OK so someone DM'd me this question about ev insurance for construction workers and how the job actually jacks up premiums. They run a framing crew, park their Tesla Model Y at muddy sites all week, and haul a Ridgid saw plus three Milwaukee packs in the frunk. They wanted to know if switching to a Rivian R1T would save them anything on the policy or just create new headaches with insurers.

I get these messages every month. Construction folks see the EV tax credits and lower fuel costs but then stare at renewal notices that feel like they're getting punished for working with their hands. The numbers aren't random. Insurers track where you park, what you carry, and how often the truck sits idle on a job site instead of commuting clean miles.

That matters because ev insurance for construction workers carries real lifestyle factors most agents never ask about. Job site parking means higher theft and vandalism scores. Tool coverage gets tacked on as an aftermarket rider. And the work vehicle distinction can flip your rate from personal to commercial if you're not careful.

How Does Parking at Active Job Sites Change Your EV Insurance Premium?

Most carriers slap a 12-18% surcharge when they learn the Tesla Model 3 or Hyundai Ioniq 5 sits on a gravel lot five days a week. Progressive calls it "unattended commercial exposure." State Farm runs a different algorithm and sometimes waives it if you add a $500 deductible bump. The kicker shows up in claims data: tools and charging cables go missing at twice the rate of suburban driveways.

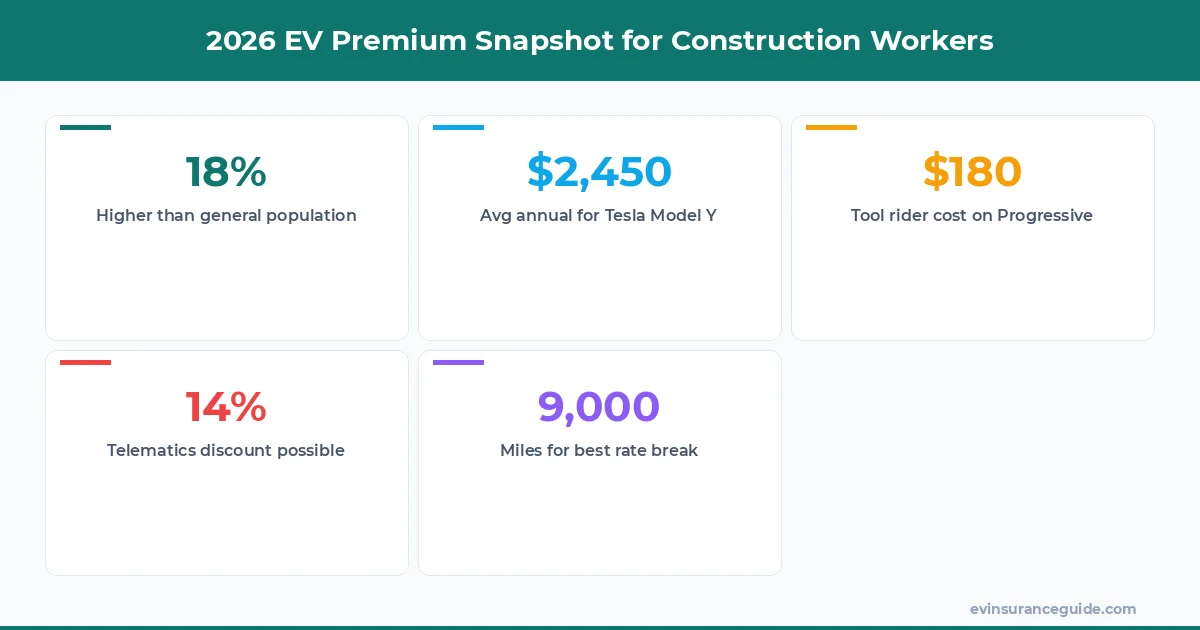

Know what the real pain point is? GPS data. If your insurer pulls telematics and sees the car hasn't moved for eight hours in an industrial zone, the rate engine flags it. One foreman I talked to watched his quote jump from $1,920 to $2,380 after he mentioned parking next to the excavator. He switched to Farmers and locked in a 7% occupational discount by proving he only drives 9,000 miles a year because half his weeks are local jobs.

