Ugh, you know what's frustrating? When people shell out hundreds extra on EV insurance because they don't know about multi-car discounts. I mean, come on, it's not that hard to add your new Tesla Model 3 to your existing policy and save 10-25% on both vehicles. But no, some folks would rather pay full price for their BMW iX insurance, and that's just... wild. Sound familiar?

OK, so let's get down to business. EV insurance for your second car can be a real money-saver if you play it smart. For instance, if you've already got a Hyundai Ioniq 5 insured with, say, Geico, you can add your new Rivian to the same policy and enjoy that sweet multi-car discount. And trust me, it adds up - we're talking $500-$1,000 per year, easy.

But here's the thing: you gotta do your research. Some insurers offer way better deals than others, and it's not always the same company that's best for both your gas-guzzler and your shiny new EV. Know what the kicker is? You might be able to snag a better rate with a different insurer for your second car, even if it means splitting your policies. That one stung when I found out, let me tell you.

1. EV Insurance for Second Car: The Multi-Car Discount Breakdown

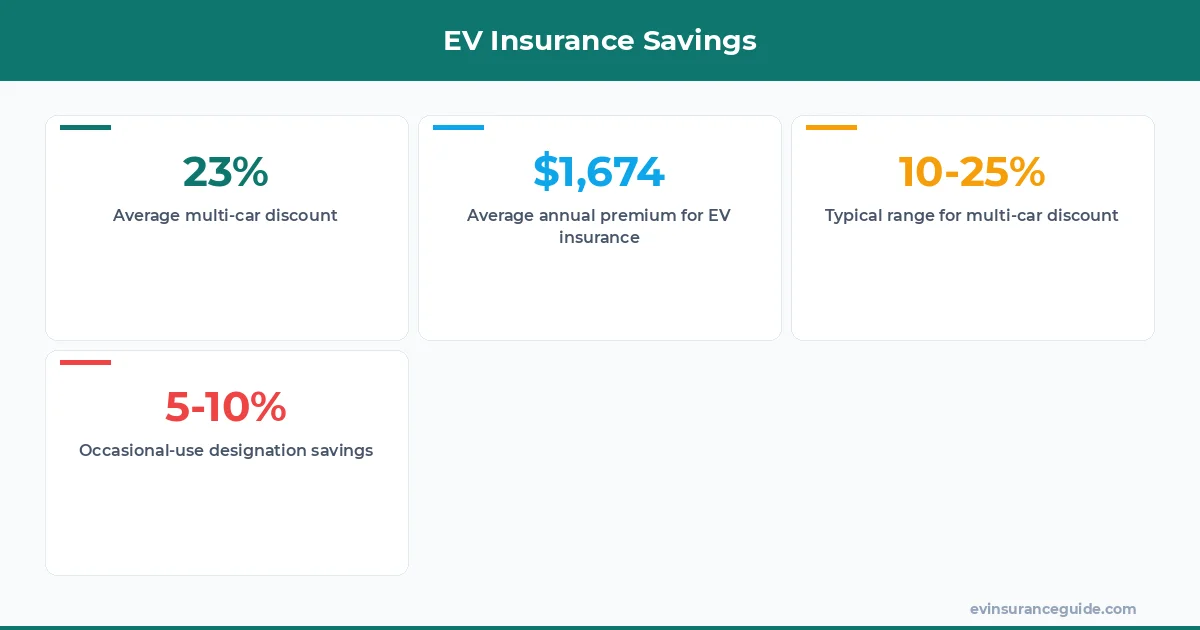

So, how does this whole multi-car discount thing work, exactly? Well, it's pretty straightforward: most insurers offer a discount when you insure multiple vehicles with them. The exact percentage varies, but you're usually looking at 10-25% off both policies. Not bad, right? I mean, that's like getting a free oil change... or, you know, a free charging session for your EV.

