shopping around.

So, what can you do to improve your insurance score? Well, first off, make sure you're paying your bills on time. Late payments can kill your credit score. And, try to keep your credit utilization ratio below 30%. That means if you've got a $1,000 credit limit, don't go above $300. Simple, right? But, it's amazing how many people don't follow these basic rules. And, if you've got any errors on your credit report, dispute them ASAP. It's gonna take some time and effort, but trust me, it's worth it.

CASUAL_DIRECT — OK So Here's the Deal With Credit Scores

Credit scores are like a report card for your financial habits. And, just like in school, you want to get good grades. A good credit score can save you thousands of dollars per year on your EV insurance. For instance, a BMW iX owner with a credit score of 780 might pay $2,200 per year, while someone with a score of 700 pays $2,800. That's a $600 difference. Now, I know what you're thinking - what about people with fair or poor credit? Don't they deserve a break? And, yeah, I feel you. But, the reality is, insurers are in the business of managing risk. If you've got a history of late payments or defaulted loans, you're a higher risk. It's not personal, it's just business.

But, there is hope. Some insurers offer discounts for people with poor credit. For example, Progressive offers a program called 'Snapshot' that tracks your driving habits and rewards you with lower rates if you're a safe driver. It's not a cure-all, but it can help. And, if you're willing to put in the work, you can improve your credit score over time. It's not gonna happen overnight, but with patience and persistence, you can get there. Just remember, it's a marathon, not a sprint.

Pro tip: if you're shopping for a new EV, consider the insurance costs before you make a purchase. It's not just about the sticker price - you've gotta factor in the ongoing costs, like insurance and maintenance. For example, a Tesla Model Y might have a higher sticker price than a Hyundai Ioniq 5, but the insurance costs might be lower. Do your research, and don't be afraid to negotiate.

QUESTION — Can You Afford the Hidden Costs?

So, you've just bought a shiny new Rivian, and you're excited to hit the road. But, have you considered the hidden costs? I'm not just talking about insurance - I'm talking about maintenance, fuel, and registration. It all adds up. And, if you're not careful, you could end up paying more than you bargained for. For instance, a study found that EV owners in California pay an average of $1,200 per year in registration fees alone. That's on top of insurance, maintenance, and fuel costs. Sound familiar?

But, here's the thing - if you've got excellent credit, you can mitigate some of these costs. For example, you might qualify for lower interest rates on your loan, or you might get better deals on your insurance. It's not a guarantee, but it's definitely worth exploring. And, if you're willing to do your research, you can find ways to save money. Just remember, it's all about being informed and taking control of your finances.

5 Key Takeaways

So, what have we learned so far? Here are the top 5 takeaways:

- 1. Your credit score can significantly impact your EV insurance rates - we're talking $1,000+ per year.

- 2. Some states, like California and Hawaii, ban credit-based insurance scoring.

- 3. Improving your credit score can save you thousands of dollars per year on your EV insurance.

- 4. Some insurers, like USAA and Geico, weigh credit less heavily than others.

- 5. It's essential to factor in ongoing costs, like insurance and maintenance, when shopping for a new EV.

FAQs

#### What is the average EV insurance premium in the US?

The average EV insurance premium in the US is around $2,500 per year, but it can vary significantly depending on your credit score, location, and vehicle model.

#### How can I improve my credit score?

You can improve your credit score by paying your bills on time, keeping your credit utilization ratio below 30%, and disputing any errors on your credit report.

#### Do all insurers use credit-based insurance scoring?

No, some insurers, like USAA and Geico, weigh credit less heavily than others. And, in some states, like California and Hawaii, credit-based insurance scoring is banned.

#### Can I negotiate my EV insurance rates?

Yes, you can negotiate your EV insurance rates. It's essential to shop around and compare quotes from different insurers to find the best deal.

#### What is the difference between a good credit score and an excellent credit score?

A good credit score is typically between 700-799, while an excellent credit score is 800+. The difference can be significant, with excellent credit scores qualifying for lower interest rates and better insurance deals.

#### How can I save money on my EV insurance?

You can save money on your EV insurance by improving your credit score, shopping around for quotes, and taking advantage of discounts and incentives offered by insurers.

That's all from me — go save some money. — Alex