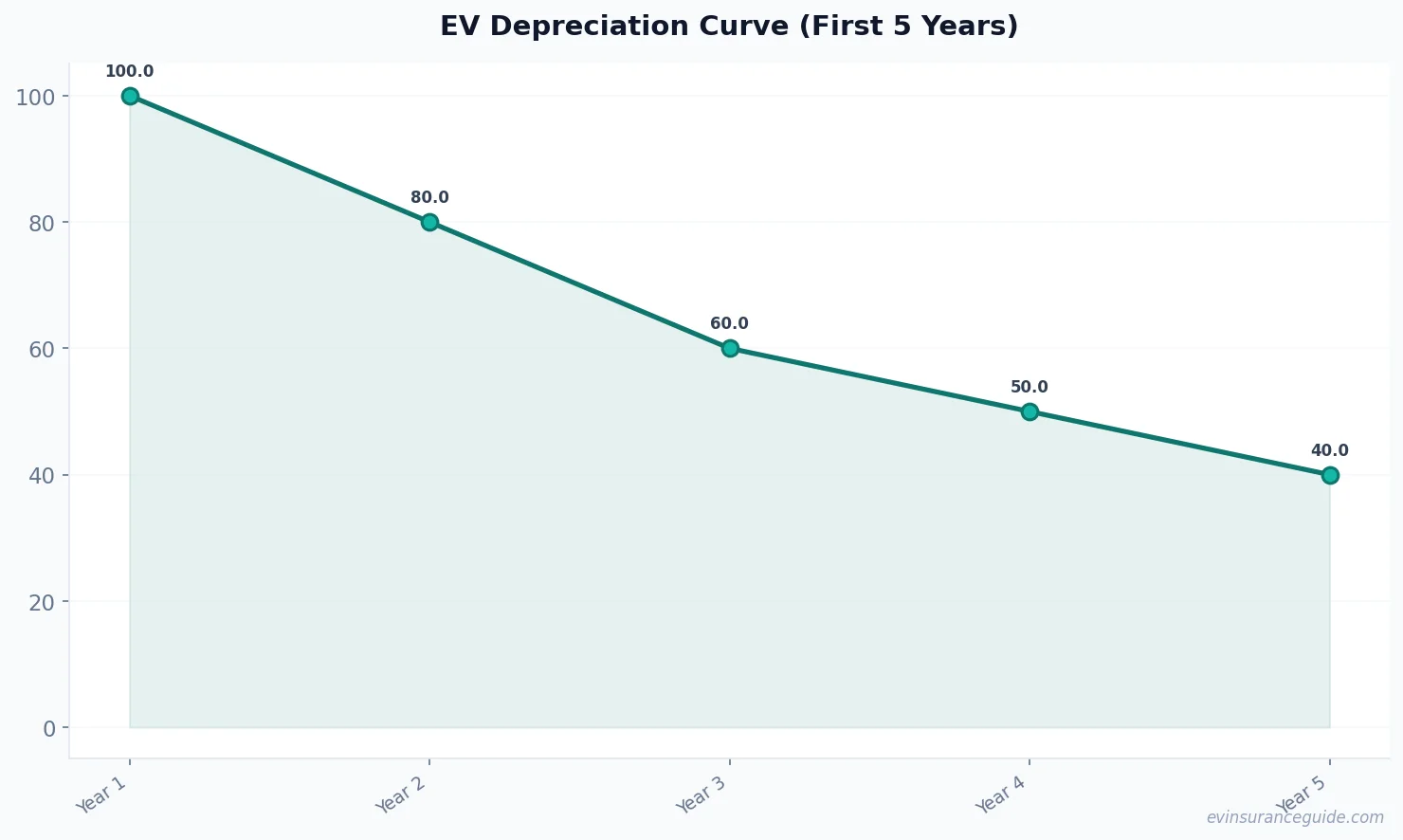

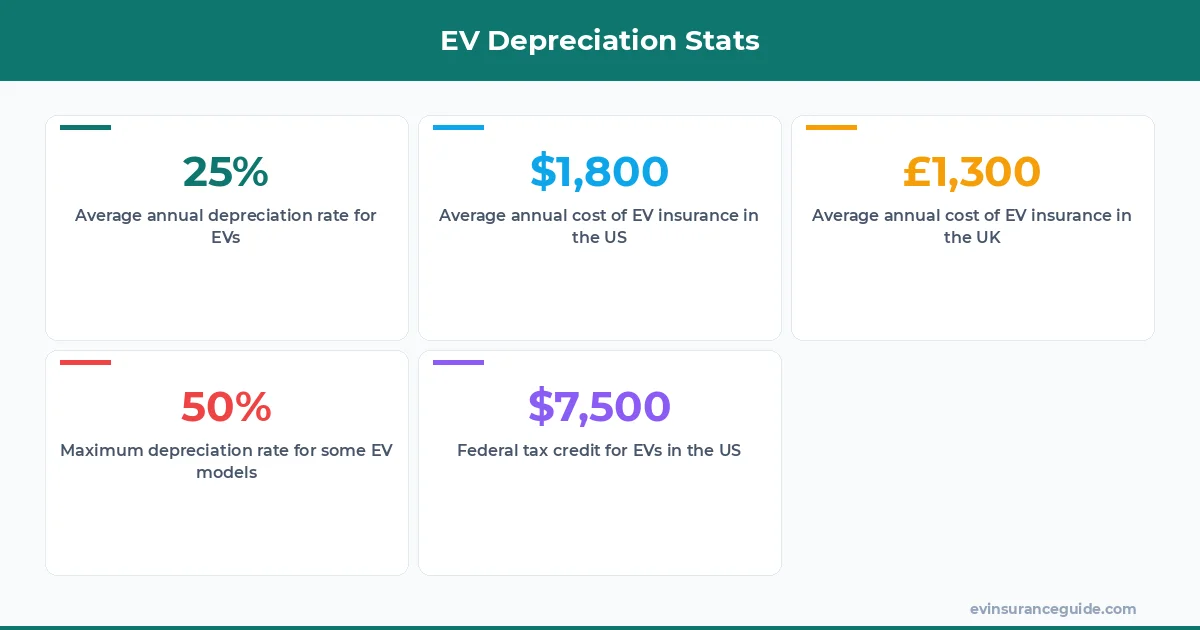

Just like how a Tesla Model 3's battery loses range over time, its resale value takes a hit too - and that's where EV insurance UK vs US comes in. You see, insurance companies factor in depreciation when calculating your premiums, so it's crucial to understand how fast your electric car loses value. Sound familiar? Know what the kicker is? The depreciation curve for EVs is steeper than gas-guzzlers, with some models losing up to 50% of their value within the first three years. That one stung.

Compare Apples to Oranges: EV Depreciation in the UK vs US

Buying an electric car is a significant investment, and the last thing you want is to see its value plummet. But, what if I told you that EV insurance UK vs US has different depreciation rates? Yep, it's true. In the UK, the BMW iX, for instance, retains around 55% of its value after three years, whereas in the US, it's more like 45%. That's a significant difference, especially when you consider the average cost of EV insurance in the US is around $1,800 per year, while in the UK, it's closer to £1,300 (approximately $1,700 USD). Wild, right? I mean, who wouldn't want to save a few hundred bucks on their premium?

Now, let's talk turkey. The Hyundai Ioniq 5, a popular EV model, has a list price of around $40,000 in the US. However, after three years, its value drops to around $24,000, which is a depreciation of about 40%. In the UK, the same model loses around 35% of its value over the same period. That's a difference of $2,000 - $3,000, which can add up quickly. And, when it comes to EV insurance UK vs US, these depreciation rates play a significant role in determining your premium.

But, here's the thing: EV insurance UK vs US isn't just about depreciation rates. It's also about the overall cost of ownership. In the US, for example, the federal tax credit for EVs is up to $7,500, which can help offset the higher upfront cost of an electric car. In the UK, there's a plug-in car grant of up to £3,500 (approximately $4,500 USD). So, when you factor in these incentives, the total cost of ownership for an EV in the UK vs US is more comparable than you might think.

A Story of EV Insurance Woes: Don't Get Caught Out

Imagine buying a brand-new Rivian R1T, only to find out that its insurance premium is through the roof. Yeah, I know, another insurance article. But hear me out. The thing is, EV insurance UK vs US is still a relatively new market, and insurers are still figuring out how to price these policies. So, you might find that the cost of insurance for your shiny new Rivian is higher than you expected. And, if you don't factor in depreciation, you could be in for a nasty shock when it's time to sell.

For instance, let's say you buy a Rivian R1T for $70,000. After three years, its value might drop to around $40,000, which is a depreciation of about 43%. Now, if you're not careful, you could end up owing more on your loan than the car is worth. That's what's known as being "upside-down" on your loan, and it's a situation you want to avoid at all costs.

