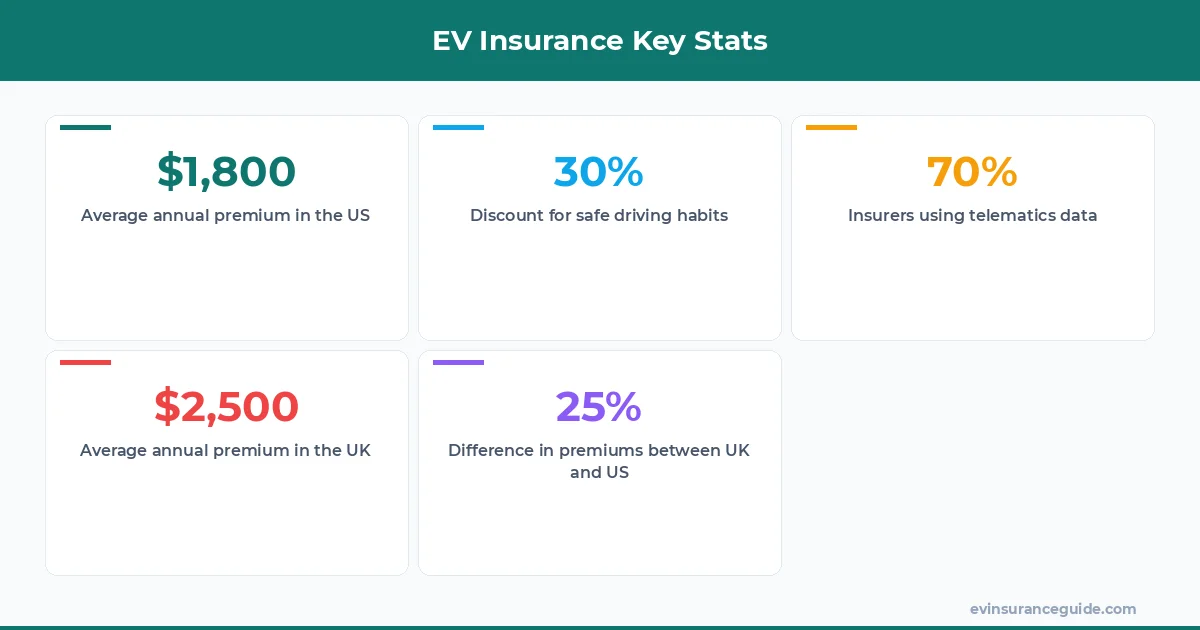

EV insurance in the US can be up to 30% cheaper than in the UK - sound familiar? But what's behind these differences? Is it just a matter of market competition, or is there something more at play? For instance, a Tesla Model 3 owner in the US might pay around $1,800 per year for insurance, while their UK counterpart could shell out over $2,500. That's a significant disparity, especially considering both countries have similar EV adoption rates.