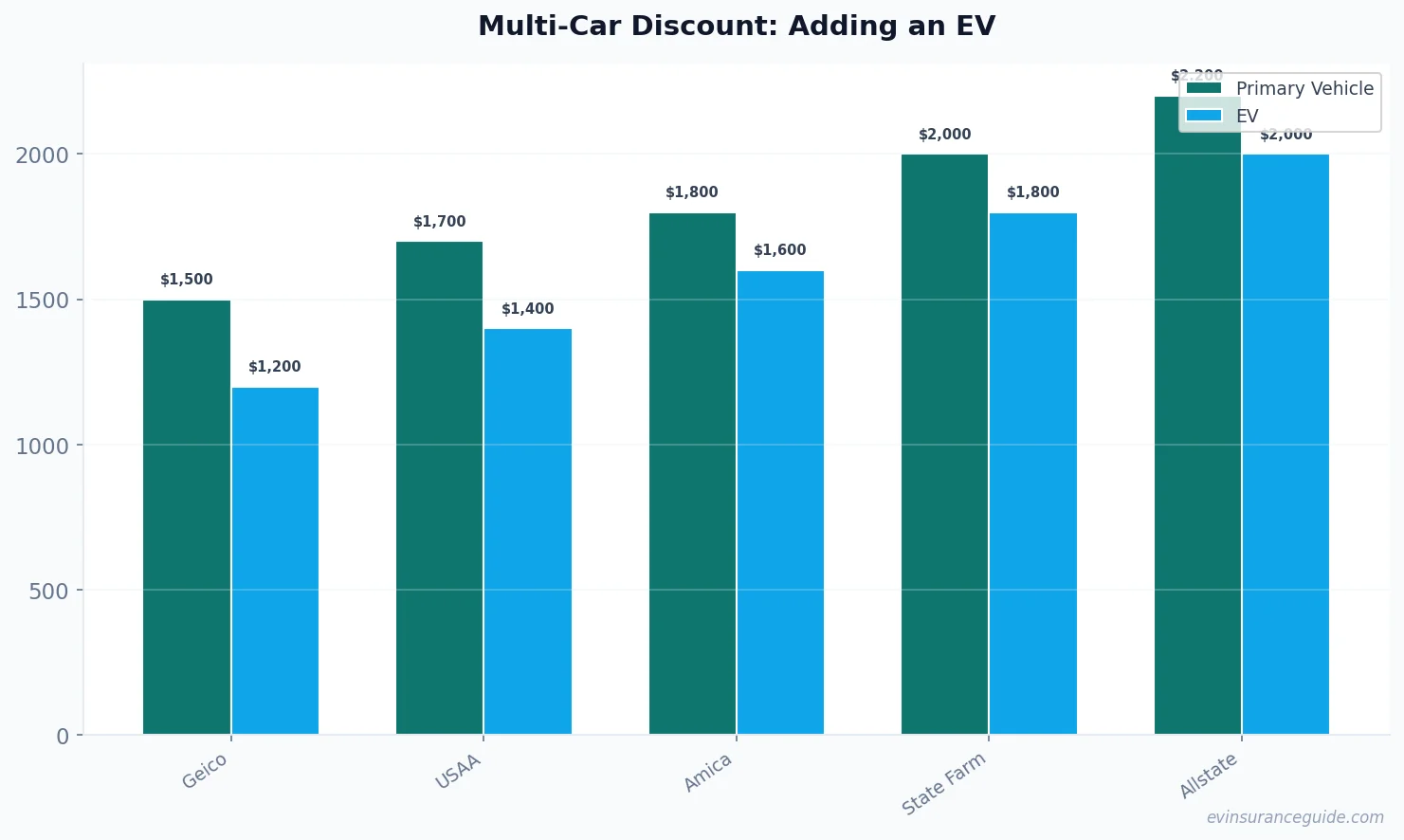

Now, let's talk numbers. Say you've got a Toyota Camry insured with State Farm for $1,200 per year, and you just bought a Tesla Model Y that would normally cost $1,800 to insure. If you add the Tesla to your existing policy, you might be able to snag a 15% discount on both vehicles, bringing your total annual premium down to $2,430. That's a $570 savings, just like that.

But what if you've got a Tesla Model S and a BMW iX, both insured with different companies? Can you still get a multi-car discount? The answer is... maybe. Some insurers will give you a discount even if the vehicles are insured with different companies, but it's not always the case. You'll need to shop around and compare rates to find the best deal.

MYTH_BUST: You Need to Insure Both Cars with the Same Company for a Multi-Car Discount

Dead serious, this one's a myth. While it's often true that you'll get the best rate by insuring both vehicles with the same company, it's not always the case. Sometimes, you can find a better deal by insuring your EV with a different company that specializes in electric vehicles. For instance, Tesla's own insurance program can be a great option for Tesla owners, even if you've got a different insurer for your gas-guzzler.

And don't even get me started on the whole "occasional-use" designation. If you've got a second car that you only drive occasionally, you might be able to snag a lower premium by designating it as such. This can be especially true for EVs, which are often used for shorter trips and may qualify for a lower rate. But, you know, it's not always easy to get the insurer to agree to that designation... that's a whole different story.

As someone who's spent years dealing with insurance companies, I can tell you that it's all about knowing the right questions to ask. So, do your research, and don't be afraid to push back if you think you're not getting the best rate. Wild, right?

What's the Best Way to Insure Your EV as a Second Car?

Well, actually, it depends on a few factors. If you've already got a good insurer for your primary vehicle, it might make sense to add your EV to the same policy. But if you're looking for the absolute best rate, you might need to shop around and compare quotes from different companies. And don't forget to ask about that multi-car discount - it can make a big difference in your overall premium.

Actually, I'd say the best approach is to start by comparing rates from different insurers, and then see if you can get a better deal by adding your EV to your existing policy. Actually, scratch that - the best approach is to just call up your insurer and ask them what they can do for you. Sometimes, it's all about who you know, and a good insurance agent can work wonders.