But, don't worry, there's hope. By understanding the depreciation curve for your EV, you can make informed decisions about your insurance policy. For example, you might want to consider a policy that factors in the car's actual cash value (ACV) rather than its sticker price. This can help you avoid overpaying for insurance, especially if your car's value has dropped significantly.

As the saying goes: "knowledge is power." And, when it comes to EV insurance UK vs US, knowledge is key. So, do your research, and don't be afraid to shop around for the best deal. You might be surprised at how much you can save.

Beware the Depreciation Trap: EV Insurance UK vs US

Know what the worst part is? The depreciation trap. It's when you buy an EV, and its value drops so quickly that you're stuck with a car that's worth less than you owe on it. That's a nightmare scenario, especially if you're planning to sell or trade-in your car in a few years. And, the thing is, it's not just the car's value that's at risk - it's also your insurance premium. If your car's value drops too quickly, your insurer might raise your premium to compensate for the increased risk.

For example, let's say you buy a Tesla Model Y for $50,000. After two years, its value might drop to around $30,000, which is a depreciation of about 40%. Now, if you're not careful, your insurance premium might increase to reflect the car's reduced value. And, if you're not prepared, that could be a significant blow to your wallet.

But, here's the thing: you can avoid the depreciation trap by doing your research. Look for EV models that hold their value well, like the Tesla Model 3 or the BMW iX. And, make sure you understand the depreciation curve for your car before you buy. It's not rocket science, but it does require some planning and foresight.

Pro tip: When buying an EV, consider the total cost of ownership, including depreciation, insurance, and maintenance. It's not just about the sticker price - it's about the overall cost of owning the car.

What's the Real Cost of EV Insurance UK vs US?

So, what's the real cost of EV insurance UK vs US? Well, that depends on a few factors, including the car's make and model, its value, and your driving history. But, as a general rule, you can expect to pay more for EV insurance in the US than in the UK. For example, the average cost of insurance for a Tesla Model 3 in the US is around $2,000 per year, while in the UK, it's closer to £1,500 (approximately $2,000 USD).

But, here's the thing: the cost of EV insurance UK vs US isn't just about the premium - it's also about the coverage. In the US, for example, you might need to add additional coverage for things like battery replacement or electric motor damage. And, these added costs can quickly add up.

So, when you're shopping for EV insurance UK vs US, make sure you factor in all the costs, including depreciation, premiums, and coverage. It's not just about finding the cheapest policy - it's about finding the best value.

FAQs

#### What's the average depreciation rate for EVs?

The average depreciation rate for EVs is around 20-30% per year, although this can vary depending on the make and model of the car. For example, the Tesla Model 3 has a depreciation rate of around 25% per year, while the BMW iX has a depreciation rate of around 20% per year.

#### How does EV insurance UK vs US affect my premium?

EV insurance UK vs US can affect your premium in a few ways. For example, if you live in the US, you might pay more for insurance due to the higher cost of living and the increased risk of accidents. In the UK, the cost of insurance is generally lower, but the depreciation rate might be higher.

#### What's the best way to avoid the depreciation trap?

The best way to avoid the depreciation trap is to do your research and understand the depreciation curve for your car. Look for EV models that hold their value well, and make sure you factor in all the costs, including depreciation, premiums, and coverage.

#### Can I customize my EV insurance policy?

Yes, you can customize your EV insurance policy to fit your needs. For example, you might want to add additional coverage for things like battery replacement or electric motor damage. Or, you might want to reduce your premium by increasing your deductible.

#### How does the federal tax credit affect EV insurance UK vs US?

The federal tax credit can affect EV insurance UK vs US by reducing the upfront cost of the car. In the US, for example, the federal tax credit is up to $7,500, which can help offset the higher cost of an EV. In the UK, there's a plug-in car grant of up to £3,500 (approximately $4,500 USD).

#### What's the average cost of EV insurance in the US vs UK?

The average cost of EV insurance in the US is around $1,800 per year, while in the UK, it's closer to £1,300 (approximately $1,700 USD). However, these costs can vary depending on a few factors, including the car's make and model, its value, and your driving history.

#### How does the depreciation curve affect my insurance premium?

The depreciation curve can affect your insurance premium by reducing the car's value over time. If your car's value drops too quickly, your insurer might raise your premium to compensate for the increased risk. So, it's essential to understand the depreciation curve for your car and factor it into your insurance policy.

Stay charged and stay covered! — Alex