WARNING — The Data Trap: What Insurers Collect

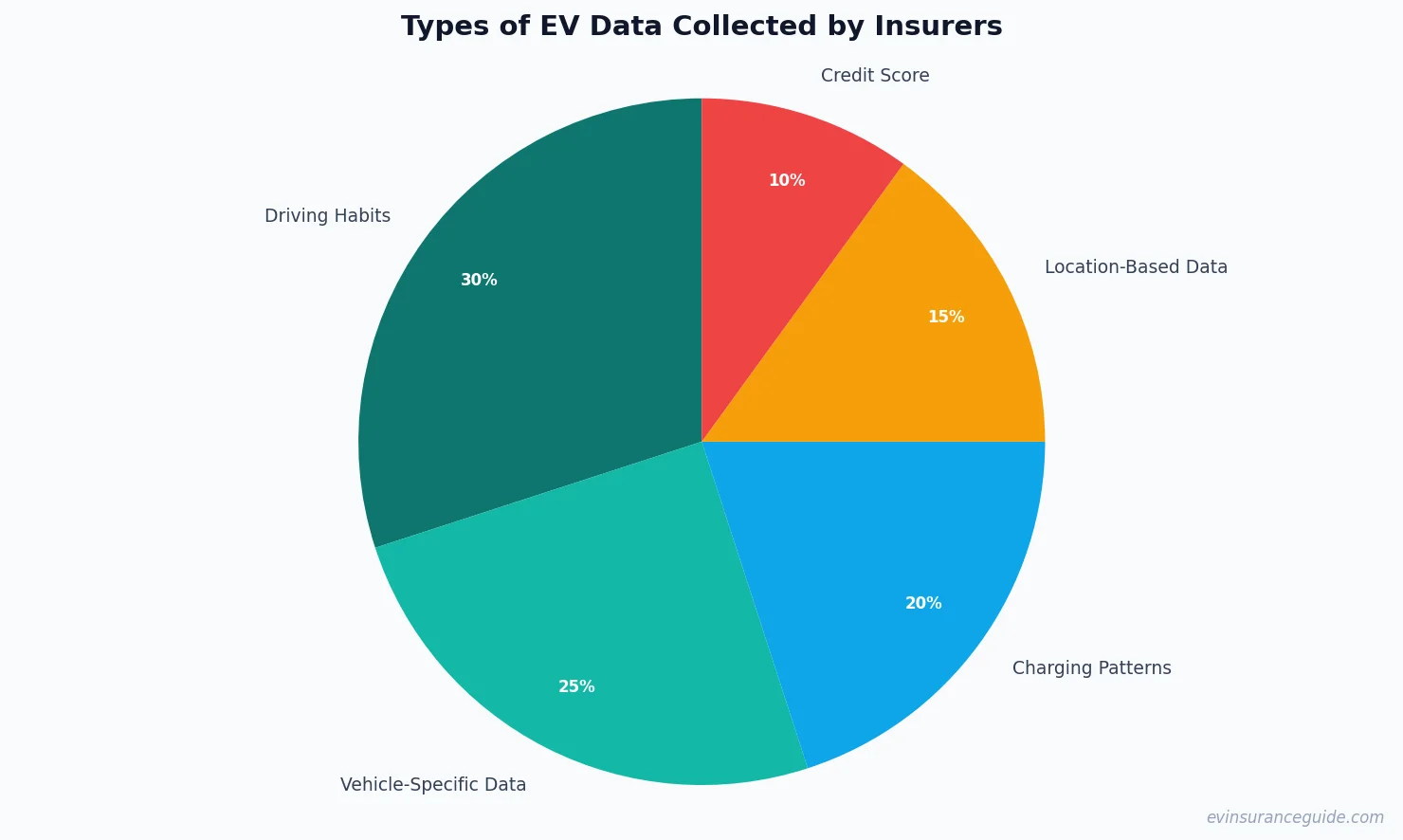

You'd be surprised what insurers collect - and how it impacts your rates. We're talking about everything from your daily commute to your charging habits. For example, a study by the National Association of Insurance Commissioners found that 70% of insurers use telematics data to determine premiums. This can be a double-edged sword: on one hand, safe drivers can enjoy lower rates; on the other, it's a bit unsettling to think that your every move is being tracked. Know what the kicker is? Some insurers, like Liberty Mutual, offer discounts of up to 30% for drivers who exhibit safe behavior.

But here's the thing: the type of data collected can vary greatly between the UK and US. In the UK, insurers might focus more on vehicle-specific data, such as the BMW iX's advanced safety features. In contrast, US insurers might prioritize driver behavior, like speeding or hard braking. Wild, right? It's like two different worlds.

OK So Here's the Deal With EV Insurance UK vs US

Let's get real - EV insurance is still a relatively new market, and there's a lot of confusion around what's covered and what's not. For instance, does your policy include charging station liability? What about home charger installation costs? These are crucial questions, especially for owners of high-end EVs like the Rivian R1T.

And then there's the issue of data sharing. Who gets access to your driving data, and how is it used? Well, actually, it's a bit of a maze. Some insurers, like State Farm, have partnerships with data analytics firms to help determine premiums. Others, like USAA, use in-house teams to review driving data. The takeaway? It's essential to read the fine print and understand what you're signing up for.

Pro tip: Always review your policy's data sharing agreement before signing up. You might be surprised at what's included - or excluded.

Busting the Myth: EVs Are More Expensive to Insure

Dead serious - this is a common misconception. While it's true that some EVs, like the Tesla Model Y, can be pricier to insure, others, such as the Hyundai Ioniq 5, can actually be cheaper. It all depends on various factors, including the vehicle's safety features, driver behavior, and even the insurance company itself.

For example, a study by the Insurance Institute for Highway Safety found that the Tesla Model 3 has a lower claim frequency than many comparable gas-powered vehicles. This can lead to lower premiums for Tesla owners. On the other hand, the BMW iX's advanced technology features might increase premiums due to higher repair costs.

A Story of Two EV Owners: Different Insurance Experiences

Meet Sarah, a Tesla Model 3 owner in the US, and John, a BMW iX owner in the UK. Both have similar driving habits and vehicle models, but their insurance experiences are worlds apart. Sarah pays around $1,500 per year for insurance, while John shells out over $2,200. The reason? Different data collection and analysis methods used by their respective insurers.

This highlights the need for transparency and standardization in EV insurance. As the market continues to grow, it's essential that insurers and regulators work together to create a level playing field. Otherwise, we might see a situation where some EV owners are unfairly penalized due to arbitrary data collection methods.

5 Key Takeaways for EV Insurance UK vs US

Here are the essential points to remember:

- 1. Data collection methods differ between UK and US insurers, affecting premiums.

- 2. EVs can be cheaper to insure than gas-powered vehicles, depending on the model and driver behavior.

- 3. Transparency and standardization are crucial for a fair EV insurance market.

- 4. Insurers like Liberty Mutual and USAA offer discounts for safe driving habits.

- 5. Always review your policy's data sharing agreement before signing up.

FAQs

#### What types of data do EV insurers collect?

EV insurers collect a range of data, including driving habits, vehicle-specific information, and charging patterns. This data is used to determine premiums and can vary between UK and US insurers.

#### Can I opt-out of data collection?

It depends on the insurer and policy. Some insurers might offer opt-out options, while others might require data sharing as part of the policy agreement. Always review your policy's terms before signing up.

#### How does EV insurance UK vs US compare in terms of cost?

On average, EV insurance in the US can be up to 30% cheaper than in the UK. However, this depends on various factors, including the vehicle model, driver behavior, and insurance company.

#### What's the average annual premium for EV insurance in the US?

The average annual premium for EV insurance in the US can range from $1,500 to $2,500, depending on the vehicle model and driver behavior.

#### Can I get a discount for driving an EV?

Some insurers, like State Farm, offer discounts for driving an EV. However, these discounts can vary depending on the insurer and policy. Always ask about available discounts when shopping for EV insurance.

#### How does EV insurance affect my credit score?

In some cases, EV insurance can affect your credit score, especially if you're late with payments or have a poor driving record. However, this depends on the insurer and policy. Always review your policy's terms before signing up.

Go get yourself a better quote. You deserve it.

— Alex