Sound familiar? Ask specifically about job site parking endorsements before you sign. Some policies treat it like overnight storage at a warehouse and charge accordingly.

Top 5 Insurers for Construction Workers Driving EVs

- Progressive – strongest tool coverage rider at $180 extra per year, covers up to $5,000 in hand tools stolen from a locked frunk on a Rivian.

- State Farm – best telematics forgiveness for low-mileage tradies, knocked 14% off a BMW iX policy for a guy who only drives weekends.

- Geico – fastest commercial-to-personal conversion if you use the EV strictly for getting to sites, not hauling loads.

- Allstate – offers a 10% "skilled trades" discount when you show proof of union card or contractor license.

- Farmers – cheapest for Hyundai Ioniq 5 owners who work fixed 7-3 shifts and garage the car every night.

These aren't ranked by ad spend. They're ranked by actual claims handling stories from guys on the tools who filed last year.

OK So Here's the Deal With Tool Theft and Work Vehicle Rules

Tool theft is the number one surprise on ev insurance for construction workers. Standard comprehensive doesn't cover a $1,800 miter saw unless you buy the rider. Progressive's version paid out same-week for a carpenter in Phoenix whose Ioniq 5 got broken into at a new build. Geico made the guy wait six weeks and still shorted him $400 on depreciation.

The work vehicle distinction trips people up fast. If you write off any mileage as business use, some underwriters reclassify the whole policy. That moves you from personal auto to commercial auto and the premium can double. One electrician learned that the hard way after he mentioned charging the car on a client's job site generator.

Blockquote: "Add the tool endorsement and keep business use under 20% or you'll pay commercial rates for a personal EV."