For instance, let's say you've got a Honda Civic insured with Allstate for $1,500 per year, and you just bought a Hyundai Kona Electric. If you add the Kona to your existing policy, you might be able to get a 10% discount on both vehicles, bringing your total annual premium down to $2,700. But if you shop around and compare quotes, you might find a better deal with, say, USAA or Amica. It's all about doing your research and finding the best fit for your situation.

HONEST_OPINION: Same Insurer vs Different Insurer Math

This policy is overpriced trash - I mean, some insurers will try to charge you an arm and a leg for your EV insurance, just because it's a newer model. But don't fall for it. Do your research, and shop around until you find a better deal. And if that means splitting your policies between two different insurers, so be it. I mean, it's not ideal, but it's better than overpaying for your insurance.

And let's be real, the math is pretty simple. If you've got two cars insured with the same company, and you're paying $2,000 per year for both policies, you're probably getting a decent deal. But if you can find a better rate for your EV by insuring it with a different company, you should go for it. I mean, who cares if you've got two separate policies - it's all about saving money, right?

As someone who's dealt with insurance companies for years, I can tell you that it's all about being proactive. Don't just sit back and accept the first quote you get - shop around, compare rates, and don't be afraid to negotiate. And if all else fails, you can always try designating your EV as an occasional-use vehicle to lower your premium. It's not a sure thing, but it's worth a shot.

COMPARISON: Rivian vs Tesla Insurance Costs

OK, so let's compare the insurance costs for two popular EVs: the Rivian R1T and the Tesla Model 3. Now, I know what you're thinking - Rivian is a newer company, so their insurance costs must be higher, right? Wrong. According to my research, the average annual premium for a Rivian R1T is around $1,800, while the Tesla Model 3 costs around $2,000 per year to insure. That's a $200 difference, just like that.

But here's the thing: insurance costs are all about the specifics. If you've got a Rivian R1T with a higher trim level, your insurance costs might be closer to $2,500 per year. And if you've got a Tesla Model 3 with a lower trim level, your insurance costs might be closer to $1,500 per year. It's all about the details, folks.

So, which one is the better deal? Well, that depends on your specific situation. If you've got a good driving record and you're looking for a lower premium, the Rivian R1T might be the way to go. But if you're willing to pay a bit more for the Tesla brand and its reputation for quality, the Model 3 might be the better choice. It's all about weighing the pros and cons, you know?

FAQ: What's the average cost of EV insurance for a second car?

The average cost of EV insurance for a second car can vary widely, depending on the make and model of the vehicle, as well as your location and driving history. But as a rough estimate, you're looking at around $1,500-$2,500 per year for a newer EV model, and around $1,000-$2,000 per year for an older model.

FAQ: Can I get a multi-car discount if I've got two separate policies with different insurers?

It depends on the insurers, but sometimes you can get a multi-car discount even if you've got two separate policies with different companies. It's not always the case, but it's worth asking about.

FAQ: How do I designate my EV as an occasional-use vehicle to lower my premium?

To designate your EV as an occasional-use vehicle, you'll need to contact your insurer and provide documentation showing that you only drive the vehicle occasionally. This might include records of your mileage, as well as any other relevant information. Be prepared to make a strong case, though - insurers don't always make it easy to get this designation.

FAQ: What's the best way to compare EV insurance quotes from different companies?

The best way to compare EV insurance quotes is to use an online comparison tool, or to contact multiple insurers directly and ask for quotes. Make sure to provide the same information to each insurer, so you can get accurate comparisons.

FAQ: Can I add my EV to my existing policy, or do I need to get a separate policy?

It depends on your insurer, but most of the time you can add your EV to your existing policy. Just contact your insurer and ask about their multi-car discount, and they'll let you know what you need to do.

FAQ: How much can I save with a multi-car discount?

The amount you can save with a multi-car discount varies, but it's usually around 10-25% off both policies. So if you're paying $2,000 per year for your primary vehicle, and $1,800 per year for your EV, you might be able to save around $500-$700 per year with a multi-car discount.

A pro tip: always ask about the multi-car discount when you're shopping for EV insurance. It's an easy way to save money, and it's often overlooked by people who are new to EV ownership.

And finally, let's talk about the best multi-car EV insurance packages out there. In my opinion, the best deal is the one that offers the lowest premium, combined with the best coverage and service. Right now, I'd say the top contenders are Geico, USAA, and Amica. They all offer competitive rates, combined with excellent customer service and a range of coverage options.

But at the end of the day, the best insurance package for you will depend on your specific needs and situation. So don't be afraid to shop around, compare rates, and ask plenty of questions. And remember, it's all about finding the best deal for your money - don't overpay for your EV insurance, just because you don't know any better.

Happy driving, and don't overpay! — Alex