Honestly, Most Standard Quotes Overcharge Tradeworkers by Default

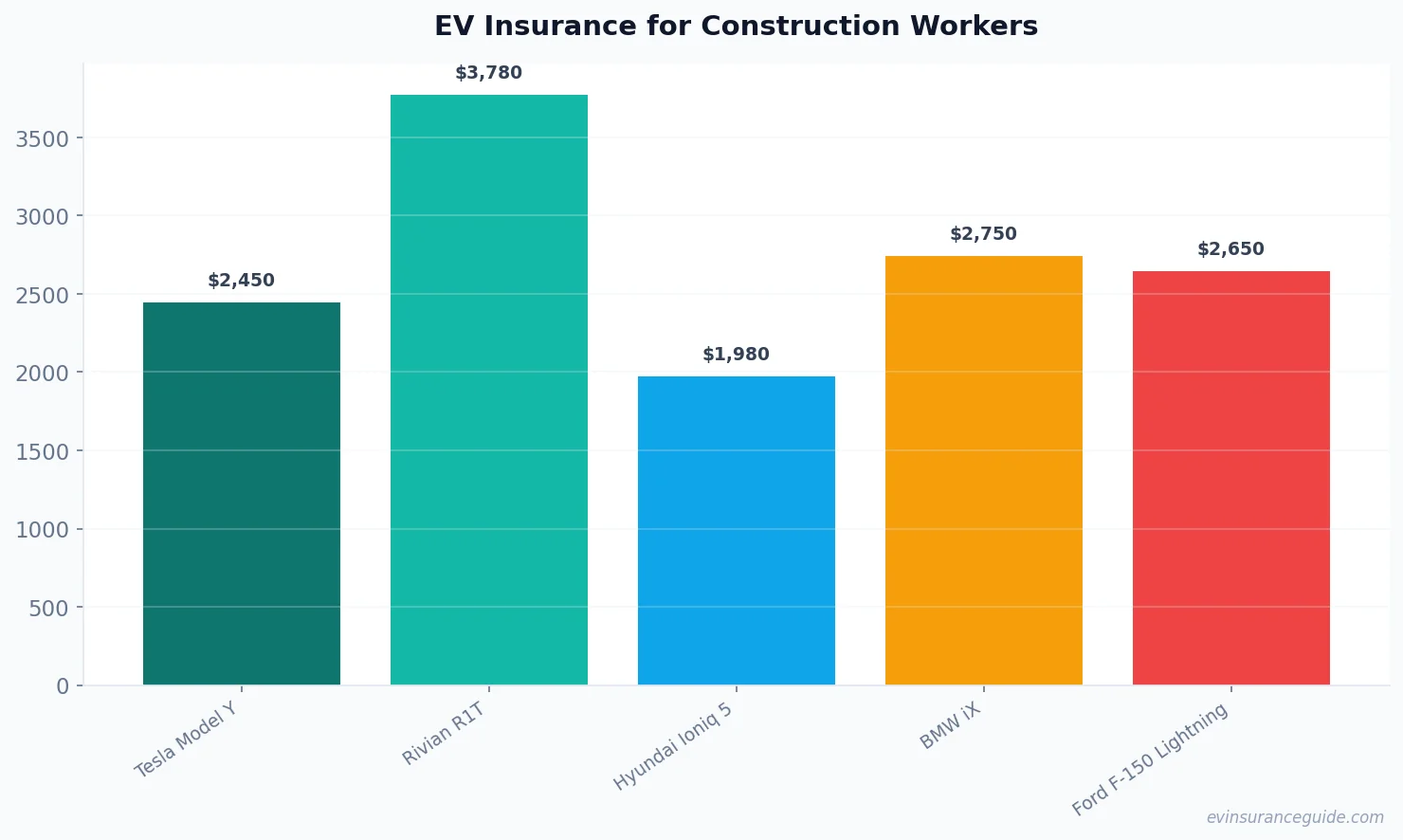

Blunt truth: the average quote engine doesn't know the difference between a Tesla Model Y driven by a remote worker and one driven by a guy who leaves it at dusty sites. They default to higher risk. That's why ev insurance for construction workers runs 15-22% above the general population for the same car. A 2026 Rivian R1T quote came in at $3,110 for a general driver but $3,780 for a framing foreman in the same ZIP code.

The fix is simple but most people skip it. Call the agent, mention your occupation explicitly, and ask for the skilled trades discount before they run the final number. Allstate and Farmers both have it buried in their rate books.

Let Me Tell You About the Concrete Guy Who Switched to a Model Y

He drove a gas F-150 for ten years, paid $2,050 a year. Bought a Tesla Model Y, parked it behind the mixer every day, and the first quote landed at $2,680. After adding proof of 8,400 annual miles and a $250 tool rider he dropped it to $2,310. Still higher than the truck, but the $300 monthly fuel savings more than covered the gap.

His schedule helped. Night shifts meant the car sat in a locked yard instead of a street. The insurer credited that pattern and knocked off another 6%.

What mileage threshold usually triggers a rate drop for construction workers?

Under 10,000 miles a year gets you the biggest break. Most carriers treat 12,000 as the cutoff. Anything under that and you're looking at 8-12% savings on ev insurance for construction workers.

Does adding a tool rider affect my deductible on the EV itself?

No. The rider sits on top of comprehensive coverage. Your collision deductible stays the same. Just make sure the tool limit matches what you actually carry in the vehicle.

Can I keep personal rates if I occasionally haul materials?

Yes if the business use stays below 20% of total miles. Log it for a month. If you're over, expect the commercial re-rate at renewal.

Which EV loses the least value in claims for tradeworkers?

Hyundai Ioniq 5. Parts are cheaper and more available than Rivian or BMW iX. That keeps premiums 10% lower than the BMW in most construction ZIP codes.

How often should I update my insurer about job site changes?

Every time your main parking location changes for more than 30 days. Moving from a paved lot to a raw dirt site can trigger a mid-term adjustment if they catch it on telematics.

Is usage-based insurance worth it for irregular construction schedules?

Only if you have consistent low-mileage weeks. One week of 400 miles to a distant site wipes out the discount you earned on lighter weeks.

Do union cards actually unlock extra discounts?

Some carriers yes. Allstate and a few regionals give an extra 5% on top of the standard skilled trades discount when you show active membership.

Remember: the best policy is the one you actually understand. — Alex